The Anti-Money Laundering meaning refers to the set of laws, regulations, and procedures aimed at preventing criminals from disguising illegally obtained funds as legitimate income. In today’s global financial system, where transactions occur across borders in seconds, AML is vital to maintaining financial integrity and preventing illicit activities like terrorism financing, drug trafficking, and corruption. Without robust AML controls, financial institutions risk becoming conduits for criminal enterprises.

This article explores the meaning of AML, the regulatory frameworks that govern it, key laws in different regions, and the emerging innovations shaping its future.

What Is Anti-Money Laundering (AML)?

The AML full form in banking is Anti-Money Laundering. It is a framework of laws, policies, and procedures that financial institutions and other regulated entities use to detect, prevent, and report money laundering activities.

In simple terms, AML is designed to stop criminals from making illegally obtained money, such as profits from drug trafficking, tax evasion, corruption, or terrorist financing, appear as if it came from legitimate sources.

The Anti-Money Laundering guidelines aim to prevent these illicit funds from entering and contaminating the legal economy. Once “cleaned”, dirty money can be used to fund further crimes or integrated into the financial system without drawing attention. AML practices work by monitoring transactions, identifying suspicious activity, and requiring reporting to authorities. These measures help protect the financial system’s integrity, ensure transparency, and support global efforts to combat organised crime and terrorism.

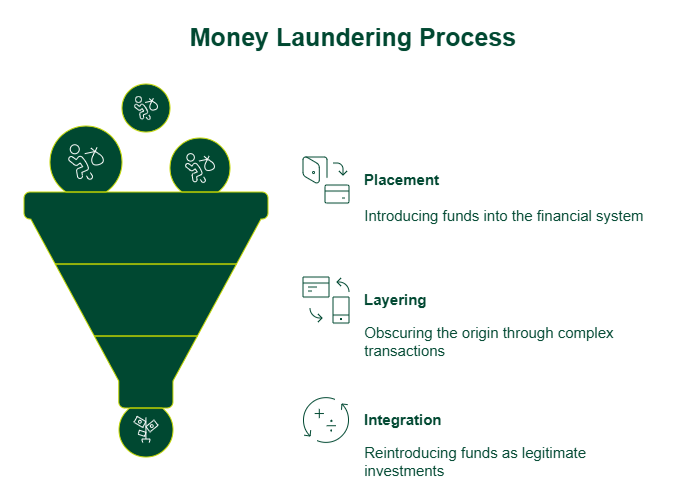

Understanding the Money Laundering Process

Money laundering is a global issue that affects both developed and developing economies. Criminals use various techniques to hide the origin of illicit funds and make them appear legal. While the methods may vary by region and regulation, the process generally follows three key stages: Placement, Layering, and Integration.

Placement

This is the initial stage, where illegal funds are introduced into the financial system. It often involves depositing cash into financial institutions, using it to purchase assets, or funnelling it through businesses to avoid detection.

Layering

In this stage, the money is moved around through complex transactions to obscure its origin. Criminals might transfer funds between multiple accounts, convert currencies, or buy and sell high-value items like art or real estate.

Integration

Here, the laundered money is reintroduced into the economy as seemingly legitimate funds. It may be invested in legal businesses, luxury properties, or used to fund further activities without raising suspicion.

The Evolution and History of AML Regulations

Anti-Money Laundering (AML) regulations have developed significantly over the past few decades in response to the rising complexity of financial crimes. Initially focused on combating issues such as organised crime, AML laws have evolved to address global threats such as terrorism financing, cybercrime, and cross-border corruption. Today, international cooperation and institutional frameworks play a critical role in shaping and enforcing AML standards across jurisdictions.

The key Anti-Money Laundering act in India is the Prevention of Money Laundering Act (PMLA), 2002, which forms the cornerstone of India’s AML efforts.

Importance of Anti-Money Laundering

The Anti-Money Laundering process is essential for safeguarding financial systems, protecting economies, and preserving public trust. It helps prevent the misuse of financial institutions for illegal activities such as fraud, drug trafficking, terrorism financing, and corruption. Effective AML measures not only deter criminal behaviour but also support economic stability and promote transparency in financial transactions.

