Upgrading technology is one of the biggest challenges small businesses face in India. The Credit-Linked Capital Subsidy Scheme for MSME units addresses this directly by providing government-backed financial support for purchasing modern plant and machinery. Under the CLCS-TUS scheme for MSMEs, eligible businesses can access an upfront capital subsidy to reduce the cost of technology adoption and stay competitive in a demanding market. This article covers everything you need to know about the MSME technology upgradation subsidy, from eligibility to the application process.

Introduction to CLCS-TUS Scheme

The Credit-Linked Capital Subsidy Scheme for MSMEs is a government subsidy programme that supports MSME modernisation by helping businesses upgrade their machinery and adopt the latest technologies through institutional finance. It combines three earlier schemes, the Credit Linked Capital Subsidy Scheme (CLCSS), the Technology and Quality Upgradation Support (TEQUP), and the Technology Acquisition and Development Fund (TADF), into a single unified framework.

This consolidation was undertaken to broaden the scope of the technology upgradation subsidy in India and make government subsidies for MSMEs more accessible and impactful.

What Is the CLCS-TUS Scheme?

The Credit-Linked Capital Subsidy and Technology Upgradation Scheme (CLCS-TUS) is an MSME government support scheme implemented under the Ministry of MSME. It is designed to help micro and small enterprises reduce the cost of production and improve product quality by introducing well-established and improved technologies in approved sub-sectors and products.

The scheme operates on a demand-driven basis, meaning there is no upper limit on annual subsidy disbursal. It supports both existing MSEs looking to modernise and new units setting up with approved technology, making it one of the most practical MSME technology upgrade schemes available.

Objectives of the CLCS-TUS Scheme

The Credit-Linked Capital Subsidy Scheme for MSME units was built around a clear set of goals:

- Promote technology upgrades in micro and small enterprises through institutional credit

- Lower production costs by enabling modern industrial machinery adoption

- Improve product quality and market competitiveness

- Drive MSME modernisation across 51 approved sub-sectors

- Prioritise support for women entrepreneurs

- Provide capital subsidy access via primary lending institutions

Key Features of the CLCS-TUS Scheme

The MSME capital subsidy scheme comes with several features that make it practical for small businesses:

- 15% upfront capital subsidy on eligible credit for technology upgrades

- Subsidy applicable on loans up to ₹1 crore

- Demand-driven scheme with no annual subsidy cap

- Covers 51 approved sub-sectors

- Implemented through various eligible financial institutions

Eligibility Criteria for CLCS-TUS Scheme

The CLCS-TUS eligibility criteria cover a broad range of business types. Here is who can apply:

- Must be a micro or small enterprise under the msmed act, 2006

- Eligible entities: sole proprietorships, partnerships, cooperatives, societies, private limited companies, and LLPs

- LLPs and companies must be registered under their respective Acts

- Must have a valid udyog aadhaar Number (UAN) or Udyam Registration Number (URN)

- Investment should be in new plant and machinery only (no second-hand or in-house equipment)

- Businesses must fall under the 51 approved sub-sectors/products

- Loan must be sanctioned by an eligible Primary Lending Institution (PLI)

Subsidy Amount and Financial Assistance

The MSME capital subsidy provided under this scheme is 15% of the actual cost of new plant and machinery purchased for technology upgradation. This is an upfront subsidy, meaning it is credited at the start rather than reimbursed over time. The maximum loan amount eligible for this capital subsidy for MSME units is Rs. 1 crore.

The subsidy amount is calculated based on the actual purchase cost of the eligible machinery inducted by the unit. This MSME modernisation subsidy directly reduces the overall loan burden, making technology investment financially manageable for small businesses.

Technology Upgradation Covered Under the Scheme

The Credit-Linked Capital Subsidy Scheme for MSME covers the purchase of new plant and machinery for modernising the manufacturing process and equipment used in rendering services. The upgradation must fall within one of the 51 approved sub-sectors or products notified by the Ministry of MSME.

