Post Office savings schemes are government-backed investment options that help you save money safely while earning steady returns. Many of these Post Office tax-saving schemes also qualify for benefits under Section 80C of the Income Tax Act. Offered by India Post under the supervision of the Government of India, these schemes combine safety, predictable growth, and tax relief. If you are looking for low-risk Post Office investment schemes, this can be a practical place to begin.

What Are Post Office Tax Saving Schemes?

The Post Office tax saving scheme meaning refers to selected savings options offered by India Post that allow you to claim a tax deduction under Section 80C of the Income Tax Act. In simple terms, a tax-saving Post Office scheme helps you reduce your taxable income while keeping your money secure.

However, not every Post Office scheme qualifies.

The most popular Post Office tax-saving schemes include Public Provident Fund (PPF), National Savings Certificate (NSC), and the 5-Year Time Deposit. These are part of the wider Post Office tax-saving investment category and are designed for disciplined, long-term saving.

Why Should You Choose the Post Office Tax-Saving Scheme?

If you prefer stability over market-linked risk, Post Office tax-saving schemes can suit you well. They are considered a generally safe tax-saving investment because they are backed by the Government of India.

Here is why many people choose them:

- Capital protection with sovereign backing

- Predictable, government-declared returns

- Eligibility for tax deduction under Section 80C

- Suitable for senior citizens, salaried individuals, and risk-averse investors

For conservative savers, these Indian Post Office savings schemes can offer clarity and peace of mind.

How Does the Post Office Tax-Saving Scheme Actually Work?

To understand how the Post Office savings scheme plans work, you first choose a qualifying programme. You invest either as a lump sum or in instalments, depending on the scheme rules. Each scheme typically has a fixed lock-in period, which means you cannot withdraw the money freely before maturity.

Interest may be compounded annually or quarterly, depending on the scheme. For example, Public Provident Fund (PPF) compounds annually, while some deposits may follow quarterly compounding. Over time, this affects your maturity value.

At maturity, you receive the principal plus interest. In certain schemes, the maturity amount enjoys tax exemption, while in others, only the principal qualifies for a tax deduction under Section 80C.

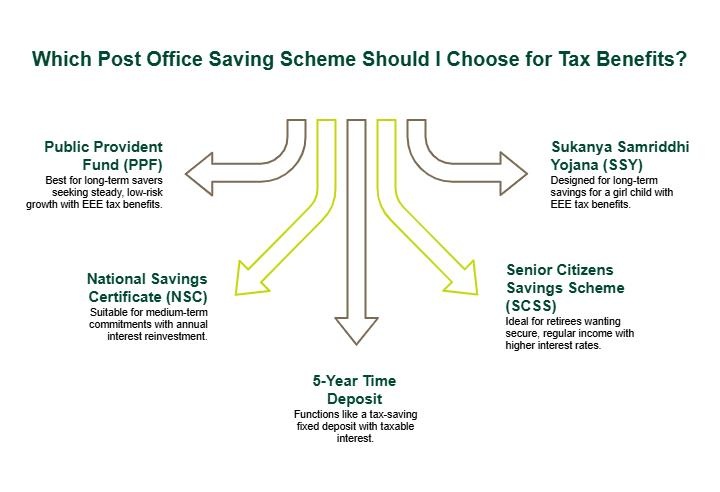

Types of Post Office Saving Schemes for Tax Benefits

When you look at the Post Office tax-saving schemes list, you will find several options such as:

1. Public Provident Fund (PPF)

The Public Provident Fund (PPF) is one of the most popular Post Office saving schemes. It has a 15-year tenure. Contributions up to Rs. 1.5 lakh per financial year qualifies for a tax deduction under Section 80C.

PPF follows the EEE (Exempt-Exempt-Exempt) category, meaning contributions, interest earned, and the maturity amount are tax-exempt.

The Public Provident Fund (PPF) suits long-term savers looking for steady, low-risk growth.

2. National Savings Certificate (NSC)

The National Savings Certificate (NSC) has a 5-year tenure. It qualifies under the Post Office tax-saving schemes under 80C. Interest is compounded annually and reinvested. While the principal gets a tax deduction, interest is taxable at maturity.

It works well if you want a medium-term commitment.

3. 5-Year Time Deposit

The 5-Year Time Deposit functions like a tax-saving fixed deposit. Interest is taxable, but the principal gets a tax deduction. The Post Office savings scheme interest rate for Time Deposit is subject to change as notified by the Government of India.

4. Senior Citizens Savings Scheme (SCSS)

The Senior Citizens Savings Scheme (SCSS) is designed for retirees and generally offers higher interest rates compared to standard deposits. It qualifies for Post Office tax-saving schemes under Section 80C benefits.

Interest earned is fully taxable, and TDS applies if interest exceeds the prescribed annual limits.

