The MUDRA loan interest rate plays a crucial role for micro-entrepreneurs looking for affordable credit under the Pradhan Mantri MUDRA Yojana (PMMY). Introduced by the Government of India, the scheme extends financial support to small business owners without the need for security or third-party guarantees, making credit more accessible nationwide. Over the years, the PMMY loan has empowered millions of MSMEs and SMEs, helping them meet working capital requirements or invest in innovation and business expansion.

Whether a borrower needs funding through the Shishu, Kishore, Tarun, or Tarun Plus categories, understanding the Pradhan Mantri MUDRA loan interest rate and related costs helps in making informed decisions.

This article covers key Pradhan Mantri MUDRA Yojana loan details, PMMY interest rate considerations and explores how a collateral-free business loan can serve as a practical alternative for growing enterprises.

What Is Pradhan Mantri Mudra Yojana (PMMY)?

The Pradhan Mantri Mudra Yojana (PMMY) was launched in 2015 to strengthen the backbone of India’s small business ecosystem. By offering 4 tiers of credit through MUDRA loan scheme categories, the scheme supports Micro, Small and Medium Enterprises (MSMEs) and the larger segment of Small and Medium Enterprises (SMEs) engaged in manufacturing, trading, and services.

The scheme was created under the umbrella of the Micro Units Development and Refinance Agency (MUDRA).

The objective of PMMY is simple: to strengthen small business funding by offering accessible funds for working capital, equipment purchases, business expansion, and start-up activities. The initiative complements national programs such as Startup India, enabling entrepreneurs to secure reliable financing under the MUDRA loan for small businesses.

Must Read: Credit Guarantee Fund for Micro Units (CGFMU) Scheme Explained

MUDRA Loan Yojana Details: Interest Rate, Loan Amount, Tenure, Processing Fee

Below are the essential MUDRA loan details, including PM MUDRA loan interest rates in 2025, loan amount, loan tenure, and processing fee components typically associated with PMMY loans.

|

Parameter

|

Details

|

|

Loan Amount

|

Up to ₹20 lakhs (Shishu, Kishore, Tarun, and Tarun Plus)

|

|

Interest Rate

|

Varies by lender, but reasonable; influenced by risk assessment, business type, and borrower profile

|

|

Loan Tenure

|

Up to 5 to 7 years

|

|

Processing Fee

|

MUDRA loan processing fee is typically waived for the Shishu category, and is at the lender's discretion for others

|

|

Collateral

|

Collateral-free loan under PMMY

|

|

Purpose

|

Working capital, business expansion, equipment, inventory, services

|

Essentially, lenders define the MUDRA Yojana interest rate, making it essential for applicants to compare options before applying.

Pradhan Mantri MUDRA Yojana Loan Interest Rate

Loans under PMMY are categorised to meet diverse business needs.

1. Shishu MUDRA Yojana

- Up to ₹50,000

- Ideal for new entrants and micro-entrepreneurs

- The Shishu MUDRA Yojana interest rate aims to support early-stage businesses and individuals starting out as small vendors, traders, or service providers.

2. Kishore MUDRA Yojana

- ₹50,001 to ₹5 lakhs

- Suitable for enterprises seeking moderate expansion

- The Kishore MUDRA loan interest rate varies based on the borrower’s experience, financial profile, and cash-flow stability.

3. Tarun MUDRA Yojana

- Above ₹5 lakhs to ₹10 lakhs

- Ideal for established micro businesses

- The Tarun MUDRA loan interest rate generally reflects higher ticket sizes but remains competitive under PMMY guidelines.

4. Tarun Plus MUDRA Yojana

- Above ₹10 lakhs to ₹20 lakhs

- Ideal for businesses aiming for sustained growth and large-scale expansion

- The Tarun Plus MUDRA loan interest rate may be determined based on the borrower’s repayment track record, creditworthiness, and long-term business potential.

