Tax in India is a compulsory payment made to the government on income, goods, or services, as prescribed under law. The meaning of tax is a legally enforced financial charge collected by the government to fund public services and national development. Taxation is the structured system through which the state assesses, collects, and manages tax revenue. The Income Tax Department under the Government of India administers direct tax laws, while the gst council oversees indirect tax through GST.

In 2026, digital tax filing and compliance systems have made tax processes faster, more transparent, and largely paperless. Let’s understand more about what taxation in India is and how it plays an important role in several aspects, including applying for loans and visas.

Meaning of Tax in India

The tax meaning refers to a compulsory payment you make to the government without receiving a direct service in return.

The tax definition explains it as a legally enforced contribution collected to fund public services and administration. Tax in India refers to charges on income, property, goods, and services. It is broadly divided into Direct Tax and Indirect Tax. These collections form a major part of Government Revenue and support national development. You are required to pay tax under the law, making it a mandatory financial obligation.

What Is Taxation?

Taxation is the formal process through which the government levies, collects, and assesses taxes. The taxation system in India operates under laws such as the Income Tax Act and the GST Act. The Central Board of Direct Taxes oversees direct tax administration. In simple terms, taxation begins with the levy, followed by collection, and then assessment to verify correct tax payment. This structured system ensures accountability and proper tax compliance.

Objectives of Taxation in India

The objectives of taxation go beyond simply revenue collection.

The purpose of taxes includes maintaining economic balance and funding national priorities.

Tax in India supports:

- Implementation of fiscal policies

- Promotion of economic development

- Financing public welfare schemes

- Redistribution of income

- Infrastructure funding and economic stability

Through proper tax planning and tax reforms, the government uses tax revenue to support growth and long-term development.

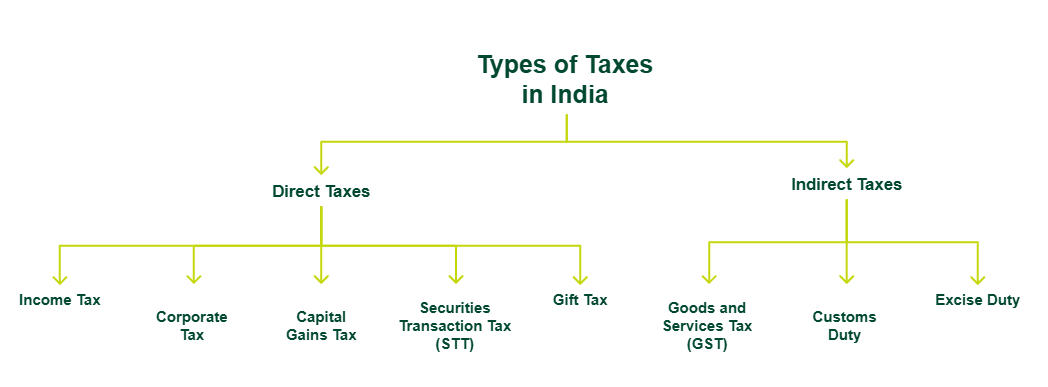

Different Types of Taxes in India

When you look at the different types of taxes in India, they are broadly classified into direct and indirect taxes under the Indian Tax System. This classification helps you understand how tax in India is collected and who ultimately bears the tax burden.

Direct Tax is imposed directly on your income or profits, meaning you pay the tax yourself to the government. Indirect Tax, on the other hand, is collected on goods and services, where the tax is included in the price you pay as a consumer.

The tax system in India relies on this structure to balance revenue collection and economic fairness. Direct and indirect taxes together ensure that the levy is collected from both income generation and consumption. The types of taxes in India demonstrate how fiscal obligations differ for individuals, businesses, and consumers, while ensuring compliance across sectors.

Direct Taxes in India

A direct tax is a tax you pay directly to the government on your income or profits. The meaning of direct tax is simple: the person on whom the tax is imposed must bear the burden and cannot transfer it to someone else. Common examples of direct tax include Income Tax, Corporate Tax, and Capital Gains Tax.

If you are salaried or self-employed, you calculate tax on your taxable income and complete an income tax filing by submitting your Income Tax Return (ITR). Direct tax in India is governed by the Income Tax Act and forms a major part of government revenue.

Examples of Direct Taxes

Common direct tax examples under the Income Tax Act include:

- Income Tax

- Corporate Tax

- Capital Gains Tax

- Securities Transaction Tax (STT)

STT applies to securities transactions in the stock market. Capital gains are further classified as LTCG (Long-Term Capital Gains) and STCG (Short-Term Capital Gains), which determine how much tax you pay on asset sales. These direct tax examples affect your overall taxable income and tax liability.

