GSTR-7 under GST is a monthly return filed by taxpayers who are required to deduct Tax Deducted at Source (TDS). The GSTR-7 meaning mainly relates to reporting TDS deductions, tax payments, and details of deductees through the GST portal. Following the correct GSTR-7 return filing process is important because delayed or incorrect filing may affect GST compliance and prevent deductees from claiming eligible tax credits on time. Timely filing also helps maintain accurate GST records and reduces the risk of penalties or notices from tax authorities.

What Is GSTR-7?

GSTR-7 is a GST return filed by registered taxpayers who deduct TDS under GST provisions on specified transactions. The GSTR-7 meaning primarily pertains to reporting TDS deductions, deductee details, and tax payments to the government through the GST portal. Proper GST TDS return filing helps deductees view the deducted tax amount in their GSTR-2A and claim eligible credit accordingly.

For example, if a government department deducts TDS while making payment to a contractor, the deducted amount is reported through GSTR-7 so the contractor can claim the corresponding GST credit.

Who Needs to File GSTR-7?

GSTR-7 must be filed by entities that are required to deduct TDS under GST provisions as per Section 51 of the CGST Act. Understanding GSTR-7 eligibility is important because only specified organisations falling under GST TDS deduction rules are required to file this return and deposit deducted tax within prescribed timelines. These entities should also monitor the applicable GSTR-7 due date to avoid penalties and compliance issues.

The following are the entities who should file GSTR-7 under current GST provisions:

- Government departments

- Local authorities

- Government agencies

- Public Sector Undertakings (PSUs)

- Notified authorities or boards

- Other notified entities required to deduct GST TDS

Conditions for TDS Deduction Under GST

TDS under GST is generally required when the contract value for taxable goods or services exceeds Rs. 2.5 lakh. Deductors must apply the correct TDS rate depending on whether the supply is intra-state or inter-state. Proper deduction, monthly GST return filing, and timely payment before the GSTR-7 due date are important for maintaining compliance.

|

Supply Type

|

Applicable TDS Rate

|

|

Intra-state Supply

|

2% (1% CGST + 1% SGST)

|

|

Inter-state Supply

|

2% IGST

|

GSTR-7 Due Date for Filing

GSTR-7 must generally be filed every month by the 10th day of the following month through the GST portal. The GSTR-7 due date 2026 continues to follow the same monthly filing structure for FY 2026–27. Delayed filing may result in interest liability and a GSTR-7 late filing penalty, which can also affect deductees claiming GST TDS credits on time. Businesses and notified entities should regularly track the GST TDS return due date to maintain compliance.

|

Tax Period

|

GSTR-7 Filing Due Date

|

|

April 2026

|

10 May 2026

|

|

May 2026

|

10 June 2026

|

|

June 2026

|

10 July 2026

|

Regular GSTR-7 filing and timely TDS deposits may sometimes affect short-term working capital planning, especially for businesses managing multiple vendor payments and compliance obligations. In such situations, a business loan may help maintain smoother operational cash flow and financial flexibility.

Enterprises planning expenses and repayments carefully may also benefit from using a business loan EMI calculator to estimate monthly repayment obligations and support more structured financial planning alongside GST compliance requirements.

GSTR-7 Format and Details Required

The GSTR-7 format includes details related to GST TDS deductions, tax payments, amendments, and related compliance information reported by deductors each month. Understanding the GSTR-7 filing format can help businesses and notified entities avoid reporting errors and maintain accurate records. The return is filed electronically through the GST portal and contains multiple sections covering tax deduction and payment details.

Main sections included in the GSTR-7 are:

- GSTIN and basic TDS deductor details

- Details of TDS deducted

- Amendments to previously filed information

- Interest and late fee details

- Refund claimed

- Tax payment and electronic cash ledger information

Details to Be Furnished in GSTR-7

The GSTR-7 online filing process requires deductors to furnish invoice-wise TDS details, tax payments, amendments, and related compliance information through the GST portal. Proper reporting of each section can help avoid mismatches, delays in TDS credit reflection, and GST compliance issues for deductees.

|

Section Name

|

Purpose

|

Mandatory / Optional

|

|

GSTIN & Deductor Details

|

Identifies the deductor filing GSTR-7

|

Mandatory

|

|

TDS Deduction Details

|

Reports invoice-wise TDS deducted from suppliers

|

Mandatory

|

|

Amendments

|

Corrects details from previous returns

|

Optional

|

|

Interest & Late Fee

|

Reports delayed payment liabilities

|

Mandatory if applicable

|

|

Refund Claimed

|

Reports refund request from cash ledger

|

Optional

|

|

Electronic Cash Ledger

|

Shows tax payment details

|

Mandatory

|

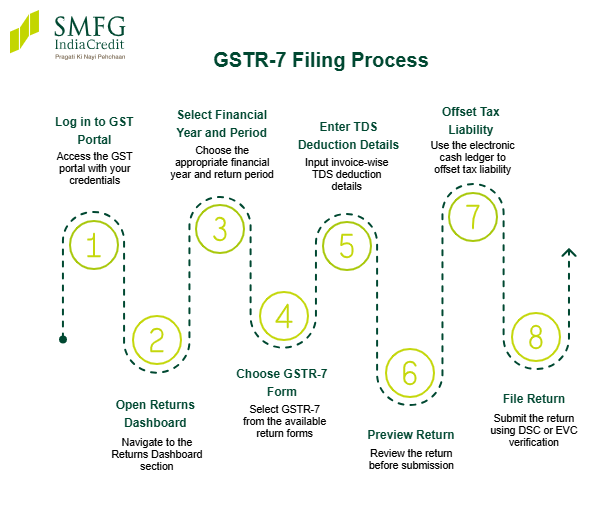

Step-by-Step Process to File GSTR-7 Online

Understanding how to file GSTR-7 correctly can help reduce filing errors and maintain proper GST compliance.

