Intra-state supply in GST refers to the supply of goods or services where the supplier and place of supply are located within the same state or Union Territory. In such cases, CGST and SGST/UTGST are generally applicable. An intra-state transaction under GST differs from inter-state supply, where the supplier and place of supply are located in different states.

What Is Intra-state Supply in GST?

Intra-state supply under GST refers to a transaction where the supplier’s location and the place of supply are situated within the same state or Union Territory. The intra-state meaning in GST mainly determines how taxes are charged on a transaction. In such cases, CGST and SGST applicability generally arises together on the same invoice. The framework and tax structure governing such supplies are regulated under GST laws recommended by the Goods and Services Tax Council to ensure uniform taxation and compliance across India.

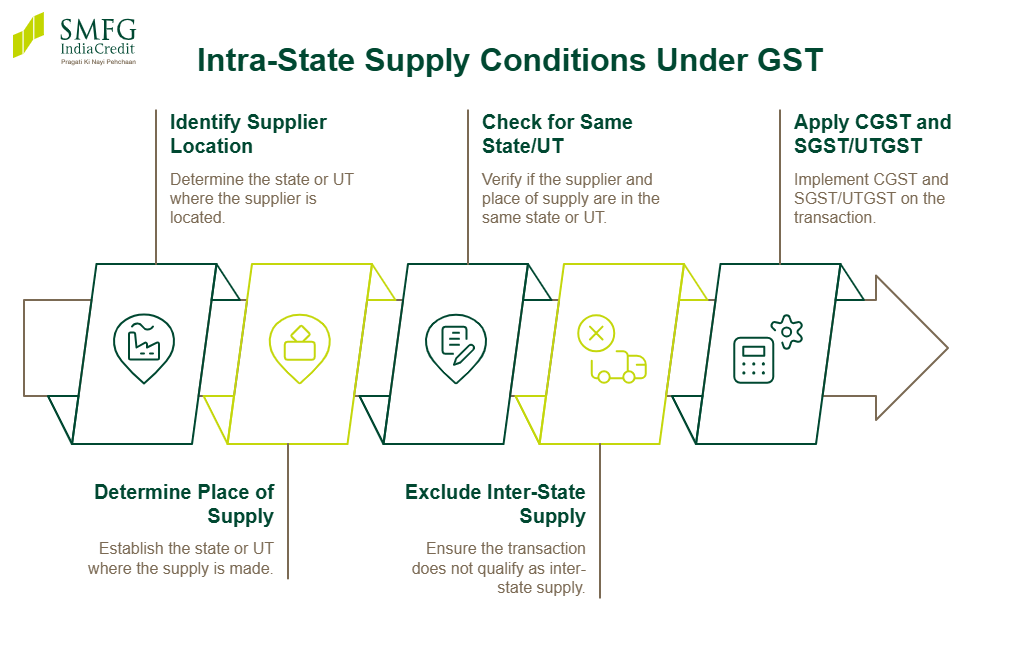

Conditions for Intra-state Supply Under GST

A transaction is generally treated as an intra-state supply when both the supplier’s location and the place of supply in GST are located within the same state or Union Territory. Understanding these intra-state supply conditions is important because they determine whether CGST and SGST/UTGST will apply to a transaction.

Key conditions for intra-state supply include:

- Supplier and place of supply must be in the same state or UT.

- The transaction should not qualify as inter-state supply.

- Applicable GST must generally include CGST and SGST/UTGST.

For example, goods supplied from Pune to Mumbai are generally treated as intra-state supply.

How Is Tax Charged on Intra-state Supply?

In an intra-state transaction, GST is generally divided equally between the Central Goods and Services Tax and the State Goods and Services Tax or Union Territory Goods and Services Tax (UTGST), depending on the location of supply. These intra-state supply rules help distribute tax revenue between the central and state governments while ensuring proper GST compliance for businesses.

|

Transaction Type

|

Applicable Taxes

|

Example

|

|

Supply within same state

|

CGST + SGST

|

Sale within Maharashtra

|

|

Supply within same UT

|

CGST + UTGST

|

Sale within Chandigarh

|

For example, on an 18% GST rate, 9% may be charged as CGST and 9% as SGST.

Understanding intra-state GST calculations may help businesses maintain clearer financial records and estimate operational tax liabilities more accurately. This can be useful while planning working capital requirements or evaluating financing options such as a business loan for expansion or inventory management.

Enterprises applying for financing may also benefit from keeping financial records, such as GST returns and invoices, organised, which can support smoother preparation of the business loan documents required.

