Section 10 of the Income Tax Act, 1961, lists specific income that is fully or partially exempt from tax. These exemptions cover everything from House Rent Allowance and Leave Travel Allowance to gratuity, agricultural income, and life insurance policy. Understanding these provisions helps you reduce your taxable income legally and plan your finances better.

What Is Section 10 of the Income Tax Act?

Section 10 of the Income Tax Act, 1961, lists incomes that are exempt from tax and are not included in your total taxable income. In simple terms, these incomes are not taxed if certain conditions are met, which means they are excluded from tax calculations from the outset. Understanding these provisions can support effective tax planning for FY 2026–27 and beyond.

Who Can Claim Exemptions Under Section 10?

Not every taxpayer is eligible for every exemption. Broadly, the following categories of people can claim the Section 10 tax exemption:

- A salaried employee receiving HRA, LTA, gratuity, or special allowances

- A retiree with pension or VRS benefits

- A farmer with agricultural income

- An investor in PF or a person availing a life insurance policy

- A member of eligible Scheduled Tribes or approved institutions

Key Exemptions Available Under Section 10 of the IT Act

Section 10 income tax explained across its major sub-sections offers a wide range of relief. This is the Section 10 exemption list most relevant to everyday taxpayers:

|

Section

|

Exemption

|

Key Condition

|

|

10(1)

|

Agricultural income

|

Land must be in India

|

|

10(5)

|

Leave Travel Allowance (LTA)

|

Domestic travel only

|

|

10(10)

|

Gratuity

|

Govt: full, Private: capped

|

|

10(10A)

|

Commuted pension

|

Fully exempt for govt employees

|

|

10(10AA)

|

Leave encashment

|

Govt: full, others can claim exemption up to prescribed limits based on salary and accumulated leave

|

|

10(10C)

|

Voluntary Retirement

|

Exempt up to the prescribed limit

|

|

10(10D)

|

Life insurance policy proceeds

|

Policy maturity proceeds are exempt if the specified premium and policy conditions are satisfied

|

|

10(11)

|

Employee Provident Fund interest

|

Interest earned remains exempt, subject to the prescribed annual contribution threshold

|

|

10(13A)

|

House Rent Allowance (HRA)

|

Exemption is calculated based on HRA received, salary, rent paid, and city of residence

|

|

10(14)

|

Special allowances

|

Certain allowances for official duties (food, internet, research, etc.) are exempt to the extent actual expenses are incurred

|

|

10(15)

|

Savings interest

|

Interest from specified savings certificates and notified securities qualifies for exemption within prescribed limits

|

|

10(23C)

|

Educational and medical institutions

|

Annual receipts ≤ ₹5 crore

|

|

10(34)

|

Dividend income

|

Dividend income of up to Rs. 10,000 received until 31st March 2020 is exempt

|

For the complete list of Section 10 subsections, refer to the Income Tax Department's official portal.

Section 10 Exemptions for Salaried Employees

Salaried employees benefit the most from Section 10 salary exemptions, which reduce taxable income based on specific conditions.

|

Exemption

|

Section

|

Key Rule

|

|

HRA

|

10(13A)

|

Least of HRA received, 50%/40% of salary (Basic + DA), or rent minus 10% of salary (Basic + DA)

|

|

LTA

|

10(5)

|

Only domestic travel expenses allowed within the CTC limit

|

|

Gratuity

|

10(10)

|

Govt: fully exempt; private sector exemption depends on applicable limits and Gratuity Act coverage

|

|

Leave encashment

|

10(10AA)

|

Govt: fully exempt, private: up to ₹25 lakh

|

|

Special allowances

|

10(14)

|

Work-related allowances only

|

|

Children's education allowance

|

10(14)

|

₹3,000/month per child (max 2)

|

|

EPF interest

|

10(11)

|

Up to ₹2.5 lakh annual contribution interest exempt

|

The HRA exemption Section 10 applies only when you are actually paying rent and can provide proof. If you live in your own home, you cannot claim this exemption.

Tip: Understanding Section 10 exemptions can also help you present a clearer income profile when applying for financial products such as a personal loan for salaried employees.

You can further strengthen your application by assessing your borrowing capacity in advance using a personal loan eligibility calculator.