- Log in to the official GST Portal.

- Open the “Returns Dashboard” section.

- Select the relevant financial year and return period.

- Choose GSTR-7 from the available return forms.

- Enter invoice-wise TDS deduction details.

- Preview the return before submission.

- Offset tax liability using the electronic cash ledger.

- File the return using DSC or EVC verification.

Late Fees and Penalty for GSTR-7

Delayed filing beyond the GSTR-7 due date may attract late fees, interest liability, and additional compliance issues under GST provisions.

Understanding GSTR-7 late fees and the penalty for late GSTR-7 filing can help entities maintain timely compliance.

|

Non-Compliance Type

|

Applicable Charges

|

|

Late Fee under CGST

|

Rs. 100 per day

|

|

Late Fee under SGST

|

Rs. 100 per day

|

|

Total Late Fee

|

Rs. 200 per day

|

|

Maximum Late Fee

|

Rs. 5,000

|

|

Interest on Delayed TDS Payment

|

18% per annum

|

|

IGST Late Fee

|

Generally not applicable

|

Interest on Delayed Payment Under GSTR-7

If TDS payment under GSTR-7 is delayed, interest is generally charged at 18% per annum on the unpaid tax amount for the delay period. The interest is usually calculated from the due date until the actual payment date.

Basic Formula:

Interest = TDS Amount × 18% × Number of Delay Days ÷ 365

For example, if a delayed TDS payment of Rs. 50,000 is made 20 days late, the applicable interest would be approximately Rs. 493.

Nil GSTR-7 Return Filing

A nil GSTR-7 return may be filed when no TDS deduction has been made during the tax period, and there are no pending or rejected records requiring correction. Under current nil GSTR-7 filing rules, deductors must still file the return within the applicable GSTR-7 due date even if no transactions are reported. Recent GST portal updates have also provided relief in certain cases by reducing or waiving late fees for eligible nil return filings, subject to CBIC notifications and applicable conditions.

Can GSTR-7 Be Revised?

GSTR-7 cannot generally be revised after submission on the GST portal. Businesses searching for how to revise GSTR-7 return should note that any correction or amendment must usually be reported in subsequent returns. For example, if incorrect TDS details are filed for one month, the deductor may correct them in the next eligible GSTR-7 filing period.

GSTR-7A TDS Certificate

Form GSTR-7A is a TDS certificate generated automatically on the GST portal after successful filing of GSTR-7 by the deductor. The GST TDS certificate GSTR-7A contains details such as TDS deducted, deductor information, deductee details, and tax amounts deposited with the government.

This TDS certificate under GST helps deductees verify deducted tax amounts and claim eligible TDS credit in their electronic cash ledger or GST records. Timely filing of GSTR-7 is important because delays may also delay certificate generation for deductees.

Benefits of Timely GSTR-7 Filing

Timely filing of GSTR-7 helps maintain proper compliance and ensures that deductees receive tax credit details without unnecessary delays. Filing before the GSTR-7 due date may also help businesses avoid penalties, interest liability, and reconciliation issues during GST audits or return verification.

Key benefits of timely GSTR-7 filing include:

- Smooth flow of Input Tax Credit (ITC) for deductees

- Reduced risk of late fees and interest charges

- Accurate reporting of GST TDS deductions

- Better GST compliance and record maintenance

- Faster availability of TDS certificates for deductees

Common Mistakes to Avoid While Filing GSTR-7

Incorrect or incomplete information while filing GSTR-7 may lead to compliance issues, delayed TDS credit reflection, and possible penalties under GST provisions. Careful verification of return details before submission can help businesses and deductors maintain accurate GST records and avoid unnecessary amendments later.

Common mistakes to avoid include:

- Entering incorrect GSTIN details

- Reporting wrong TDS amounts

- Delayed filing of returns

- Invoice mismatches or incorrect deductee details

- Errors in amendment reporting

- Incorrect tax payment or ledger adjustment details

Conclusion

GSTR-7 plays an important role in GST TDS compliance by helping deductors report tax deductions, payments, and related details accurately. Timely filing before the GSTR-7 due date can help avoid penalties, support smooth tax credit flow for deductees, and maintain accurate GST records.

For businesses managing GST compliance alongside operational and expansion requirements, SMFG India Credit offers unsecured financing of up to Rs. 75 lakhs* at competitive business loan interest rates.

Prepare the business loan documents required and apply with a convenient online process.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us