“What is GST?” is a fundamental question for businesses, professionals, and consumers operating under India’s Goods and Services Tax regime. The CGST meaning refers to the Central Goods and Services Tax, which represents the central government’s share of GST on intra-state transactions. In simple terms, whenever goods or services are supplied within the same state, a portion of the tax collected goes to the Centre in the form of CGST.

To clearly grasp the CGST definition, it is important to see it as one of the key pillars of the GST framework. Central GST in India works alongside the State Goods and Services Tax (SGST) to ensure balanced revenue distribution between the central and state governments. A proper understanding of CGST helps businesses maintain compliance, calculate taxes correctly, and avoid penalties under the GST law.

Meaning of CGST

The CGST full form is Central Goods and Services Tax. The CGST definition refers to the tax imposed by the Central Government on intra-state supplies of goods and services within the broader GST framework. Whenever a sale or service takes place within the boundaries of a single state, the total GST charged is split into two equal components: CGST and State Goods and Services Tax.

To further clarify what CGST is, it represents the portion of GST revenue allocated to the central authority from such intra-state transactions. Rather than functioning as a separate or additional levy, CGST operates as an integrated element of the GST structure. Among the various GST components, CGST plays a crucial role in ensuring revenue sharing between the Centre and states while preserving a standardised indirect taxation system throughout India.

Understanding the CGST Act

The CGST Act governs the levy, collection, administration, and compliance of the Central Goods and Services Tax in India. Enacted in 2017, the CGST Act aligns with the overall GST law to create a harmonised tax structure.

The Act defines taxable events, input tax credit provisions, registration rules, valuation methods, and compliance requirements. It also outlines penalties for violations and procedural guidelines. By operating alongside the State Goods and Services Tax law and Integrated GST provisions, the CGST Act ensures a coordinated and uniform GST system across the country.

Applicability of CGST

CGST applicability arises in the following situations:

- Intra-state supplies of goods

CGST is charged when goods are supplied within the geographical boundaries of the same state. In such cases, the transaction does not cross state lines, and the total GST is divided equally between the Central Goods and Services Tax and the State Goods and Services Tax. This applies to manufacturers, wholesalers, retailers, and any registered supplier making local sales.

- Intra-state supplies of services

CGST also applies when services are provided within a single state. If both the location of the supplier and the place of supply are in the same state, intra-state supplies CGST becomes applicable along with the corresponding state component. Professional services, consultancy, repairs, and digital services rendered locally fall under this category.

- Sales where the supplier and buyer are located in the same state

When both the seller and the recipient are registered or operating in the same state, the transaction qualifies as an intra-state supply. In such cases, Central Goods and Services Tax is levied as part of the total GST charged on the invoice. The tax collected is then apportioned between the central and state governments in equal proportion.

- Transactions falling under taxable supplies as defined in the CGST Act

CGST applies only to supplies that are classified as taxable under the CGST Act. If goods or services are neither exempt nor zero-rated, they are generally subject to GST, including the CGST portion. The Act clearly defines taxable events, ensuring that only eligible transactions attract CGST liability.

CGST on Goods and Services: Example

If a product worth ₹50,000 is sold within Karnataka at 18% GST:

- CGST applicable (9%) = ₹4,500

- SGST applicable (9%) = ₹4,500

Here, CGST on goods and services represents the central government’s share. Thus, understanding CGST applicability helps businesses determine proper tax charging and compliance.

Key Features of the CGST Act

- Uniform Tax Structure Across India

The CGST Act establishes a standardised indirect tax framework that applies uniformly throughout the country. This consistency reduces disparities between states and simplifies taxation for businesses operating in multiple locations. A uniform structure also promotes ease of doing business and enhances transparency in pricing.

- Seamless Input Tax Credit Mechanism

Businesses can claim credit for the CGST paid on purchases and offset it against their output CGST liability. This mechanism minimises the cascading effect of taxes and ensures that tax is levied only on the value addition at each stage.

- Defined Threshold Limits for Registration

The Act clearly specifies turnover thresholds beyond which registration becomes mandatory. This ensures that small businesses below a certain limit are not burdened with unnecessary compliance requirements. At the same time, it brings medium and large enterprises into the formal tax system, improving revenue collection and accountability.

- Structured Compliance and Reporting System

The CGST Act lays down detailed provisions for return filing, record maintenance, and tax payment schedules. Businesses are required to submit periodic returns through the GST portal and disclose transaction details through the prescribed formats. This structured compliance framework promotes systematic reporting and reduces the scope for tax evasion.