The focus is on the induction of well-established and improved technologies that reduce production costs and improve output quality. The MSME machinery upgrade subsidy applies to manufacturing units as well as service-oriented MSEs. Second-hand machinery, imported used equipment, and in-house fabricated machinery are explicitly excluded from the capital subsidy scheme for MSMEs.

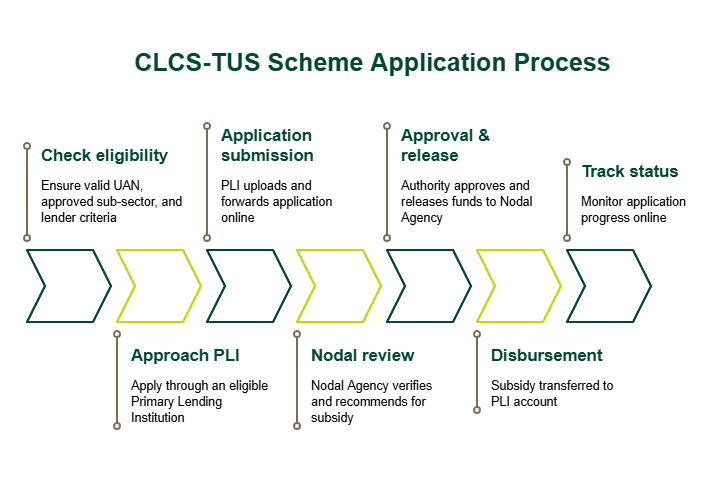

How to Apply for the CLCS-TUS Scheme

The CLCS-TUS application process typically involves the following steps:

- Check eligibility: Ensure a valid UAN, an approved sub-sector, and meet lender criteria.

- Approach PLI: Apply through an eligible Primary Lending Institution (PLI).

- Application submission: PLI uploads and forwards your application online.

- Nodal review: Nodal Agency verifies and recommends for subsidy.

- Approval & release: Authority approves and releases funds to the Nodal Agency.

- Disbursement: Subsidy is transferred to your PLI account.

- Track status: Applicants can monitor application progress for the MSME capital subsidy scheme online.

Documents Required for CLCS-TUS Application

The following are standard requirements based on the Credit-Linked Capital Subsidy Scheme for MSMEs framework:

- Valid udyam registration certificate confirming MSE status

- Project report detailing the technology upgradation plan

- Quotations or invoices for the new plant and machinery

- Bank account details and financial statements

- LLP agreement or Certificate of Incorporation for applicable business structures

Benefits of the CLCS-TUS Scheme for MSMEs

The MSME capital subsidy scheme delivers tangible advantages for small businesses:

- Reduces the upfront cost of modern machinery

- Lowers loan burden with 15% capital subsidy

- Improves production efficiency and quality

- Enhances competitiveness against larger players and imports

- Enables modernisation without affecting working capital

- Encourages inclusive growth with priority for women entrepreneurs

Challenges or Limitations of the Scheme

Despite its benefits, the Credit-Linked Capital Subsidy Scheme for MSMEs has a few practical limitations. Many MSEs are unaware that the scheme exists or find the application process procedurally complex. The restriction to 51 approved sub-sectors means businesses in other industries cannot access the capital subsidy scheme for MSMEs.

In such cases, enterprises may consider alternative financing options such as a business loan to fund technology upgrades or expansion. With many lenders offering competitive business loan interest rates and a relatively simple online application process involving minimal documentation, this route can provide quicker access to funds without the constraints of sector-specific eligibility. This makes it a practical option for enterprises looking to invest in growth without bureaucratic delays.

Conclusion

The Credit-Linked Capital Subsidy Scheme for MSMEs is one of the most practical government subsidy programmes available to small businesses looking to modernise. By providing a 15% upfront capital subsidy on institutional credit for new plant and machinery, it directly reduces the financial burden of technology upgradation.

However, its reach may be limited due to relatively low awareness and procedural complexities involved in the application process.

If you’re exploring financing options for your enterprise, SMFG India Credit offers business loans of up to Rs. 75 lakhs*, without any collateral requirements. Use our business loan eligibility calculator to assess your borrowing potential and apply online. Feel free to contact us for more details.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us