A CIBIL suit filed status appears in a credit report when a lender takes legal action against a borrower due to prolonged non-payment of dues. Understanding the suit filed meaning in CIBIL reports is important because it can negatively affect future loan approvals, borrowing terms, and overall financial credibility. A CIBIL suit filed entry may also lower your credit score and remain visible in your report for a significant period if not resolved properly. However, borrowers can take corrective steps such as repaying outstanding dues, settling disputes with lenders, and raising rectification requests to improve their credit profile over time.

What Is a CIBIL Suit Filed?

A suit filed status in a credit report indicates that a lender has initiated legal proceedings against a borrower due to unpaid loan dues or prolonged default. In simple terms, a suit filed means the matter has moved beyond reminders and recovery follow-ups, and the lender has chosen to take legal action to recover the outstanding amount.

A suit filed in the CIBIL report generally appears when a borrower has not repaid a loan, credit card bill, or other credit obligation despite repeated notices from the lender. The credit information company, TransUnion CIBIL, records this status based on information shared by financial institutions.

Such an entry can negatively affect a borrower’s creditworthiness because lenders may view it as a sign of higher repayment risk. It may also reduce the chances of getting future personal loan or credit cards approved, as financial institutions carefully review repayment history before extending credit.

Why Does a Suit Filed Status Appear in a CIBIL Report?

A suit filed status usually appears when a borrower fails to repay a loan or credit card dues for a prolonged period despite repeated reminders and recovery efforts by the lender. In such situations, the lender may initiate legal proceedings, and the account may be reported as a CIBIL suit in the borrower’s credit history.

Common reasons for a suit filed status include:

- Continuous missed EMIs on loans

- Loan defaults over an extended period

- Unpaid credit card outstanding amounts

- Disputed or incomplete loan settlements

- Unresolved repayment issues with lenders or financial institutions

- Ignoring recovery notices or legal communication from the lender

How Does a CIBIL Suit Filed Impact Your Credit Score?

A suit filed entry can significantly affect a borrower’s financial profile because lenders may consider it a sign of serious repayment issues. The effect of a suit filed on a credit score can often be long-lasting, especially if the dues remain unresolved for an extended period. It can reduce the chances of getting approved for future loans, credit cards, or higher credit limits.

A suit filed status may lead to:

- A drop in the borrower’s credit score

- Lower chances of loan or credit card approval

- Reduced trust from lenders during credit assessment

- Difficulty accessing future borrowing facilities, especially unsecured credit

- Higher personal loan interest rates, or rates for other specific credit products, due to increased risk perception

Types of Suit Filed Status in a CIBIL Report

Different repayment-related remarks can appear in a credit report depending on the borrower’s repayment history and the lender’s recovery actions. While all negative remarks affect creditworthiness to some extent, each status reflects a different stage or nature of default. Understanding different terms like suit filed, wilful default, written off, and settled can help borrowers take corrective action more effectively.

|

Possible CIBIL Report Suit Filed Status

|

Meaning

|

|

Suit filed

|

Legal action has been initiated by the lender to recover unpaid dues.

|

|

Wilful default

|

The borrower has the ability to repay but intentionally avoids repayment.

|

|

Written off

|

The lender has treated the loan as a loss in its books after prolonged non-payment.

|

|

Settled

|

The borrower has paid part of the outstanding amount as a negotiated settlement.

|

How to Check if a Suit Is Filed in Your CIBIL Report?

Borrowers can check whether a suit has been filed by reviewing their latest CIBIL report online. The report contains account-wise repayment details, overdue amounts, and lender-reported status remarks. Any suit-related information is usually shown against the specific loan or credit account.

Steps to check it:

- Visit the official TransUnion CIBIL website.

- Log in or create an account using your PAN and personal details.

- Download or view your latest credit report.

- Check each loan or credit card account carefully.

- Look for remarks such as suit filed, written-off, settled, or wilful default.

- Contact the lender if any entry appears incorrect.

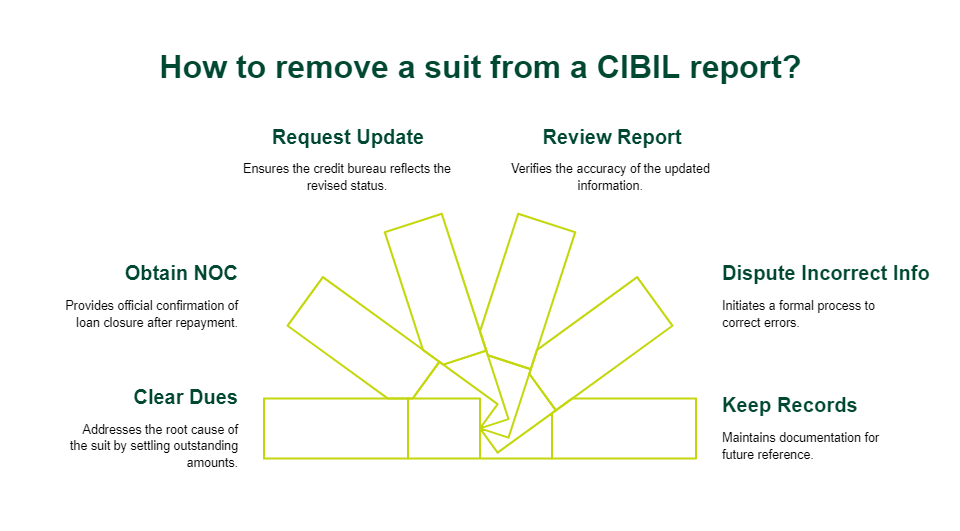

How to Remove a Suit Filed in a CIBIL Report?