- Clear Provisions for the Reverse Charge Mechanism

The Act includes specific CGST rules regarding the reverse charge mechanism (RCM), where the recipient of goods or services is liable to pay tax instead of the supplier. This provision applies in notified categories and certain unregistered transactions. It ensures tax collection even when the supplier may not be registered or compliant.

- Defined Penalties for Non-Compliance

The Act outlines penalties for delayed CGST return filing, non-payment of tax, incorrect reporting, and fraudulent activities. Interest, fines, and even cancellation of registration may be imposed in serious cases. These deterrent measures encourage timely compliance and responsible tax practices.

- Transparent Invoicing Standards

Proper invoicing is a critical requirement under the Central Goods and Services Tax The Act mandates specific details such as GSTIN, invoice number, taxable value, and tax breakup to be clearly mentioned on invoices. Transparent invoicing ensures accurate tax calculation, smooth ITC claims, and better audit tracking.

These features make the CGST Act an integral part of the GST framework and promote GST compliance nationwide.

Difference Between CGST and Other GST Components

Under GST, tax is divided based on the nature of supply. Understanding CGST vs SGST or CGST vs IGST is essential.

- CGST – Collected by the Central Government on intra-state supplies.

- SGST – Collected by the State Government on intra-state supplies.

- IGST – Collected on inter-state supplies.

- UTGST – Applicable in Union Territories instead of SGST.

GST Components Comparison

|

Component

|

Applicable On

|

Collected By

|

Example

|

|

CGST

|

Intra-state

|

Central Govt

|

Sale within Delhi

|

|

SGST

|

Intra-state

|

State Govt

|

Sale within Delhi

|

|

IGST

|

Inter-state

|

Central Govt

|

Delhi to Maharashtra

|

|

UTGST

|

Union Territories

|

UT Govt

|

Sale within Chandigarh

|

Key CGST Rules

The CGST rules govern several essential compliance aspects:

- Proper Tax Invoice Issuance

Under the Central Goods and Services Tax rules, every registered taxpayer must issue a valid tax invoice for taxable supplies of goods or services. The invoice must contain mandatory details such as GSTIN, invoice number, date of issue, description of goods or services, taxable value, applicable GST rate, and the amount of tax charged. Accurate invoicing is critical because it forms the basis for tax calculation and enables the recipient to claim Input Tax Credit.

- Determination of the Time of Supply

The time of supply determines when the liability to pay the Central Goods and Services Tax The rules specify different criteria for goods and services, generally linked to the date of invoice issuance or receipt of payment, whichever is earlier. Correct determination of the time of supply ensures that CGST is reported and paid in the appropriate tax period, preventing interest and penalties.

- Valuation Based on Taxable Value

CGST is calculated on the taxable value of goods or services supplied. The rules define how this value should be determined, including the inclusion of incidental expenses such as packing, commission, and certain taxes (excluding GST itself). Proper valuation ensures that the correct amount of Central Goods and Services Tax is charged and prevents disputes related to underreporting or overvaluation.

- Reverse Charge Mechanism (RCM) Provisions

The CGST rules include provisions for the Reverse Charge Mechanism (RCM), where the responsibility to pay tax shifts from the supplier to the recipient. This typically applies in specific notified categories or when dealing with unregistered suppliers. RCM ensures that tax is collected even when the supplier may not be liable or registered under GST.

- Record Maintenance Requirements

Registered persons are required to maintain detailed records of purchases, sales, stock, input tax credit, and tax payments. These records must be preserved for a prescribed period and made available during audits or inspections. Proper record maintenance supports transparency, facilitates return filing, and ensures smooth compliance under the CGST Act.

CGST Rate Slabs in India

The CGST rate slabs mirror half of the overall GST rate. It determines the CGST percentage applicable to a taxable supply.

CGST Slab Rates

- 0% CGST rate – Essential goods

- 2.5% (5% GST rate) – Basic items

- 9% (18% GST rate) – Standard goods and services

- 20% (40% GST rate) – Luxury goods

Special categories include:

- 1.5% CGST (3% GST rate) for jewellery and precious metals/gemstones like gold and pearls

- 0.125% CGST (0.25% GST rate) for diamonds and precious stones

Each CGST slab aligns with the GST tax slab in India guidelines and applies based on product classification.

