The GST composition scheme is a simplified taxation system designed for small businesses and taxpayers with limited turnover under GST. Instead of following regular GST filing and tax calculation procedures, eligible businesses can pay tax at fixed rates with reduced compliance requirements.

In 2026, the scheme continues to support small traders, manufacturers, restaurants, and local businesses by simplifying return filing and recordkeeping. The GST composition scheme turnover limit and eligibility conditions remain important factors for businesses evaluating this option, especially those seeking easier GST compliance for SMEs and reduced administrative burden.

What Is the Composition Scheme in GST?

The GST composition scheme is a simplified tax option introduced under Section 10 of the CGST Act for eligible small taxpayers.

Under the GST composition scheme rules, businesses pay GST at fixed lower rates based on their aggregate turnover instead of charging regular GST rates on every transaction. The scheme is mainly designed to reduce compliance requirements, maintain simpler records, and lower return filing frequency for eligible taxpayers. The GST composition scheme for small businesses is commonly used by local traders, manufacturers, and restaurants with limited turnover.

For example, a small restaurant registered under the composition scheme may pay GST at a fixed percentage of turnover instead of following standard GST tax rates and filing procedures.

Key Features of GST Composition Scheme

The GST Composition Scheme offers simplified tax compliance for eligible small businesses by reducing filing requirements and recordkeeping responsibilities. Under the GST Composition Scheme rules, taxpayers pay GST at fixed lower rates on turnover instead of regular GST rates. The scheme is designed to simplify GST filing for composition dealers and reduce administrative burden for smaller businesses.

Key features of the GST Composition Scheme include:

- Lower GST rates on eligible turnover.

- Simplified quarterly tax payments.

- Reduced GST return filing requirements.

- Easier bookkeeping and compliance processes.

- No requirement for detailed tax invoices in many cases.

- Composition dealers cannot collect GST separately from customers.

- Limited compliance burden compared to regular GST registration.

Eligibility Criteria for GST Composition Scheme

Businesses eligible for the GST Composition Scheme generally include small manufacturers, traders, restaurants, and specified service providers meeting prescribed turnover conditions. The composition levy under GST is available only if the business turnover remains within the notified threshold limits across all businesses linked to the same PAN. The GST composition scheme limit differs for normal and certain special category states.

|

Eligible Category

|

Basic Eligibility

|

|

Manufacturers

|

Eligible subject to notified goods restrictions and turnover limits

|

|

Traders

|

Eligible if aggregate turnover remains within prescribed limits

|

|

Restaurants

|

Eligible for restaurants not serving alcohol

|

|

Service Providers

|

Eligible subject to specified turnover conditions under GST

|

|

Special Category States

|

Lower turnover thresholds may apply in certain states

|

Turnover Limit Under GST Composition Scheme 2026

The GST Composition Scheme is available only to businesses whose aggregate turnover remains within prescribed limits under GST Council law. Aggregate turnover includes taxable supplies, exempt supplies, exports, and inter-state supplies across all businesses linked to the same PAN. The GST turnover limit 2026 remains an important factor for businesses evaluating eligibility under the scheme. Businesses should also regularly review the GST composition scheme turnover limit because thresholds may change through future GST updates and notifications.

|

Business Category

|

Turnover Limit

|

|

Goods (Traders and Manufacturers)

|

Up to Rs. 1.5 crore in the preceding financial year

|

|

Special Category States

|

Up to Rs. 75 lakhs in specified states (such as Manipur, Meghalaya)

|

|

Service Providers

|

Up to Rs. 50 lakhs in the preceding financial year

|

|

Mixed Businesses (Goods + Services)

|

Goods turnover within Rs. 1.5 crore, and services within Rs. 5 lakhs or 10% of turnover

|

GST Composition Scheme Tax Rates 2026

The GST Composition Scheme allows eligible small businesses to pay GST at concessional fixed rates based on turnover instead of standard GST rates. The composition scheme GST rate varies depending on the type of business activity. These simplified GST tax rates for small businesses are designed to reduce compliance burden and simplify tax calculations for eligible taxpayers.