List of Popular Subsections Under Section 10

Here is a quick Sec 10 exemption list of the most commonly referenced sub-sections:

|

Sub-section

|

What it covers

|

|

10(5)

|

Leave Travel Allowance for domestic travel

|

|

10(10D)

|

Life insurance maturity benefits

|

|

10(13A)

|

HRA for salaried employees paying rent

|

|

10(14)

|

Special allowances (food, internet, conveyance, etc.)

|

|

10(10AA)

|

Leave encashment on retirement or resignation

|

|

10(11)

|

Interest on PF and Sukanya Samriddhi Account

|

|

10(23C)

|

Income of eligible educational/medical institutions

|

|

10(38)

|

Long-Term Capital Gains on equity (up to 31 March 2018)

|

|

10AA

|

Profits of SEZ units

|

|

10(26)

|

Income of eligible Scheduled Tribe members

|

Sections 10(5) of the Income-tax Act (Leave Travel Allowance) and 10(10D) (life insurance) are among the most commonly used in practice.

Section 10 Old vs New Tax Regime

|

Exemption

|

Old Regime

|

New Regime

|

|

HRA

|

Available

|

Not available

|

|

LTA

|

Available

|

Not available

|

|

Children’s education allowance

|

Available

|

Not available

|

|

Special allowances

|

Available

|

Not available

|

|

Standard deduction

|

Available

|

Available

|

|

Agricultural income

|

Available

|

Available

|

|

Leave encashment

|

Available

|

Available

|

|

VRS exemptions

|

Available

|

Available

|

|

Gratuity

|

Available

|

Available

|

If you want to claim exempt income under the Income Tax Act provisions, like HRA or LTA, you must actively opt for the old regime while filing your ITR. The Central Board of Direct Taxes has clarified that salaried employees can switch between regimes each year, while business taxpayers can only do so once.

