The Aadhaar Enabled Payment System (AePS) is changing how millions of Indians access financial services. For small businesses, rural retailers, and customers in underserved areas, AePS offers a simple, secure way to conduct financial transactions using just an Aadhaar number and a fingerprint.

This article covers the AePS meaning, how it works, the transactions it supports, and why it matters for small businesses and financial inclusion across India.

What Is the Aadhaar Enabled Payment System (AePS)?

The Aadhaar Enabled Payment System is a biometric banking system that allows customers to perform financial transactions using their Aadhaar number and biometric verification. Developed by the National Payments Corporation of India (NPCI), it was designed to expand access to digital banking in rural and semi-urban areas where traditional financial infrastructure is limited or unavailable.

Through AePS, customers can withdraw cash, check balances, transfer funds, and access other financial services without needing a card or internet connection.

What Is AePS?

Aadhaar Enabled Payment System is a payment framework developed by NPCI that processes transactions through Aadhaar verification and biometric authentication. It works by linking a customer's bank account to their Aadhaar number. Once linked, the customer can carry out transactions at any AePS-enabled micro ATM or through a banking correspondent, without visiting a branch.

AePS is interoperable across all financial institutions (FIs), meaning a customer of any FI can use any AePS-enabled point to access their account securely, regardless of which institution they hold their account with.

How AePS Works

The AePS works through a straightforward process of Aadhaar verification and biometric authentication. When a customer initiates a transaction, they provide their Aadhaar number and the name of their FI at an AePS-enabled micro ATM or banking correspondent outlet. The system then prompts for biometric input, typically a fingerprint scan, which is verified against the UIDAI database in real time.

Once authenticated, the transaction is processed through the NPCI network, and the customer's linked bank account is debited or credited accordingly. The entire AePS transaction process takes only a few seconds and generates a printed receipt confirming the transaction details for the customer.

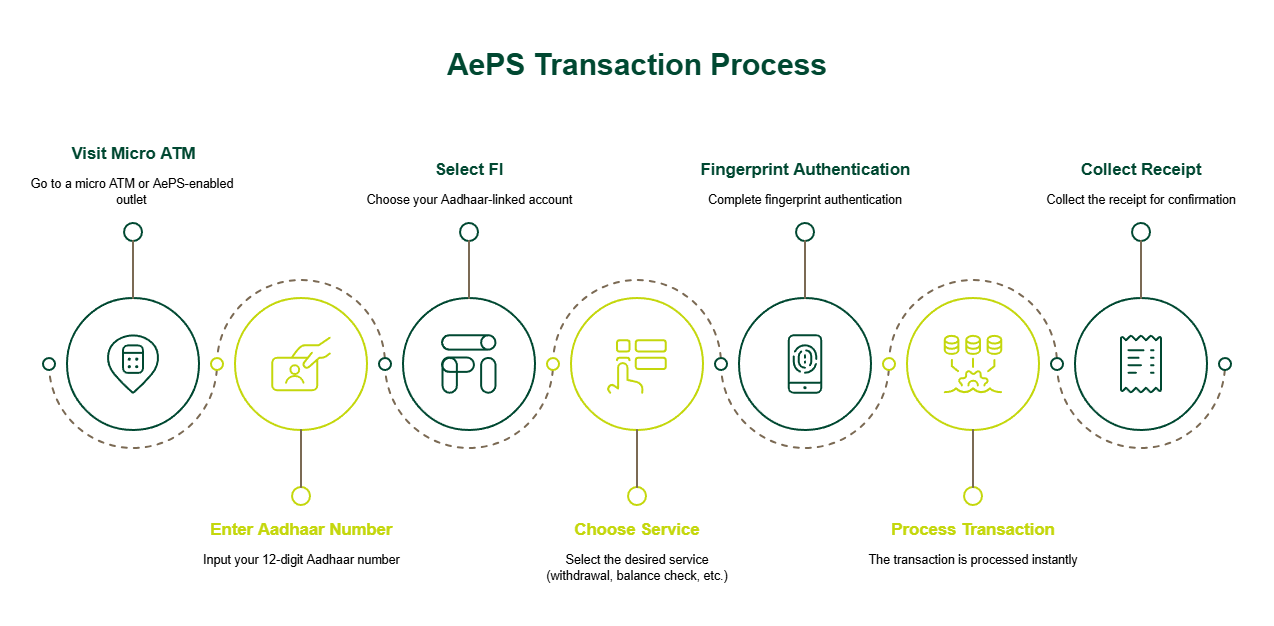

Step-by-Step AePS Transaction Process

Here is how a standard AePS transaction process works from start to finish:

- Visit a micro ATM or an AePS-enabled outlet.