Examples of Intra-state Supply in GST

Intra-state GST examples generally involve transactions where both the supplier and the place of supply are located within the same state or Union Territory. In such cases, CGST and SGST/UTGST are charged together on the invoice. These transactions may involve both business-to-business and business-to-consumer supplies.

|

Transaction

|

Type of Supply

|

GST Applicable

|

|

Furniture sold from Pune to Mumbai

|

Goods within Maharashtra

|

CGST + SGST

|

|

Salon services provided in Bengaluru

|

Service within Karnataka

|

CGST + SGST

|

|

Electronics sold within Delhi

|

Consumer goods transaction

|

CGST + SGST

|

|

Restaurant services in Chandigarh

|

Service within UT

|

CGST + UTGST

|

Intra-state Supply vs Inter-state Supply

Understanding the difference between inter-state and intra-state GST is important because the type of supply determines which taxes apply to a transaction. The classification mainly depends on the supplier’s location and the place of supply under GST provisions.

|

Basis

|

Intra-state Supply

|

Inter-state Supply

|

|

Supplier & Place of Supply

|

Located in the same state/UT

|

Located in different states/UTs

|

|

Taxes Charged

|

CGST + SGST/UTGST

|

IGST

|

|

Applicability

|

Local transactions within one state

|

Transactions across states

|

|

Example

|

Goods supplied from Mumbai to Pune

|

Goods supplied from Mumbai to Bengaluru

|

|

Tax Revenue Distribution

|

Shared between Centre and State

|

Collected as IGST by Centre

|

Place of Supply and Its Role in Intra-state Transactions

The place of supply plays an important role in determining whether a transaction qualifies as intra-state or inter-state supply under GST law. GST tax on intra-state supply generally applies only when both the supplier’s location and the place of supply are within the same state or Union Territory. The place of supply concept helps identify the correct GST type applicable to a transaction.

For example, services provided by a consultant in Chennai to a client located in Chennai are generally treated as intra-state supply and taxed accordingly.

When Is a Supply Not Considered Intra-state?

Certain transactions may not be treated as intra-state supply even if they appear to occur within the same state. Under GST law, some special transactions are automatically classified as inter-state supplies based on the nature of supply or the parties involved.

Examples where supply is not considered intra-state include:

- Supplies made to or by Special Economic Zones (SEZs)

- Import of goods or services into India

- Export transactions

- Supplies made to tourists under notified conditions

- Certain transactions specifically treated as inter-state under GST provisions

Benefits of Understanding Intra-state Supply for Businesses

Understanding intra-state supply rules can help businesses apply the correct GST structure on transactions and maintain smoother tax compliance. Proper classification of supplies may also reduce invoicing errors, tax mismatches, and reporting issues during GST return filing or audits.

Key benefits for businesses include:

- Correct charging of CGST and SGST/UTGST

- Improved GST compliance and recordkeeping

- Reduced GST calculation and invoicing errors

- Better accuracy in GST return filing

- Easier reconciliation of tax payments and invoices

Common Mistakes Businesses Make While Determining Intra-state Supply

Businesses may sometimes make errors while determining whether a transaction qualifies as intra-state supply, which can lead to incorrect GST charging and compliance issues. Understanding intra-state supply rules and referring to guidance issued by the Central Board of Indirect Taxes and Customs can help businesses reduce reporting and invoicing mistakes.

Common mistakes businesses should avoid include:

- Confusing supplier location with place of supply

- Charging IGST instead of CGST and SGST/UTGST

- Incorrect GST invoicing and tax classification

- Ignoring special cases such as SEZ transactions

- Failing to verify transaction details before filing returns

Latest GST Rules Related to Intra-state Supply

Recent GST clarifications have continued to emphasise the importance of correctly determining the place of supply before classifying a transaction as intra-state or inter-state. Businesses should note that GST rules and tax applicability may evolve through notifications, circulars, and clarifications issued by GST authorities from time to time.

Conclusion

Correct classification of supplies under inter-state and intra-state GST helps businesses apply the appropriate taxes, maintain accurate invoices, and improve overall GST compliance. Proper understanding of supply rules may also reduce reporting mismatches, tax calculation errors, and avoidable compliance-related complications.

For businesses managing GST compliance alongside operational growth, SMFG India Credit offers unsecured financing of up to Rs. 75 lakhs* at attractive business loan interest rates.

Check your borrowing capacity using our business loan eligibility calculator and apply online today.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us