Many individuals today must balance several financial responsibilities while working with a fixed or limited income. Effective financial goals planning becomes important when you need to manage expenses, savings, and long-term commitments at the same time. Managing money with a limited income requires careful decision-making and a clear understanding of priorities. By focusing on budgeting for multiple goals, individuals can allocate resources more thoughtfully and avoid financial strain.

With the right approach to financial planning and spending, it becomes possible to address both immediate needs and future objectives in a structured and manageable way.

What Are Financial Goals?

Financial goals refer to the specific objectives you set for your money, helping guide how you save, spend, and invest over time. In personal finance planning, these goals are often categorised as short-term, medium-term, or long-term. For example, short-term goals may include building an emergency fund, while long-term goals may involve retirement planning or purchasing a home.

Effective multiple financial goals planning requires careful financial priorities management so that limited income is allocated wisely. Following practical money management can help individuals stay focused on achieving their financial targets.

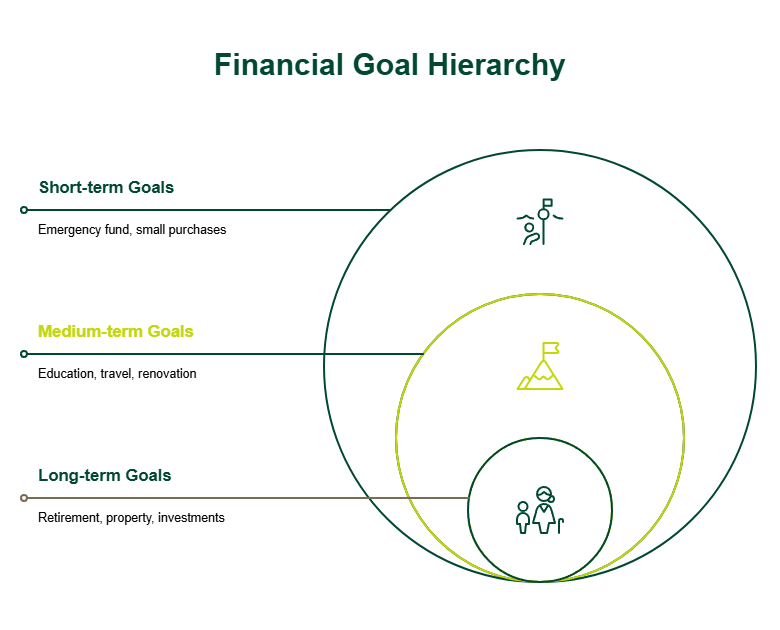

Types of Financial Goals

Understanding different types of monetary objectives can help you organise your financial planning more effectively. A good financial goal planning guide often divides objectives into short-term, medium-term, and long-term categories based on the time required to achieve them. Each category may require a different savings plan or funding approach depending on the urgency and amount needed. In certain situations, you may also consider options such as a personal loan to address immediate financial needs while continuing to work towards longer-term objectives.

Common types of financial goals include:

- Short-term goals: Building an emergency fund or saving for small purchases

- Medium-term goals: Funding higher education, travel, or home renovation

- Long-term goals: Retirement planning, buying property, or long-term investment planning

Short-Term Financial Goals

Short-term financial goals are objectives that can usually be achieved within a year. These may include building an emergency fund, saving for travel, or clearing smaller debts. Reaching such goals requires following practical saving money strategies and consistent monthly budgeting. By careful expense tracking and setting aside a portion of income regularly, you can work towards these targets more efficiently. Including short-term goals as part of overall financial planning can also help create better control over day-to-day finances.

Medium-Term Financial Goals

Medium-term financial goals usually take around three to five years to achieve. These may include buying a car, funding higher education, or making home improvements. Reaching such goals requires a clear budget allocation strategy, especially when practising financial planning with limited income.

In some situations, individuals may consider loans to meet immediate funding needs while keeping long-term savings intact. Before borrowing, it is important to review factors such as personal loan interest rates and repayment capacity to ensure the plan remains financially manageable.

Long-Term Financial Goals

Long-term financial goals usually take several years or even decades to achieve. These may include retirement planning, purchasing a home, or building a portfolio of long-term investments. Achieving such goals requires consistent budget planning and disciplined saving over time. It is also important to practise responsible debt management so that liabilities do not interfere with future financial objectives. Along with regular savings, thoughtful investment planning can help individuals gradually build wealth and stay on track towards achieving their long-term financial goals.

Strategies to Manage Multiple Financial Goals

Managing several financial goals at the same time can be challenging, especially when income is limited. However, with disciplined financial planning and clear priorities, it becomes easier to balance immediate needs with long-term objectives. Simple money management tips, such as following the 50–30–20 rule to divide income between needs, wants, and savings, can help maintain structure. If you are managing repayments as well, tools like a personal loan EMI calculator can help with effective monthly budget planning. These practices are particularly useful when focusing on saving with a low income.

Practical strategies to manage multiple financial goals include:

- Automating savings to ensure consistent contributions

- Tracking expenses regularly to understand spending patterns

- Reducing unnecessary or discretionary spending

- Exploring additional income sources where possible

- Prioritising essential financial goals before secondary ones

Common Mistakes to Avoid While Managing Financial Goals

Discipline and careful financial planning are essential when managing multiple goals. However, certain mistakes can make it harder to stay on track. Ignoring basic practices such as regular expense tracking or responsible debt management may lead to financial imbalance over time. Being aware of common pitfalls can help you adjust your approach and maintain steady progress towards your goals.

Common mistakes to avoid include:

- Setting unrealistic or overly ambitious financial goals

- Ignoring the importance of building an emergency fund

- Overspending on non-essential expenses

- Failing to track monthly spending consistently

- Taking on excessive debt without a clear repayment plan

Conclusion

Balancing several financial goals with a limited income requires discipline, clear priorities, and consistent savings habits. By practising structured financial planning, tracking expenses, and focusing on the most important goals first, you can gradually build financial stability while working towards both short-term and long-term objectives.

If you need additional support to meet certain financial needs, apply for an SMFG India Credit personal loan of up to Rs. 30 lakhs*, with interest rates starting from just 13%* per annum. Check your borrowing capacity in advance using our personal loan eligibility calculator to make informed application decisions. Feel free to contact us for tailored guidance.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us