Borrowers wondering how to remove a suit filed in CIBIL records should first understand that the process usually begins with resolving the outstanding dues linked to the account. Once the payment or settlement is completed, the lender may update the account status with the credit bureau. In some cases, borrowers may also need to raise a dispute if incorrect information continues to appear in the report. Proper documentation and regular follow-up are important during the CIBIL suit removal process.

Steps that may help:

- Clear the pending dues or settle the outstanding amount with the lender.

- Obtain a No Objection Certificate or loan closure confirmation after repayment.

- Request the lender to update the revised status with the credit bureau.

- Review the updated credit report after a few weeks.

- Raise a request through the CIBIL dispute resolution process if incorrect information remains visible.

- Keep copies of payment receipts and settlement documents for future reference.

How Long Does It Take to Remove a Suit Filed Status?

The time required to update or remove a CIBIL suit filed status can vary depending on the lender’s reporting cycle and the nature of the dispute. After repayment or settlement, lenders may take a few weeks to update the revised account status with the credit bureau. If a borrower raises a dispute regarding incorrect information, the verification and correction process may take additional time. Borrowers should regularly check their updated credit report and maintain all repayment and settlement documents for reference.

Can a CIBIL Suit Filed Be Removed Without Repayment?

In most cases, a suit filed status cannot be removed unless the outstanding dues are repaid or formally settled with the lender. However, removal may be possible if the entry appears due to incorrect reporting, identity mismatch, duplicate accounts, or outdated information. In such situations, borrowers can raise a dispute with the lender and the credit bureau for verification and correction. If the claim is found to be inaccurate, the status may be revised or removed from the credit report.

Difference Between Suit Filed, Written-off, and Settled Status

Suit filed, wilful default, and written off statuses carry varying levels of severity and can affect future borrowing differently. Understanding these differences can help borrowers evaluate their credit position more clearly.

|

Status

|

Meaning

|

Impact on Credit Score

|

Loan Approval Chances

|

|

Suit Filed

|

Legal action initiated for the recovery of dues

|

Severe negative impact

|

Significantly reduced

|

|

Written-Off

|

Loan treated as a loss by the lender

|

High negative impact

|

Low chances of approval

|

|

Settled

|

Partial repayment accepted by lender

|

Moderate to high impact

|

May affect future approvals and repayment terms

|

Tips to Improve Credit Score After a CIBIL Suit Filed Case

Recovering from a negative credit remark takes time and consistent financial discipline. Borrowers looking to improve their CIBIL after suit filed cases should focus on building a stable repayment record and reducing overall credit risk. Regular monitoring of credit reports can also help identify errors or delayed updates from lenders.

Some practical steps include:

- Pay EMIs and credit card bills on time without delays

- Reduce outstanding debt gradually and avoid over-borrowing

- Maintain low credit utilisation on credit cards

- Avoid applying for multiple loans within a short period

- Check credit reports regularly for incorrect entries

- Use tools such as a personal loan EMI calculator to plan repayments more effectively

Common Mistakes Borrowers Make While Resolving a CIBIL Suit Filed Case

Many borrowers delay corrective action or fail to complete the documentation process properly while resolving repayment disputes. Such mistakes can prolong the negative impact on their credit profile and delay future borrowing opportunities.

Common mistakes include:

- Ignoring repayment notices or legal communication from lenders

- Opting for partial settlements without written confirmation

- Failing to obtain a No Dues Certificate or a loan closure document

- Not checking whether the lender updated the revised status with the credit bureau

- Neglecting to monitor updated credit reports regularly

Latest Updates Related to CIBIL Reporting and Suit Filed Status

Recent measures introduced by the Reserve Bank of India have made credit reporting more frequent and transparent. Credit bureaus and lenders are now expected to update borrower information every 15 days instead of longer reporting cycles followed earlier. This helps borrowers track changes in repayment behaviour, credit score movements, and suit filed status updates more quickly. Faster reporting may also help consumers identify incorrect entries earlier and raise disputes without unnecessary delays.

Conclusion

A CIBIL suit filed status indicates that a lender has initiated legal action due to unresolved repayment issues or prolonged loan default. Such an entry can negatively affect a borrower’s credit score, loan eligibility, and future borrowing opportunities. However, timely corrective action, responsible repayment behaviour, proper documentation, and regular credit monitoring can help improve the overall credit profile over time.

Borrowers planning future financial requirements should also assess repayment capacity carefully before taking fresh credit. Tools such as a personal loan eligibility calculator and an EMI calculator can support better financial planning.

For eligible borrowers seeking structured financing solutions, SMFG India Credit offers personal loans of up to Rs. 30 lakhs* with competitive interest rates. Check out the personal loan documents required and apply online today.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us