Section 194J of the Income Tax Act, 1961, governs Tax Deducted at Source (TDS) on payments made to residents for professional and technical services, royalty, non-compete fees, and director remuneration. For FY 2026–27, TDS applies when total payments exceed ₹50,000 in a financial year, at rates of 2% or 10% depending on the nature of the service.

What Is Section 194J of the Income Tax Act?

Section 194J requires businesses and specified taxpayers to deduct TDS before paying professionals or technical service providers. It applies to payments made to doctors, lawyers, engineers, architects, consultants, accountants, and similar professionals.

The section also covers technical services, royalty, non-compete fees, and director remuneration. Its primary objective is to facilitate tax collection at the source.

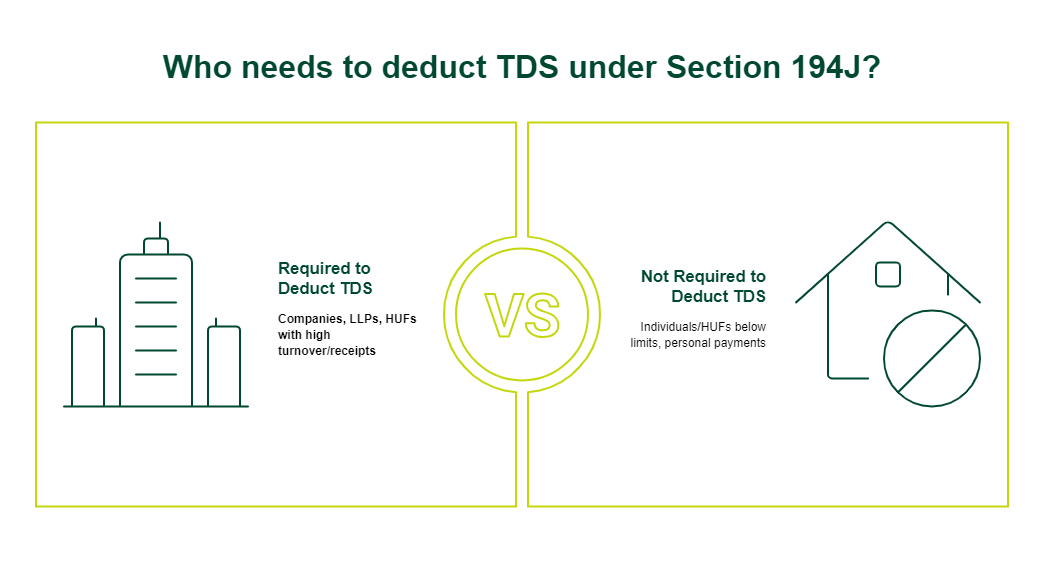

Who Is Required to Deduct TDS Under Section 194J?

Not everyone who makes a payment for professional services needs to deduct TDS. Here is who is responsible:

Required to deduct TDS:

- Companies, partnership firms, LLPs, trusts, government bodies, and local authorities

- Individuals or HUFs with a business turnover above ₹1 crore in the previous financial year

- Individuals or HUFs with professional receipts above ₹50 lakh in the previous financial year

Not required to deduct TDS:

- Individuals or HUFs below the prescribed turnover limits

- Payments made for purely personal purposes

Where Section 194J applicability does not arise, Section 194M may still apply to certain payments.

Payments Covered Under Section 194J

Section 194J covers five broad categories of payments:

|

Type of Payment

|

Examples

|

|

Professional fees

|

Doctors, lawyers, CAs, architects

|

|

Technical services

|

Consultancy, IT support

|

|

Royalty

|

Patents, trademarks, copyrights

|

|

Non-compete fees

|

Restrictive business agreements

|

|

Director remuneration

|

Sitting fees, commission

|

Professional services under 194J include professions notified by the Central Board of Direct Taxes (CBDT) under Section 44AA, covering medicine, law, architecture, accountancy, interior design, advertising, technical consultancy, information technology, and film artistry. The CBDT has also notified sportspersons, coaches, commentators, physiotherapists, umpires, and sports columnists.

Technical services under Section 194J refer to managerial, consultancy, or technical expertise provided by humans. As clarified by the Supreme Court, machine-rendered or automated services do not qualify as technical services under this section.

What Is the TDS Rate Under Section 194J?

The Section 194J TDS rate varies based on the nature of the payment:

|

Nature of Payment

|

TDS Rate

|

|

Fees for technical services

|

2%

|

|

Payments to call centres

|

2%

|

|

Royalty for cinematographic films

|

2%

|

|

Royalty other than cinematographic films

|

10%

|

|

Professional services

|

10%

|

|

Director remuneration, sitting fees, or commission

|

10%

|

|

Cases where PAN (Permanent Account Number) is not provided

|

20%

|

The threshold limit is ₹50,000 per financial year for most payments. Director payments have no minimum threshold.

Threshold Limit Under Section 194J

The Section 194J threshold limit is ₹50,000 per financial year for each payment category. TDS applies only when payments to a payee exceed this 194J limit. The threshold is calculated separately for professional fees, technical services, and royalties.

