A CIF number, or Customer Information File, is a unique identifier assigned to every customer by a bank or financial institution. It allows the institution to store and access all personal details, account information, and transaction history in one place, making transactions faster, more secure, and more personalised.

Your CIF number also simplifies verification for services such as a personal loan, business loan, or two-wheeler loan, and ensures your financial profile remains organised without needing multiple documents each time.

This guide, updated for 2026, explains the CIF number meaning in banks, how to find the CIF number on your account documents, and why it plays a vital role in digital banking today.

Key Takeaways

- CIF number = Customer Information File linked to your banking identity

- Stores personal details and transaction history, aiding efficient data management

- Helps financial institutions verify customers quickly across loan KYC and service requests

What Is CIF? Full Form & Simple Definition

The CIF full form is Customer Information File, and the term refers to the digital record a financial institution maintains for each customer. In simple terms, what a CIF number means can be explained as a unique identifier – typically 8–12 digits or alphanumeric – used to link all your banking information to one profile.

This number helps financial institutions retrieve your account, service history, and personal details instantly whenever needed.

Full Form of CIF Number

The CIF number's full form is Customer Information File. It represents the unique code assigned to every customer in a bank's system, allowing multiple account-related information to be tracked under one profile. This helps streamline verification, service requests, and data management.

Why CIF Number Exists: Purpose & Who Uses It

The purpose of the CIF number is to maintain a unified financial identity for each customer. Instead of storing data separately for multiple accounts, the CIF links all information under a single profile. Here’s why the CIF number is used and who benefits from it:

- Acts as a central repository for savings accounts, fixed deposits, loans, and other products

- Connects KYC records, PAN, Aadhaar, and address proofs for instant verification

- Helps lenders determine product eligibility, such as personal loan, business loan, or credit card offers

- Enables faster service processing across branches and digital channels

- Supports risk evaluation, including TRV/CRV calculations and credit behaviour patterns

- Plays a role in fraud monitoring, identity verification, and account security

Most financial institutions use encrypted systems to store CIF data, maintaining compliance with data protection and regulatory standards. This ensures customer information remains secure while enabling seamless banking operations.

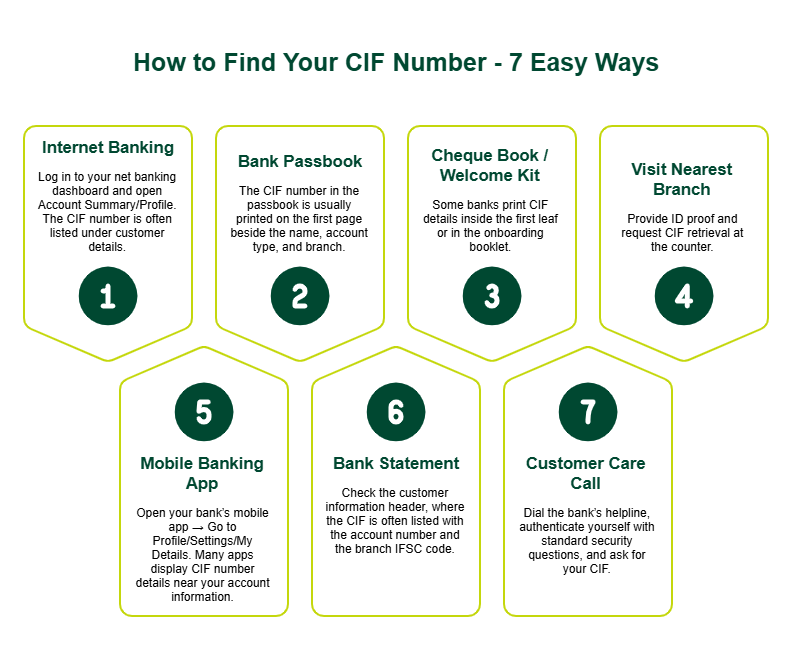

How to Find Your CIF Number: 7 Easy Ways

If you’re unsure how to get a CIF number, most institutions provide multiple offline and digital methods to retrieve it.

- Internet Banking

Log in to your net banking dashboard and open Account Summary/Profile. The CIF number in the bank account is often listed under customer details.

Tip: If not visible, check the “Account Details” or “Personal Profile” tab.

- Mobile Banking App

Open your bank’s mobile app → Go to Profile/Settings/My Details. Many apps display CIF number details near your account information.

Tip: Some apps show it under “Manage Account” or “Digital ID”.

- Bank Passbook

The CIF number in the passbook is usually printed on the first page beside the name, account type, and branch.

Tip: If not printed, request a reissued passbook at the branch.

- Bank Statement (E-Statement or Printed)

Check the customer information header, where the CIF is often listed with the account number and the branch IFSC code.

Tip: Search PDF with the keyword “CIF” for quick scanning.

- Cheque Book / Welcome Kit

Some banks print CIF details inside the first leaf or in the onboarding booklet.

Tip: Look under “Customer Information File Number” or “Client ID”.

- Customer Care Call

Dial the bank’s helpline, authenticate yourself with standard security questions, and ask for your CIF.