The Senior Citizens Savings Scheme (SCSS) is suitable if you want a secure, regular income post-retirement.

5. Sukanya Samriddhi Yojana (SSY)

The Sukanya Samriddhi Yojana (SSY) is a dedicated Post Office scheme for women, specifically created for the financial security of a girl child. This Post Office Sukanya Samriddhi Yojana offers one of the highest small-savings interest rates and provides full tax exemption on maturity, placing it in the EEE category.

If you are planning long-term savings for your daughter, this Post Office scheme for women is designed precisely for that purpose.

Comparative Study of Post Office Schemes for Tax Exemption

|

Scheme

|

Tenure / Lock-in Period

|

Tax Deduction (Section 80C)

|

Tax Exemption on Interest / Maturity

|

|

Public Provident Fund (PPF)

|

15 years

|

Yes

|

Yes - Full exemption (EEE category)

|

|

National Savings Certificate (NSC)

|

5 years

|

Yes

|

Partial - Interest is taxable, but reinvested interest qualifies for 80C

|

|

5-Year Time Deposit

|

5 years

|

Yes

|

No - Interest fully taxable

|

|

Senior Citizens Savings Scheme (SCSS)

|

5 years

|

Yes

|

No - Interest taxable; TDS applies above limits

|

|

Sukanya Samriddhi Yojana (SSY)

|

21 years

|

Yes

|

Yes - Full exemption (EEE category)

|

How to Apply for Tax-Saving Schemes in the Post Office?

If you are wondering how to apply for a Post Office savings scheme, the process is simple.

- Visit your nearest Post Office branch.

- Fill the application form for the chosen Post Office tax-saving schemes.

- Submit KYC documents, including Aadhaar and PAN.

- Deposit the investment amount through cash, cheque or authorised electronic transfer.

You may also use India Post’s banking services for limited online features. The Post Office savings account online opening option is offered in select cases, and some services can be managed through the India Post portal or mobile apps.

Who Should Apply for the Post Office Tax-Saving Schemes?

If you are unsure who should invest in Post Office schemes, here are the profiles that commonly benefit from them:

- Salaried individuals planning their annual tax savings under the Section 80C limit

- Senior citizens looking to earn stable returns through SCSS

- Parents considering a Post Office scheme for women, such as SSY, for their daughter

- Risk-averse investors who prefer secure, non-market-linked products

What Are the Documents Required to Open a Post Office Savings Account?

To start with any of the Post Office savings schemes, you typically need:

- Filled application form

- Identity proof

- Address proof

- Aadhaar

- PAN

- Passport-size photographs

Once your KYC is completed, you may open a basic savings account and even opt for a Post Office monthly savings scheme, depending on eligibility. The Post Office savings account interest rate is applicable only to regular savings accounts and is reviewed periodically by the Government of India.

How Does the Post Office Scheme Compare to Other Options?

When comparing Post Office vs. ELSS or Post Office vs. tax-saving FD, the main difference lies in risk, returns, and predictability.

|

Investment

|

Risk

|

Tax Benefit

|

Returns Type

|

|

Post Office Tax-Saving Schemes

|

Low

|

Yes

|

Fixed

|

|

ELSS

|

Market-linked

|

Yes

|

Variable

|

|

Tax-saving Fixed Deposit

|

Low

|

Yes

|

Fixed

|

|

National Pension System (NPS)

|

Market-linked

|

Yes

|

Market-based

|

The National Pension System (NPS) allows additional deductions beyond Section 80C. A Tax-saving Fixed Deposit in banks is similar to a 5-Year Time Deposit but may offer slightly different interest structures.

What’s the Next Step? How Do You Get Started?

Start by reviewing your annual Section 80C limit of Rs. 1.5 lakh under the Income Tax Act. Decide whether you need long-term growth through the Public Provident Fund (PPF) or a shorter commitment via the National Savings Certificate (NSC).

Be sure to check the latest Post Office savings account interest rate before investing, as these rates are revised periodically. Visit your nearest branch of India Post to explore suitable savings schemes based on your financial goals and risk profile.

Conclusion

Post Office schemes remain a safe tax-saving investment for individuals seeking stability, predictable returns, and government-backed security. With options such as PPF, NSC, SSY, and SCSS, a Post Office tax-saving plan allows you to build long-term discipline while reducing taxable income under Section 80C. These schemes work well for risk-averse savers and anyone looking to strengthen their financial planning with dependable, low-risk instruments.

As you manage routine expenses with investment commitments, a personal loan can help with any short-term cash flow gaps. SMFG India Credit offers unsecured funding of up to Rs. 30 lakhs* at competitive interest rates. Check your eligibility, review the required personal loan documents, and apply online. You can also use the personal loan EMI calculator and eligibility calculator to plan your finances effectively before applying.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us