These categories collectively support diverse entrepreneurs, making the MUDRA Yojana interest rate and loan limits flexible and business-friendly.

Features of Pradhan Mantri Mudra Yojana Loans

The salient features of MUDRA loans include:

- Collateral-free loans are available, reducing entry barriers.

- Categorised funding as per business stage.

- Support for working capital and term loans.

- Designed for MSMEs and micro-enterprise development.

- Competitive PMMY scheme interest rate bands depending on lender assessment.

- Widely available across participating Non-Banking Financial Companies (NBFCs), Microfinance Institutions (MFIs), and other financial institutions.

- Offers specialised options for women entrepreneurs.

- Supports the broader financial ecosystem through the refinance scheme provided by MUDRA.

Factors Affecting Mudra Loan Interest Rates

While PMMY defines the framework, individual lenders determine the final PM MUDRA loan interest rates. Key influencing factors include:

- Credit score and repayment discipline

- Type of business (trading, services, manufacturing)

- Loan amount and category (Shishu, Kishore, Tarun, Tarun Plus)

- Loan tenure and repayment capacity

- Market conditions and lender policies

- Accuracy of documentation and strength of the application profile

Strong MUDRA loan eligibility criteria alignment increases the chances of securing competitive rates.

Must Read: Minimum CIBIL Score for Business Loans

Tips to Get Mudra Loans at Affordable Interest Rates

Borrowers exploring how to get low MUDRA loan interest rates in 2025 can consider the following steps:

- Maintain a robust credit score and consistent repayment history.

- Present a clear, professionally structured business plan.

- Evaluate lenders offering PMMY loans across financial institutions and NBFC

- Ensure accuracy and completeness of all documents needed for MUDRA loans.

- Explore specialised MUDRA loans for women entrepreneurs.

- Strengthen business cash-flow management and financial records.

- Understand eligibility norms before applying to avoid delays.

Mudra Yojana Schemes and Variants

PMMY includes multiple schemes addressing diverse business needs:

- Micro Enterprise Loans: Suitable for traders, artisans, and self-employed individuals.

- Mahila Udyami Yojana: Designed for women business owners seeking options such as the MUDRA Yojana loan for women.

- MUDRA Card: A digital, debit-card-like facility for MUDRA loan borrowers.

- Equipment Finance: Supports machinery and equipment purchases.

- Mudra Refinance Scheme: Offers refinance support to institutions through MUDRA.

Documents Required for MUDRA Loan

The MUDRA loan documents required typically include:

- Identity and address proof

- Business proof or registration documents

- Quotation for equipment (if applicable)

- Financial statements for higher-category loans

- Recent passport-size photographs

- Completed application form

Additional eligibility documents may be requested depending on lender policy, business type, loan category, and borrower profile.

Mudra Loan Eligibility

Eligibility norms typically include:

- The individual must be an Indian citizen.

- The applicant should be at least 18 years old when submitting the application.

- The enterprise must fall under the micro or small business category.

- The business should be involved in income-generating activities, excluding activities directly related to agriculture, such as farming or cultivation.

- A good credit history and compliance with lender-specific criteria may be required.

From Whom Can You Avail Loans Under the MUDRA Scheme?

Wondering where to apply for a MUDRA loan? PMMY loans are available from a wide network of MUDRA lending institutions, offering convenience, accessibility, and service quality. These institutions operate under the regulatory framework of the Reserve Bank of India (RBI) to ensure secure, compliant, and responsible lending practices.

These typically include: public sector banks, private sector banks, Regional Rural Banks (RRBs), Non-Banking Financial Companies (NBFCs), Microfinance Institutions (MFIs), and Small Finance Banks (SFBs).

Types of Borrowers Eligible Under Mudra Yojana

Common borrowers under PMMY fall into various micro-enterprise categories across trading, manufacturing, and services.