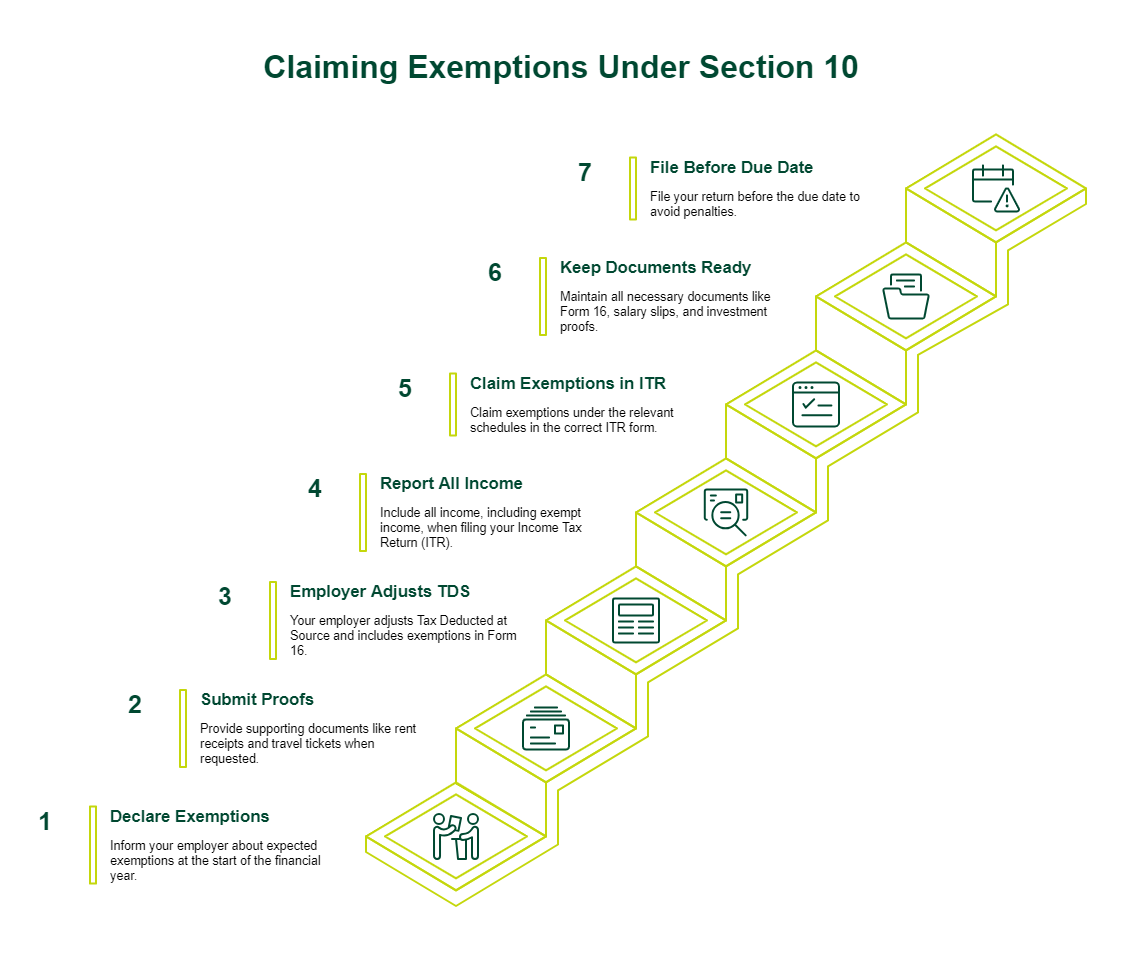

How to Claim Exemptions Under Section 10?

Claiming income exempt under Section 10 correctly ensures you do not pay tax you do not owe. Here is how to go about it:

- Declare expected exemptions (HRA, LTA, etc.) to your employer at the start of the financial year.

- Submit supporting proofs like rent receipts, travel tickets, and bills when requested.

- Employer adjusts TDS and includes exemptions in Form 16.

- Report all income while filing your ITR, including exempt income.

- Claim exemptions under the relevant schedules in the correct ITR form.

- Keep documents ready: Form 16, salary slips, rent receipts, bills, and investment proofs.

- File your return before the due date to avoid penalties.

Once you understand how these exemptions can improve your disposable income, you can use tools such as a personal loan EMI calculator to estimate repayment obligations more effectively before borrowing.

A high and stable income, along with a healthy credit profile, may improve your eligibility for financing and help you secure more favourable borrowing terms, such as a lower personal loan interest rate.

Examples of Section 10 Tax Exemptions

Example 1: HRA Exemption

|

Condition

|

Amount

|

|

Actual HRA received

|

₹3,00,000/year

|

|

50% of basic salary (metro)

|

₹3,00,000/year

|

|

Rent paid minus 10% of basic salary

|

₹1,80,000/year

|

|

Exempt amount (lowest of above)

|

₹1,80,000/year

|

Result: ₹1,80,000 is exempt, and the remaining ₹1,20,000 is taxable.

Example 2: Leave Encashment (Private Sector)

|

Condition

|

Amount

|

|

Actual amount received

|

₹10,00,000

|

|

Statutory limit

|

₹25,00,000

|

|

10 months’ average salary

|

₹6,00,000

|

|

Exempt amount (lowest of above)

|

₹6,00,000

|

Result: ₹6,00,000 is exempt, and the remaining ₹4,00,000 is taxable.

*The above calculations are purely illustrative. Actual exemption amounts may vary depending on salary structure, supporting documents, eligibility conditions, and prevailing rules under the Income Tax Act.

Common Mistakes While Claiming Section 10 Exemptions

- Claiming HRA while living in your own house or not paying rent.

- Choosing the new tax regime and still trying to claim the unavailable Section 10 exemptions.

- Not submitting rent receipts or travel proofs to the employer on time.

- Confusing exemptions (Section 10) with deductions (Section 80C).

- Missing key documents like Form 16, salary slips, rent agreement, or bills.

Latest Updates Related to Section 10 for FY 2026

- The Income Tax Act, 2025, comes into effect from 1st April 2026, while most Section 10 exemptions continue to remain available.

- HRA exemption expanded to 4 more metro cities under new income tax rules.

- The new tax regime is the default; Section 10 exemptions like HRA and LTA require opting for the old regime.

- Food allowance exemption has been revised to ₹1,05,600 per year.

Conclusion

Section 10 of the Income Tax Act, 1961, gives salaried employees, pensioners, and investors a legitimate way to reduce their taxable income by excluding specific receipts from the tax computation. The income tax exemption list under Section 10 covers everything from HRA and LTA to provident fund interest and life insurance proceeds.

If you are planning a major purchase or need additional financial support while managing your tax planning, consider a personal loan of up to Rs. 30 lakhs* from SMFG India Credit.

Check out the personal loan documents required and apply online to benefit from competitive interest rates starting from 13%* per annum.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us