|

Type of Business

|

CGST

|

SGST

|

Total GST Rate

|

|

Manufacturers and Traders (Goods)

|

0.5%

|

0.5%

|

1.0%

|

|

Restaurants that do not serve alcohol

|

2.5%

|

2.5%

|

5.0%

|

|

Other Eligible Service Providers

|

3.0%

|

3.0%

|

6.0%

|

Benefits of GST Composition Scheme for Small Businesses

The GST Composition Scheme offers several practical advantages for small businesses looking for easier tax compliance and lower administrative costs. As a GST simplified taxation scheme, it helps eligible taxpayers reduce paperwork, maintain simpler records, and avoid frequent compliance requirements. Small retailers, local restaurants, and neighbourhood traders often prefer the scheme because it supports easier day-to-day tax management and predictable tax payments.

Key benefits of the GST Composition Scheme include:

- Lower GST rates compared to regular GST registration

- Simplified accounting and recordkeeping requirements

- Reduced return filing frequency

- Easier GST filing for composition dealers

- Lower compliance burden for small businesses

- Better cash flow planning due to simpler tax calculations

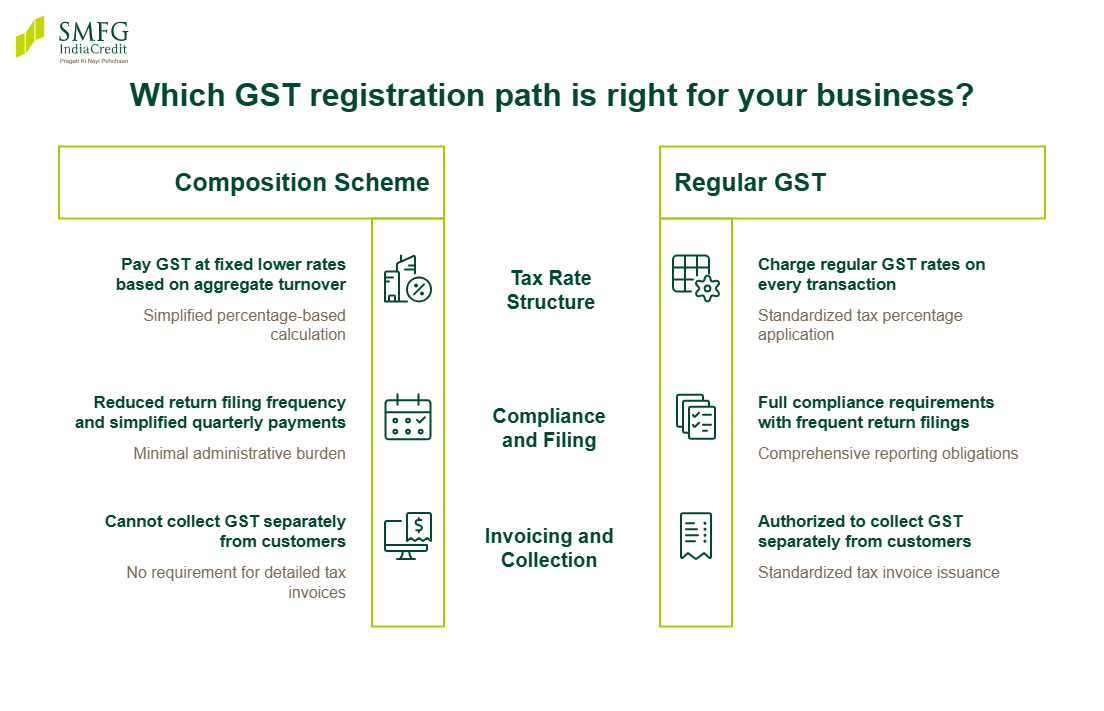

GST Composition Scheme vs Regular GST Scheme

|

Basis

|

Composition Scheme

|

Regular GST Scheme

|

|

GST Rates

|

Fixed lower rates on turnover

|

Standard GST rates as applicable

|

|

Input Tax Credit (ITC) Availability

|

ITC cannot generally be claimed

|

Eligible ITC can be claimed subject to conditions

|

|

Return Filing

|

Simplified and fewer returns

|

Regular monthly or quarterly filings

|

|

Interstate Supply

|

Generally restricted

|

Allowed across India

|

|

Invoice Type

|

Bill of supply issued

|

Tax invoice issued with GST

|

|

GST Collection

|

GST cannot be collected separately from customers

|

GST collected from customers

|

|

Compliance Burden

|

Lower compliance requirements

|

Higher compliance and reporting requirements

|

The composition scheme is generally more suitable for small local businesses with limited turnover, while the regular GST scheme may benefit businesses seeking interstate expansion, larger ITCs, and broader operational flexibility.