Eligible businesses or entities under MUDRA Yojana typically include:

- Individuals

- Proprietary concerns

- Partnership firms

- Private limited companies

- Public companies

- Any other legal entities

Features and Benefits of MUDRA Card

The MUDRA Card is an innovative financial tool designed to give micro-entrepreneurs flexible and convenient access to funds. Functioning much like a debit or prepaid card, it allows borrowers to withdraw money in small amounts as needed instead of taking the entire sanctioned loan at once.

This flexibility is especially valuable for managing working capital for small businesses, where daily operational expenses such as purchasing inventory, paying suppliers, or handling urgent service requirements can fluctuate frequently. By enabling controlled and need-based spending, the Mudra Card helps business owners maintain financial discipline, track expenditure efficiently, and avoid unnecessary borrowing costs. It also eliminates the need for repeated branch visits, making it a practical and user-friendly option for micro-entrepreneurs who require quick access to funds to support their operations.

Comparison of Shishu, Kishore, Tarun, and Tarun Plus Loans

|

Category

|

Loan Amount

|

Target Borrower

|

Primary Use

|

|

Shishu

|

Up to ₹50,000

|

New micro-businesses

|

Startup needs, inventory

|

|

Kishore

|

₹50,001–₹5 lakh

|

Growing enterprises

|

Expansion, machinery

|

|

Tarun

|

₹5 lakh–₹10 lakh

|

Established units

|

Scaling operations

|

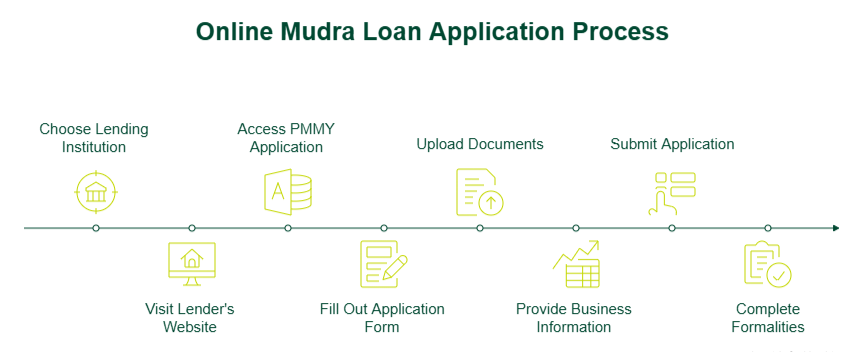

How to Apply for Mudra Loan Online

To apply for a MUDRA loan online, follow these steps:

- Choose a preferred lending institution that offers PMMY loans.

- Visit the lender’s website and access the PMMY application section.

- Fill out the PMMY loan details form.

- Upload the required documents to proceed with the MUDRA loan application process.

- Provide business and financial information.

- Submit the application for verification.

- Complete any additional formalities required by the lender.

This MUDRA Yojana loan process facilitates convenient digital access to funding.

Why Consider a Business Loan as an Alternative?

While a business loan under MUDRA Yojana can be beneficial, some enterprises eventually require a larger scale of financing for expansion, equipment upgrades, inventory, or new projects. In such cases, a standard business loan can be a more suitable option, as lenders generally offer higher loan amounts, flexible repayment tenures, and competitive business loan interest rates based on the borrower’s credit profile and business stability.

Before applying, entrepreneurs can use tools like a business loan eligibility calculator and a business loan EMI calculator to make informed borrowing decisions.

Conclusion

The Pradhan Mantri MUDRA loan interest rate plays a central role in enabling micro-entrepreneurs to access affordable financing. With collateral-free loan structures, flexible loan categories, and widespread institutional availability, the MUDRA loan for the self-employed remains one of India’s most empowering financial initiatives.

For those exploring financing options for enterprise growth, SMFG India Credit offers collateral-free business loans of up to Rs 75 lakhs*. Review your business loan eligibility and apply online today with minimal business loan documents for a hassle-free experience.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us