A lien amount refers to a specific sum of money that a bank or financial institution temporarily blocks in a customer's bank account as security against loans, unpaid dues, or any other financial obligation.

Understanding what a lien amount is and its meaning is vital for account holders, especially those with ongoing loans or financial commitments. When a lien is placed, the blocked amount is not available for withdrawal or transfer, which can affect your available funds and daily financial management.

In this article, we’ll explore the lien balance or lien amount meaning in detail and explain its implications for your finances.

What Is a Lien?

A lien is a legal right or claim granted to a lender or creditor over a borrower’s property, asset, or bank funds as security for a debt. In banking, a lien represents the bank’s right to retain possession or control over a portion of your funds in the bank account until the borrower fulfils their repayment obligations.

The lien definition typically refers to this hold placed on assets, often without transferring ownership, but restricting usage or withdrawal.

This lien meaning in banking is particularly important as it affects how freely you can use your funds. For instance, banks may place a lien on your savings or fixed deposit accounts to secure certain loans, ensuring that they have a claim on the funds in case of default.

Understanding the nature of liens helps borrowers recognise their rights and responsibilities and avoid surprises when portions of their account balances are restricted.

What Is the Lien Amount?

The lien amount definition pertains to the exact sum that is blocked or frozen by a financial institution in your account. Depending on the financial institution's policies, this amount can also act as collateral against a loan or outstanding dues.

It is typically calculated based on the loan outstanding, overdue payments, or as agreed upon in your loan contract. This amount remains blocked until the loan is repaid or the lien is legally removed. The lien amount may also vary depending on the borrower’s eligibility, as factors such as income, repayment capacity, and existing liabilities can influence how much security a lender requires.

Lien amount explained simply means that even though your account may show a total balance, a part of that, the lien amount, is restricted from use. For example, if your account balance is ₹70,000 but the lien amount is ₹30,000, you can only use ₹40,000 until the lien is cleared.

The lien amount in banking could be a fixed sum, a percentage of the outstanding loan, or the entire loan amount, depending on the agreement.

Knowing this helps borrowers avoid unexpected fund shortages and plan their finances, including loan repayment, better.

Types of Liens

There are several types of liens that banks, lenders, and authorities use, each with distinct characteristics:

Statutory Lien

Imposed by law, such as tax authorities placing a lien for unpaid taxes. This is an involuntary lien that the account holder does not agree to, but is legally binding.

Consensual Lien

Created by agreement between borrower and lender, such as a mortgage lien, where the lender has a claim on your property until the loan is repaid.

Judgment Lien

Results from a court ruling, allowing creditors to claim funds or property to recover debts.

Mortgage Lien

A specific consensual lien on real estate property securing a mortgage loan.

Each of these legal liens or financial lien types affects individuals differently. For example, voluntary liens like consensual liens are part of the loan agreement, while involuntary liens can be unexpected and must be resolved legally.

For borrowers with ongoing loans, using tools such as a personal loan EMI calculator can help manage repayments effectively, reduce the risk of defaults, and avoid potential financial complications.

Why Banks and NBFCs Apply a Lien Amount?

Depending on their internal policies, banks or NBFCs may place a lien amount on customer accounts to secure loans and ensure timely repayment.

Some reasons why banks place a lien include:

- Security for loans: Ensuring lenders can recover outstanding loan amounts if the borrower defaults.

- Risk management: Blocking funds limits misuse and guarantees partial repayment security.

- Recovery from delinquent accounts: For overdue loan repayments, the lien serves as a collection tool.

- Regulatory compliance: Banks follow prescribed norms to safeguard financial stability and protect depositors.

How to Clear or Remove a Lien Amount From Your Bank Account

The process to remove a lien from an account depends on why the lien was placed in the first place. In most cases, the first step to clear a lien from a bank account is settling the underlying obligation, such as overdue EMIs, credit card dues, or loan instalments. Once the outstanding amount is paid, you can formally request the bank to lift the lien.

You may initiate the request by visiting the branch or through your mobile banking app or online banking portal, depending on the bank’s facilities. After submitting the request, banks usually verify the payment and update your records. It is advisable to check your account statement to confirm when the lien has been removed, and your full account balance is restored for use.