Why AML Compliance Is Crucial

AML compliance plays a key role in protecting both national and global economies from criminal exploitation. For instance, by detecting and reporting suspicious activities, AML frameworks for NBFCs (NBFC Full Form: Non-Banking Financial Company) help maintain financial integrity, reduce systemic risk, and support fair and lawful economic growth.

Must Read: Learn All About NBFC & Types of NBFC

Key Benefits

- Promotes transparency in financial transactions

- Builds trust among customers and investors

- Reduces risk of regulatory fines and penalties

- Ensures compliance with global legal standards

- Enhances the stability of financial institutions and markets

Key Components of an AML Program

|

AML Program Component

|

Description

|

|

Customer Due Diligence (CDD)

|

Collecting and verifying customer information to assess risk.

|

|

Enhanced Due Diligence (EDD)

|

In-depth investigation for high-risk customers or transactions.

|

|

Know Your Customer (KYC)

|

Confirming the identity of customers to prevent fraud and misuse.

|

|

Transaction Monitoring

|

Ongoing review of transactions to spot unusual or suspicious activity.

|

|

Suspicious Transaction Report (STR)/Suspicious Activity Report (SAR)

|

Reporting detected suspicious activities to regulatory authorities.

|

|

Risk Assessment

|

Identifying and managing money laundering risks within the organisation.

|

|

Training & Independent Audit

|

Educating staff on AML policies and conducting regular program reviews.

|

Global AML Regulations and Frameworks

The Anti-Money Laundering process relies on international cooperation, guided by key regulatory bodies and legal frameworks worldwide. These organisations develop standards, share intelligence, and promote best practices to combat money laundering and terrorism financing on a global scale. Different regions have also enacted specific laws to enforce AML measures domestically, tailored to their unique financial environments.

AML Framework and Compliance in India

India has a structured Anti-Money Laundering (AML) system aimed at safeguarding its financial ecosystem. Key AML laws in India and regulatory bodies ensure that financial institutions follow strict procedures to detect and report suspicious activities.

Prevention of Money Laundering Act (PMLA), 2002

PMLA is the primary AML legislation in India. It mandates financial institutions to verify customer identities, maintain records, and report suspicious transactions to the authorities.

Financial Intelligence Unit – India (FIU-IND)

FIU-IND collects and analyses Suspicious Transaction Reports (STRs) submitted by financial institutions. It shares actionable intelligence with law enforcement and regulators.

RBI, SEBI, and IRDAI AML Guidelines

- The Reserve Bank of India sets AML norms for banks and NBFCs.

- The Securities and Exchange Board of India (SEBI) regulates capital market entities like brokers and mutual funds.

- The Insurance Regulatory and Development Authority of India (IRDAI) enforces Anti-Money Laundering compliance for insurance providers.

Key Compliance Obligations in India

- Customer verification/Know Your Customer (KYC)

- Ongoing transaction monitoring

- STR filing with FIU-IND

- Employee AML training

- Recordkeeping and audits

- Appointment of a compliance officer

How AML Compliance Works (Step-by-Step)

AML compliance is a structured process that financial institutions follow to detect and prevent money laundering. It involves a series of steps, beginning with risk assessment and continuing through monitoring, reporting, and regular audits. Below is a simplified breakdown of how institutions typically implement Anti-Money Laundering regulations.

Risk-Based Approach

A risk-based approach in AML entails identifying and assessing risks related to customers, products, services, and geographies. Institutions apply stricter checks to higher-risk profiles to ensure appropriate scrutiny. Financial products like a personal loan or a business loan may also be evaluated for risk if they involve large sums, frequent transactions, or unclear sources of repayment.

Customer Onboarding & Verification

During onboarding, institutions perform Know Your Customer (KYC) and Customer Due Diligence (CDD) checks. They also verify the identity of beneficial owners in the case of companies or partnerships.

AML Transaction Monitoring & Alerts

Financial entities often use automated systems to monitor transactions in real time. These systems flag unusual or high-risk activities for review by compliance teams.

Suspicious Activity Reporting (SAR/STR)

If suspicious behaviour is identified, a Suspicious Activity Report (SAR) or Suspicious Transaction Report (STR) is filed with the relevant authority. Timely reporting helps prevent further misuse of the system.

Record Keeping & Auditing

All customer data, transactions, and reports must be securely stored and made available for regular internal and external audits to ensure continued compliance.