- Enter your 12-digit Aadhaar number.

- Select your FI (Aadhaar-linked account).

- Choose the service (withdrawal, balance check, transfer, mini statement).

- Complete fingerprint authentication.

- The transaction is processed instantly.

- Collect the receipt for confirmation.

Types of Transactions Supported by AePS

The AePS services cover a range of essential financial functions that make it a comprehensive tool for everyday financial needs:

- AePS cash withdrawal: Withdraw cash from your Aadhaar-linked account without a debit card.

- AePS balance inquiry: Check your account balance using biometric authentication.

- Mini statement: View recent transactions instantly.

- Cash deposit: Deposit cash into your linked account via a banking correspondent.

- Fund transfer: Transfer money securely to another Aadhaar-linked account.

AePS Transaction Services

Here is a simplified overview of the AePS services India supports through the Aadhaar Enabled Payment System:

|

Service Type

|

What It Does

|

Requires Aadhaar Linking

|

|

AePS Cash Withdrawal

|

Withdraw cash without a debit card

|

Yes

|

|

AePS Balance Inquiry

|

Check account balance instantly

|

Yes

|

|

Mini Statement

|

View recent transaction history

|

Yes

|

|

Cash Deposit

|

Deposit cash via banking correspondent

|

Yes

|

|

Fund Transfer

|

Transfer funds to another Aadhaar-linked account

|

Yes

|

All AePS micro ATM transactions follow the same biometric authentication process, making every transaction equally secure and accessible. These features of AePS make it one of the most inclusive digital banking tools available in India, particularly for communities that have historically lacked access to formal financial services and infrastructure.

Benefits of AePS for Small Businesses

AePS for small businesses delivers practical advantages that go well beyond simple payments:

- No card infrastructure needed: No need to invest in POS machines or card systems.

- Serves unbanked customers: Helps customers without debit cards or smartphones.

- Additional income stream: Earn commission on every AePS transaction.

- Builds community trust: Becomes a reliable local financial service point.

- Faster service: Biometric transactions are quick, reducing wait times.

Tip: For small enterprises looking to expand operations alongside offering AePS services, external financing, such as a business loan, may help fund additional working capital or basic setup requirements. Many lenders offer competitive business loan interest rates, which can help reduce the overall cost of borrowing.

AePS for Rural and Micro Enterprises

Rural banking has always faced the challenge of physical distance from lender branches. AePS financial inclusion in India addresses this directly by turning local shop owners and agents into financial service points for their entire community. A rural retailer registered as a banking correspondent can offer cash withdrawals, balance inquiries, and fund transfers locally, earning a commission in the process.

This model does not require a stable internet connection or expensive hardware, making it practical even in the most remote locations. For micro enterprises operating in villages and small towns, AePS remove the need for customers to travel long distances just to access basic financial services, which builds loyalty and foot traffic for the business at the same time.

Security and Authentication in AePS

Security is built into every step of the AePS. Each transaction requires biometric authentication, meaning the customer must be physically present and provide their fingerprint for the transaction to go through. This fingerprint is verified in real time against the UIDAI database, making it virtually impossible for someone else to access your official account through AePS.

The NPCI network that processes all AePS transactions uses multiple layers of encryption. Unlike password- or PIN-based systems, biometric banking systems are at lesser risk of being compromised by phishing or card skimming, giving users in rural banking communities a level of security that traditional systems often cannot match.

Challenges and Limitations of AePS

Despite its strengths, AePS comes with a few practical limitations worth knowing. Biometric authentication can fail for customers with worn fingerprints, which is common among manual labourers and elderly users. Privacy concerns around Aadhaar data and biometric records remain a consideration for some users. The daily transaction limit on AePS also restricts the volume a business or customer can process in a single day, which can be a constraint for higher-volume outlets.

Conclusion

The Aadhaar Enabled Payment System (AePS) has emerged as a key driver of digital banking and financial inclusion in India, particularly for small businesses and rural communities. By enabling secure, cardless transactions through simple biometric authentication, it bridges critical access gaps and brings essential banking services closer to underserved populations. For small businesses, AePS not only enhances customer reach but also creates new revenue opportunities.

To support your cash flow as you explore new opportunities, SMFG India Credit offers unsecured business loans of up to Rs. 75 lakhs*. Eligible enterprises can avail of competitive interest rates and flexible tenures of up to 60 months*.

Review the business loan documents required and apply online today.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us