Return Filing Under GST Composition Scheme

Businesses registered under the composition scheme are required to follow simplified return filing procedures through the GST portal. Instead of multiple monthly returns, composition taxpayers generally file quarterly tax payment statements and an annual return.

Understanding the applicable GST Composition Scheme forms, filing frequency, and due dates can help businesses avoid penalties and maintain proper compliance.

|

GST Composition Scheme Form

|

Purpose

|

Filing Frequency

|

Due Date

|

|

CMP-08

|

Statement for tax payment under composition scheme

|

Quarterly

|

18th of the month following the quarter

|

|

GSTR-4

|

Annual return for composition taxpayers

|

Annual

|

Generally due by 30th April following the financial year

|

How to Register for GST Composition Scheme

Eligible businesses can apply for the composition scheme online through the GST Portal by following the prescribed GST composition registration process. Existing taxpayers generally need to opt into the scheme before the beginning of a financial year, while new applicants may select the option during GST registration itself. Businesses should also ensure that they satisfy turnover and eligibility conditions before applying.

- Visit the official GST portal and log in.

- Navigate to the composition scheme application section.

- Submit Form CMP-02 to opt for the composition scheme.

- Verify business details and eligibility conditions.

- Submit the application using digital verification methods.

- Existing taxpayers should generally apply before the start (31st March) of the next financial year.

Invoice Rules for Composition Dealers

Composition dealers are required to issue a Bill of Supply instead of a regular tax invoice because they cannot collect GST separately from customers. Under composition dealer rules, invoices must clearly mention that the supplier is registered under the composition scheme. Proper invoicing helps businesses maintain GST compliance and avoid reporting issues during return filing or audits.

Basic invoice compliance checklist for composition dealers:

- Issue a Bill of Supply instead of a tax invoice

- Mention “composition taxable person” prominently on invoices

- Include supplier name, address, and GSTIN

- Mention invoice number and date

- Maintain proper records of all outward supplies

Input Tax Credit (ITC) Under GST Composition Scheme

Businesses registered under the GST Composition Scheme are generally not allowed to claim Input Tax Credit (ITC) on purchases and expenses. Since composition dealers also cannot collect GST separately from customers, the tax paid on inputs becomes part of their business cost. This may affect pricing decisions, especially in B2B transactions where buyers often prefer suppliers who allow ITC claims.

For example, a regular GST dealer purchasing goods worth Rs. 1 lakh may claim eligible ITC on GST paid. However, a composition dealer purchasing the same goods cannot claim ITC, which may increase the effective business cost compared to a regular GST-registered business.

For small businesses operating under the composition scheme, blocked ITC and upfront tax costs may sometimes affect working capital and cash flow management. In such situations, a business loan may help enterprises manage inventory purchases, supplier payments, and operational expenses more smoothly.

Businesses planning borrowing may also benefit from estimating repayment obligations in advance. Using a business loan EMI calculator can help assess monthly instalments and support better financial planning alongside GST-related expenses.

Penalties and Non-Compliance Under GST Composition Scheme

Non-compliance under the GST composition scheme may result in penalties, cancellation of registration, or disqualification from the scheme if a business is found ineligible. Delayed filing of GSTR-4 may attract late fees of Rs. 50 per day, subject to a prescribed limit of a maximum of Rs. 2,000 under GST provisions.

Conclusion

The GST Composition Scheme offers a simplified tax structure for eligible small businesses by reducing compliance requirements, lowering filing frequency, and simplifying recordkeeping. Understanding eligibility conditions, tax rates, return filing rules, and the GST composition scheme limit can help businesses choose the most suitable Goods and Services Tax structure for their operational and compliance needs.

To support enterprises managing GST obligations alongside expansion efforts, SMFG India Credit offers unsecured financing of up to Rs. 75 lakhs* at competitive business loan interest rates.

Check your borrowing capacity using our business loan eligibility calculator and apply online today.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us