In India, your ability to access affordable loans significantly depends on your credit history. Over 79% of loans are approved for individuals with a CIBIL score of 750 or above , as per the credit bureau’s insights. However, many borrowers are unaware that even hard enquiries – especially if repeated across multiple lenders in a short period – can negatively impact their credit score.

This guide covers everything you need to know about how to remove loan enquiries from CIBIL reports, when such entries can actually be removed, and how to safeguard your credit profile going forward.

Related Read: What Is the Role of CIBIL Score in the Loan Application Process?

What Is a CIBIL Enquiry?

A CIBIL enquiry is recorded whenever a lender accesses your credit report, typically when you apply for a loan or credit card.

There are two types of credit enquiries:

Soft enquiries occur when you check your own credit score or when a lender performs a pre-approved offer check. These do not affect your credit score.

Hard enquiries, on the other hand, are triggered by actual loan or credit card applications and can negatively impact your score. Understanding the difference between soft vs hard CIBIL enquiries is essential to gauge their impact on your creditworthiness.

If you're planning to apply for credit products such as a personal loan, it's wiser to first use online tools like a personal loan EMI calculator and an eligibility calculator. This approach helps you apply more strategically and avoid triggering multiple hard enquiries by applying directly to several lenders.

Removal of Loan Enquiry from a CIBIL Report

You may be able to remove a loan enquiry from your CIBIL report in the following two cases:

- Unauthorised Enquiry: Your credit report was accessed without your consent.

- Data Error: The enquiry was added due to an error by the credit bureau or a mismatch in details.

Steps to remove loan enquiries from CIBIL:

- Get Your CIBIL Report: Identify any incorrect or suspicious enquiries.

- Raise a Dispute: Go to the Dispute Resolution section on CIBIL’s website and submit your complaint.

- Wait for Resolution: CIBIL will investigate your dispute and, if found valid, remove the incorrect enquiry from your report.

Note: If the enquiry is valid, it cannot be removed. It can remain on your report for 1 to 2 years. In this case, the best course of action is to maintain timely repayments, limit unnecessary credit applications, and manage your credit utilisation wisely.

How to Check CIBIL Credit Reports?

Here’s how to check your CIBIL report in order to identify any recent or unauthorised loan enquiries:

- Register or log in to your official CIBIL account.

- Request your most recent credit report and score.

- In the Enquiry Information section, review the credit report for loan enquiries. This helps you spot any errors or unauthorised access to your credit data.

How to Increase Your CIBIL Score?

Once you’ve understood how to remove a loan enquiry in CIBIL or raised a dispute, your next focus should be on rebuilding or improving your credit score:

- Pay all EMIs and credit card bills on time.

- Maintain a credit utilisation ratio below 30%.

- Keep a balanced credit mix – a combination of secured (e.g., auto loan) and unsecured (e.g., personal loan) credit.

- Monitor your CIBIL report regularly and correct inaccuracies promptly.

Impact of a Hard Enquiry on Credit Score

The hard enquiry impact on credit score is typically minor but worth noting:

- Minor Drop: Each hard enquiry may slightly lower your score, usually by a few points.

- Short-Term Effect: The dip is usually temporary and fades if you continue to manage credit responsibly.

- Multiple Enquiries: However, several enquiries in a short time can signal credit stress and reduce your score more noticeably.

Why Does a Credit Score Drop After a Hard Enquiry?

A hard enquiry lowers your credit score slightly because it indicates you're actively seeking credit. This may be perceived as a risk signal by lenders, especially if multiple applications are made within a short span.

Each enquiry suggests a potential increase in your debt load, which could affect your ability to repay. However, the impact of a single hard enquiry is typically small and temporary. On the other hand, repeated hard enquiries over a short period can lead to a more noticeable decline in your credit score.

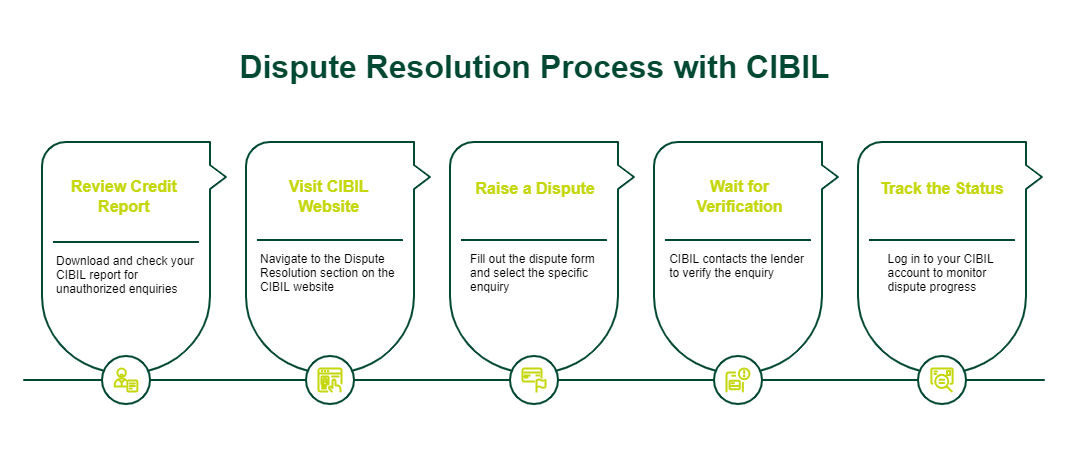

How to Raise a Dispute with CIBIL to Remove a Loan Enquiry from Your Credit Report?

Here’s the detailed process for how to delete a loan enquiry in CIBIL:

Step 1: Review Your Credit Report

Download your CIBIL report and carefully check for any loan enquiries you did not authorise.

Step 2: Visit the CIBIL Website

Go to the official CIBIL website and navigate to the Dispute Resolution section.

Step 3: Raise a Dispute

Fill out the dispute form, select the specific enquiry you want corrected, and upload any supporting documents (if applicable).

Step 4: Wait for Verification

CIBIL will contact the lender to verify whether the enquiry was valid. The process may take up to 45 days.

Step 5: Track the Status

You can log in to your CIBIL account to track the progress of your dispute.

Tips to Prevent Credit Score Decline After a Loan Enquiry

- Space Out Applications: Avoid applying for multiple loans or credit cards within a short period.

- Use Pre-Qualification: Before applying, check if you’re eligible for any pre-approved loan offers that don't trigger hard enquiries.

- Maintain Good Credit Habits: Always pay your EMIs and credit card bills on time, keep your credit utilisation ratio low, and maintain a balanced credit mix.

Conclusion

While a single loan enquiry may not drastically affect your CIBIL score, multiple hard enquiries in a short span can raise red flags for lenders. By understanding the difference between soft and hard enquiries, regularly monitoring your credit report, and disputing any unauthorised entries, you can protect and improve your credit health. If you're planning to apply for a loan, take a strategic approach – compare options, check your eligibility, and avoid unnecessary applications.

Looking for a hassle-free borrowing experience? SMFG India Credit offers personal loans of up to INR 30 lakhs* for eligible applicants with a CIBIL score of 750 and above. Check your eligibility and apply online today to enjoy competitive interest rates, flexible repayment tenures, and minimal documentation.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us