If you are unsure how to remove a lien or the reason for the restriction, contacting customer support can help clarify whether additional documentation or approvals are required. In cases where the lien is court-ordered or imposed by a statutory authority, the bank can remove it only after receiving legal clearance or an official no-objection certificate.

Documents Required to Remove a Lien

The documents needed to remove a lien usually include:

- No-dues certificate or no-objection certificate issued by the financial institution.

- Application form requesting lien removal.

- KYC documents such as identity proof and address proof.

- Account statement showing the lien amount.

These documents for removing a lien serve as proof that your loan repayment or any other obligation is complete and authorise the bank to release the lien. Sometimes, banks may ask for additional papers based on their policies.

Proper submission of papers required for lien removal speeds up the process and helps maintain your financial reputation.

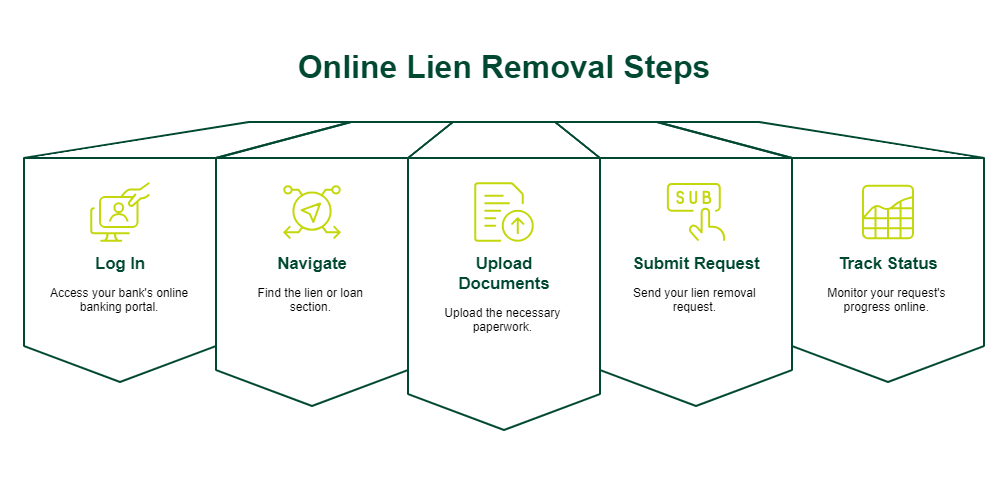

How to Remove a Lien Amount Online

Many banks now offer the facility to remove a lien online through their internet banking portals or mobile banking apps.

This online process for lien removal typically involves:

- Logging into your bank’s online banking portal.

- Navigating to the lien or loan section.

- Uploading the required documents.

- Submitting a lien removal request.

- Tracking the status of your request digitally.

Tips to Prevent a Lien on Your Bank Account

Here are some practical tips to avoid lien on account issues:

- Make timely payments on all your loans and EMIs to prevent default.

- Maintain an adequate account balance to cover any unexpected dues.

- Keep track of loan repayment schedules using reminders or apps.

- Use your mobile banking app regularly to monitor any liens or restrictions.

By preventing liens on bank accounts, you maintain access to your funds and protect your credit score/CIBIL score.

Must Read: How to Improve CIBIL Score

Manage Lien Amount to Keep Your Finances on Track

Effective management of lien amounts involves keeping your finances organised and debt repayments on schedule. Here’s how to manage:

- Plan your budget considering the lien balance meaning, so you know how much money is accessible.

- Pay off any pending obligations promptly to reduce the lien amount and free blocked funds.

- Monitor your account statement regularly via mobile or online banking.

- Use financial tools such as a personal loan eligibility calculator and an EMI calculator to plan future borrowing responsibly.

By actively managing the lien, you ensure financial stability and smooth loan repayment journeys.

Conclusion

Understanding the lien amount definition and its implications is essential for maintaining healthy finances. Always ensure you clear lien amounts promptly to avoid penalties and maintain a strong financial profile.

Timely payment of dues and proactive management will help you avoid lien complications and maintain your creditworthiness.

If you are exploring additional support while managing your finances, consider a personal loan of up to Rs 30 lakhs* from SMFG India Credit. We aim to make your borrowing journey smooth and transparent with simple personal loan eligibility, flexible repayment tenures, and competitive personal loan interest rates. Review the personal loan documents required and apply online today.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us