Tip: Keep PAN/registered mobile ready for verification.

- Visit Nearest Branch

Provide ID proof and request CIF retrieval at the counter.

Tip: This is ideal if digital access is unavailable or details are unclear.

What Does the CIF Number Contain?

A Customer Information File stores all essential banking data under one profile. While fields may vary slightly across institutions, the table below summarises the most common CIF details you’ll find linked to your identity:

|

CIF Contains

|

Examples of Linked Data

|

|

Personal details

|

Name, date of birth, residential address

|

|

Identity documents

|

PAN, Aadhaar, voter ID, other verified KYC proofs

|

|

Account information

|

Savings account, current account, linked FD/RD

|

|

Transaction history

|

Deposits, withdrawals, digital payments

|

|

Loan relationships

|

Personal loan, business loan, mortgage

|

|

Investment products

|

Fixed deposits, recurring deposits, Demat/Mutual fund linkage

|

|

Digital banking activity trails

|

Login records, OTP authentication logs (where supported)

|

|

KYC & risk flags

|

KYC completion status, risk assessment category

|

These CIF details help a bank verify customers quickly and manage multiple accounts under a single, unique identifier.

Advantages of CIF Number: Operational & Customer Benefits

The benefits of the CIF number extend to both banks and customers, improving efficiency, security, and service experience. Because the CIF acts as a unique identifier, it allows systems to recognise a customer instantly and pull complete records from one place. Here’s why the CIF number's importance is high in day-to-day banking:

- Potentially faster verification and reduced processing time for service requests

- All accounts, loans, and deposits linked to one financial profile

- Easier credit product eligibility checks

- Supports compliance, audit trails, and regulated data handling

- Helps prevent identity mismatch and reduces fraud risk

- Allows easier account portability across branches or digital platforms

- Streamlines documentation for loans and KYC updates

- Saves customers from repeating information for every service request

[Check Your CIF Now]

CIF vs IFSC Code vs Account Number

Many users confuse these three banking identifiers, but each serves a different role. The table below highlights the difference between CIF and IFSC code, along with account number comparisons for clarity.

|

Feature / Aspect

|

CIF Number

|

IFSC Code

|

Account Number

|

|

Purpose

|

Customer identification within bank systems

|

Branch identification for fund transfers

|

Identifies a specific customer account

|

|

Scope

|

Entire customer financial profile

|

Routing transfers between banks

|

Single savings/current account only

|

|

Confidentiality

|

Private, not shared publicly

|

Publicly used for payments

|

Sensitive – kept secure

|

|

Use Cases

|

KYC, service requests, loan processing

|

NEFT / RTGS / IMPS online transfers

|

Deposits, withdrawals, EMIs, transactions

|

|

Example Format

|

Typically 8–12 digits/alphanumeric

|

Usually 11 characters (e.g. ABCD0123456)

|

Varies by bank (length + pattern differ)

|

Notes:

- IFSC is typically used for RTGS/NEFT/IMPS payments

- CIF is used internally by banks for customer identity

- Account number links to only one account, while CIF links to all associated banking products

How CIF Number Works

Understanding how CIF works becomes easier when viewed as a lifecycle from creation to continuous updates across your banking journey. Below is a simple step-flow of the CIF lifecycle:

- Generated at Account Opening

When you open your first bank account, the system creates a CIF number and stores your basic profile information.

- Linked to All Future Accounts & Products

Any new savings account, fixed deposit, loan, or credit card is mapped to the same CIF, allowing a unified view of your transaction history.

- Updated After KYC or Personal Changes

When you update PAN, Aadhaar, email, mobile, or address, the CIF record is refreshed to reflect your latest verified details.

- Used in Loan & Product Origination

During a personal loan, business loan, or deposit request, banks fetch risk scores, past behaviour, income details, and compliance flags through the CIF file.

- Supports Risk Monitoring & Analytics

Banks analyse repayment patterns, spending behaviour, and account activity through CIF-linked records for fraud control and decisioning.

Multiple CIF Records?

Sometimes customers hold more than one CIF due to older accounts or branch migrations. Banks can merge them on request. If you suspect duplicates, ask your branch to consolidate for smoother access and faster service.

Conclusion & Next Steps: Find Your CIF & Keep It Secure

Your CIF number is a core unique identifier that keeps your banking history and profile organised under one secure file.

Key takeaways:

- CIF helps financial institutions manage personal details, accounts, loans and transaction history under one profile

- It supports verification, compliance, and faster product processing

- You can retrieve it through net banking, mobile app, passbook, branch visits, or customer care

- Keep your CIF confidential to prevent unauthorised access

If you’re exploring loan solutions to meet your goals, SMFG India Credit offers personal loans of up to Rs. 30 lakhs* at competitive interest rates.

Check your eligibility, estimate monthly repayment using our personal loan EMI calculator, and apply online today!

For higher funding requirements, you can explore our business loan and Loan Against Property options.

If you require help with CIF number access or financing queries, our support team will be happy to assist you.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us