How CGST Is Calculated, with Example

Understanding how the Central Goods and Services Tax is calculated requires applying the formula of CGST to the taxable value.

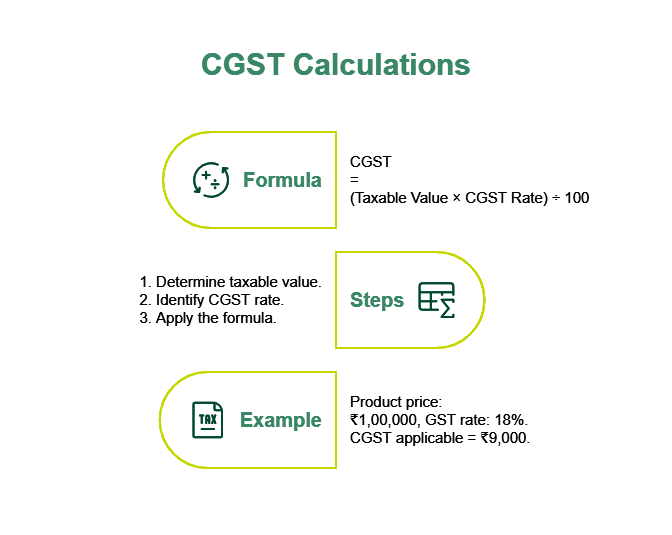

Formula of CGST

CGST = (Taxable Value × CGST Rate) ÷ 100

Steps for CGST Calculation

- Determine the taxable value of goods/services.

- Identify the applicable CGST rate slab.

- Apply the formula of CGST.

CGST Calculation Example

Product price: ₹1,00,000

GST rate: 18%

CGST applicable = ₹1,00,000 × 9% = ₹9,000

This example demonstrates the GST formula in India for intra-state supplies.

CGST Registration Requirements

Businesses must obtain CGST registration under the GST registration in India if:

- Annual turnover exceeds prescribed threshold limits

- Engaged in interstate supplies

- Operating as e-commerce operators

- Liable under reverse charge

The CGST registration process is conducted online through the GST Portal and involves verification and approval by authorities.

Documents Required for CGST

To complete CGST registration, the following documents are typically required:

- pan card

- Aadhaar card

- Address proof of business

- Bank account details

- Business registration certificate

These documents support GST registration in India compliance requirements.

Input Tax Credit (ITC) Under CGST

CGST ITC allows businesses to claim credit for tax paid on purchases. Through the Input Tax Credit under GST, CGST paid on inputs can be offset against the Central Goods and Services Tax liability.

This reduces cascading tax effects and improves liquidity. However, ITC must comply with eligibility rules under the CGST Act and proper documentation requirements.

Compliance and Return Filing for CGST

CGST return filing is a critical part of GST compliance. Businesses must file:

- GSTR-1 – Details of outward supplies

- GSTR-3B – Summary return with tax payment

Return filing must follow the compliance schedule, generally monthly or quarterly, depending on turnover. Filing is done via the GST Portal. Proper reporting avoids penalties and ensures smooth compliance.

Benefits of CGST for Businesses and Consumers

Key CGST benefits include:

- Eliminates cascading tax effect

- Promotes transparency in taxation

- Simplifies indirect tax structure

- Enables seamless ITC claims

- Improves compliance efficiency

- Uniform tax rates nationwide

- Reduced tax evasion

- Better revenue tracking

These CGST advantages benefit both enterprises and end consumers.

Penalties for Non-Compliance

Depending on the severity of non-compliance, CGST penalties can include:

- Late filing fees

- Interest on delayed payment

- Monetary fines

- Cancellation of registration

Strict adherence to rules helps avoid such GST non-compliance penalties.

Conclusion

Understanding CGST tax importance is vital for every business operating in India. From knowing what CGST is and its slab structure to mastering compliance and calculation methods, a strong grasp of the Central Goods and Services Tax ensures lawful and efficient tax management. With this knowledge, taxpayers can maintain compliance, reduce errors, and optimise tax planning within the GST framework.

Alongside meeting GST responsibilities, businesses often need to maintain steady working capital, manage operating expenses, and fund expansion. To help meet these financial requirements, SMFG India Credit provides business loans of up to Rs. 75 lakhs*. Enterprises that meet business loan eligibility can access competitive interest rates and flexible repayment tenures of up to 60 months*. You can use the business loan EMI calculator and eligibility calculator to plan your borrowing and apply online with minimal business loan documentation.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us