The Role of Technology in AML

Modern technology is using AI in AML compliance, making it faster, smarter, and more efficient. Automated tools now help financial institutions detect risks early, reduce manual work, and stay ahead of evolving threats.

Modern AML Technologies

- Artificial Intelligence (AI): AI analyses transaction patterns to flag suspicious activity.

- Blockchain: Using blockchain in financial compliance offers transparent, tamper-proof records for traceability.

- RegTech: Automates compliance checks and reporting.

- Biometrics: Strengthens customer identity verification.

Benefits of Technology in AML

- Improves accuracy and reduces false positives.

- Speeds up monitoring and onboarding.

- Cuts compliance costs.

- Enhances security and real-time reporting.

Common Challenges in AML Implementation

- High Compliance Costs: Implementing and maintaining AML systems can be expensive, especially for smaller institutions.

- Complex and Overlapping Regulations: Varying rules across jurisdictions make global compliance difficult and time-consuming.

- Data Silos and Poor Integration: Disconnected systems limit visibility and delay detection of suspicious patterns.

- High Rate of False Positives: Overly sensitive monitoring systems often flag legitimate transactions, increasing workload.

- Lack of Trained AML Professionals: There's a global shortage of skilled experts to manage and interpret AML compliance processes

- Adapting to Digital Fraud and Emerging Risks: Rapid changes in technology and criminal tactics make it hard to keep AML systems up to date.

Innovations and Future of AML

AML is evolving rapidly, thanks to the advancements in technology and global collaboration. Institutions are moving toward smarter, real-time systems that adapt to emerging threats.

Key Trends

- AI & Machine Learning: Improve detection and reduce false positives.

- Blockchain: Enhances transparency and traceability.

- Real-Time Monitoring: Speeds up risk detection and response.

- RegTech Solutions: Automate compliance processes.

- Global Cooperation: Cross-border data sharing and harmonised regulations.

AML and Emerging Risks: Cryptocurrency & Fintech

Cryptocurrencies pose new AML challenges due to their anonymity and decentralised nature, making them attractive for illicit transactions. Criminals employ techniques such as mixing services and unregulated exchanges to launder funds.

Fintech companies, often operating with leaner models, are rapidly adopting advanced AML tools like AI-based monitoring, blockchain analytics, and automated KYC to stay compliant. Regulators are also increasing oversight of the crypto and fintech sectors to close existing gaps.

Consequences of Non-Compliance

- Hefty Fines: Regulatory penalties can reach millions of dollars.

- Legal Action: Criminal or civil charges against the institution or individuals.

- Licence Suspension: Risk of losing the right to operate.

- Reputational Damage: Loss of customer trust and investor confidence.

- Increased Scrutiny: More audits and regulatory pressure in the future.

AML vs KYC vs CDD

|

Term

|

Full Form

|

Purpose

|

Scope

|

|

AML

|

Anti-Money Laundering

|

A broad framework to detect and prevent money laundering and terrorism financing

|

Covers policies, laws, monitoring, reporting, and compliance programs

|

|

KYC

|

Know Your Customer

|

Verifying customer identity before and during the business relationship

|

A key component of AML, done at onboarding

|

|

CDD

|

Customer Due Diligence

|

Assessing customer risk and understanding their financial behaviour

|

Ongoing process based on risk level, part of Anti-Money Laundering and KYC

|

Strengthening AML Frameworks: Future-Ready Strategies

- Integrate AI and Machine Learning

Automate detection and reduce false positives with intelligent analytics.

- Enhance Cross-Border Collaboration

Share data and best practices with global partners and regulators.

- Invest in Continuous Staff Training

Keep teams updated on evolving risks and regulatory changes.

- Adopt RegTech Solutions

Use specialised tools for real-time monitoring and compliance automation.

- Conduct Regular Risk Assessments

Update internal controls based on new products, markets, and threats.

- Strengthen Data Integration

Break down internal silos for a unified view of customer risk.

Conclusion

Anti-Money Laundering (AML) remains vital in the fight against financial crime and protecting the global economy. As risks evolve, innovation and strong compliance are key to staying ahead. With smarter tools and stronger collaboration, institutions can build a more secure and future-ready financial system.

SMFG India Credit is committed to maintaining the highest standards of AML compliance, ensuring secure and transparent financial services across products like personal loans, business loans, and Loans Against Property. Apply online for the solution that best suits your needs, or contact us to learn more.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us