For example, consider the following payments made by a company:

|

Payment Type

|

Amount

|

TDS Applicable

|

|

Professional fees

|

₹30,000

|

No

|

|

Technical services

|

₹25,000

|

No

|

In this example, no TDS is deducted because neither category individually crosses ₹50,000.

When Should TDS Be Deducted Under Section 194J?

TDS under Section 194J must be deducted at the earlier of two events:

- When the payment is credited in the books of accounts

- When the actual payment is made

After deduction, the TDS must be deposited with the government within the prescribed timelines.

|

Payment Type

|

Non-Government Deductors

|

Government Deductors

|

|

Payment made before 1 March

|

Within 7 days from the end of the month

|

Within 7 days from the end of the month

|

|

Payment made in March

|

30 April

|

30 April

|

Failure to deduct or deposit TDS within the specified timelines may attract interest and penalties.

Professional Services vs Technical Services Under Section 194J

|

Basis

|

Professional Services

|

Technical Services

|

|

Nature

|

Specialised professional expertise

|

Technical or consultancy support

|

|

TDS Rate

|

10%

|

2%

|

|

Examples

|

Lawyer, doctor, chartered accountant

|

IT consultant, management adviser

|

|

Requirement

|

Profession notified by CBDT

|

Human technical expertise

|

Exemptions Under Section 194J

The following situations are exempt from TDS for professional fees or technical service fees:

- Total payment does not exceed ₹50,000 in a financial year

- The payer is an individual or HUF not liable for tax audit

- The payment is made for personal use

- The service does not qualify as a professional or technical service under Section 194J

However, director remuneration does not qualify for Section 194J exemption, as TDS applies regardless of the payment amount.

How To Calculate TDS Under Section 194J?

TDS under Section 194J is calculated using a simple formula:

TDS = Payment Amount × Applicable 194J TDS Rate

The applicable rate depends on the type of service provided.

|

Type of Payment

|

Amount

|

TDS Rate

|

TDS Amount

|

|

Professional fees

|

₹80,000

|

10%

|

₹8,000

|

|

Technical services

|

₹60,000

|

2%

|

₹1,200

|

If the payee does not provide PAN details, TDS must be deducted at 20% instead of the normal rate.

Due Date for Depositing TDS Under Section 194J

TDS deducted under Section 194J must be deposited within the prescribed timelines. Businesses must also file quarterly TDS returns and issue Form 16A to the deductee.

|

Compliance Requirement

|

Due Date

|

|

TDS deposit (April–February)

|

7th day from the end of the month

|

|

TDS deposit for March

|

30th April

|

|

Quarterly TDS return

|

Quarterly basis

|

|

Form 16A issuance

|

Within prescribed quarterly timelines

|

Penalty for Non-Compliance Under Section 194J

Failure to comply with Section 194J can result in penalties, interest, and disallowance of expenses.

Common consequences include:

- Interest at 1% per month for non-deduction of TDS

- Interest at 1.5% per month for late deposit

- Disallowance of 30% of the expense claimed

Maintaining proper TDS compliance not only helps businesses avoid penalties and notices but also strengthens financial credibility. Consistent tax compliance and organised financial records may support smoother evaluation when applying for external financing solutions such as a business loan.

Accurate accounting records, timely TDS filings, and properly maintained invoices can also make it easier for enterprises to prepare the business loan documents required during the application and verification process.

Common Mistakes Businesses Make Under Section 194J

Businesses often make mistakes while applying Section 194J, leading to penalties and notices.

Common errors include:

- Wrong classification between professional and technical services

- Applying incorrect 194J TDS rates

- Treating ₹50,000 as a combined threshold

- Delaying TDS deduction or deposit

- Ignoring PAN verification requirements

Latest Updates Related to Section 194J for FY 2026

A few important developments to be aware of:

- The TDS threshold under Section 194J has been increased from ₹30,000 to ₹50,000, as per the Budget 2025 update.

- From 1 April 2026, the Income Tax Act, 1961, has been replaced by the Income Tax Act, 2025, where Section 194J-related provisions now fall under Section 393.

- TDS filing for FY 2026-27 now uses numeric payment codes (1001–1067) instead of old section references like 194J.

- 194JB of the Income Tax Act and 194JB TDS related to professional service fees continue at a 10% TDS rate under the new system.

Conclusion

Section 194J of the Income Tax Act becomes easier to manage once businesses understand its scope and applicability. It requires TDS deduction on specified professional and technical service payments exceeding Rs. 50,000 in a financial year, with rates of 10% for most professional services and 2% for certain technical services. Payments made to directors are subject to TDS without any minimum threshold limit.

For businesses, timely compliance under Section 194J is important not only for avoiding penalties and disallowance of expenses but also for maintaining smoother financial operations. Effective cash flow management becomes particularly important when taxes are deducted at source on large professional payments. In such situations, an unsecured business loan from SMFG India Credit may help enterprises manage operational or working capital requirements more efficiently while benefiting from competitive business loan interest rates and flexible repayment tenures of up to 60 months*.

It is advisable to use our business loan eligibility calculator before applying to estimate your borrowing capacity and make informed application decisions.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us