Indirect Taxes in India

An indirect tax in India is a tax collected on goods and services rather than directly on income. The burden of indirect tax can be shifted to the end consumer, as it is included in the price of products. The most important indirect tax today is the Goods and Services Tax (GST tax).

Before GST, indirect tax in India included Excise Duty and Value Added Tax (VAT). These were later merged into GST to simplify the tax structure. When you purchase goods or services, you pay GST as part of the final price. Businesses collect this tax and deposit it with the government. Indirect tax plays a key role in broadening the tax base and strengthening the overall tax system.

GST as the Main Indirect Tax in India

GST in India is the central indirect tax that replaced multiple older indirect tax laws, such as VAT and Excise Duty. It follows a dual structure consisting of CGST, SGST, and IGST, depending on whether the supply is within a state or between states. Different GST types apply based on the nature of the transaction. The GST Council decides GST rates and policy changes. The Goods and Services Tax simplified the indirect tax structure, reduced the cascading effect, and improved compliance by creating a unified national market.

Must Read: Direct vs Indirect Taxes: A Guide for Business Owners

Tax Slabs in India

Income tax in India follows a slab-based system, meaning your tax liability depends on your income level. An income tax slab defines the rate at which tax applies to different income ranges. Under the Income Tax Act, you can choose between the Old Tax Regime and the New Tax Regime.

Tax slabs in 2026 are progressive, so higher income attracts higher tax rates. The Old Tax Regime allows you to claim more deductions and exemptions, while the New Tax Regime offers lower tax rates with fewer deductions. Your choice affects overall tax calculation and long-term financial planning. Tax slabs in India are revised periodically under tax reforms, so you should always check the latest rules before filing your income tax.

New Regime Slab Rates (FY 2026-2027)

|

Income Tax Slab (Rs.)

|

New Regime Rate

|

|

Up to 4 lakh

|

Nil

|

|

4 lakh – 8 lakh

|

5%

|

|

8 lakh – 12 lakh

|

10%

|

|

12 lakh – 16 lakh

|

15%

|

|

16 lakh – 20 lakh

|

20%

|

|

20 lakh – 24 lakh

|

25%

|

|

Above 24 lakh

|

30%

|

Old Regime Slab Rates (FY 2026-2027)

|

Income Tax Slab (Rs.)

|

Old Regime Rate

|

|

Up to 2.5 lakh

|

Nil

|

|

2.5 lakh – 5 lakh

|

5%

|

|

5 lakh – 10 lakh

|

20%

|

|

Above 10 lakh

|

30%

|

*Slab rates differ for resident senior and super senior citizens.

Income Tax Slab Comparison (Old vs New Regime)

|

Regime

|

Income Tax Exemptions

|

Best For

|

|

New Regime (Section 115BAC)

|

Limited exemptions, lower tax rates

|

Individuals with fewer deductions

|

|

Old Regime

|

Deductions such as Section 80C, HRA, and Standard Deduction are available

|

Salaried taxpayers maximising benefits; individuals with high deductions

|

Your old vs new tax regime choice directly impacts tax savings and income tax calculation.

How Taxes are Calculated in India

If you want to understand how income tax is calculated, start with your gross total income. This includes salary, business income, capital gains, and other sources. From this, you subtract eligible deductions to arrive at taxable income.

The applicable income tax slab rates are then applied. After calculating basic tax, you add health & education cess and, where applicable, surcharge.

This full process forms your income tax calculation in India. For example, if your gross total income is ₹10,00,000 and deductions reduce ₹1,50,000, tax applies only on the remaining income. Accurate calculation ensures correct tax filing and avoids tax penalties.

Tax Deductions and Exemptions in India

Tax deductions and income tax exemptions help you legally reduce your overall tax liability. When you calculate tax, you first determine your income and then subtract eligible tax deductions to arrive at taxable income. These deductions are allowed under specific sections of the Income Tax Act and apply to both salaried and self-employed individuals. Proper use of deductions and exemptions improves financial planning and supports tax compliance in India.

Key tax deductions and exemptions include:

- Section 80C: Investments such as PPF, ELSS, and life insurance

- Section 80D: Health insurance premiums

- House Rent Allowance (HRA): Rent paid by salaried individuals

- Standard Deduction: Fixed deduction for salaried taxpayers

If you are self-employed, you may claim eligible business-related expenses as deductions.

Must Read: Difference Between Deduction and Exemption in Income Tax

Benefits of Paying Taxes

The benefits of taxes go beyond personal compliance. When you pay tax on time, you contribute directly to national progress. If you ask why pay taxes, the answer lies in public services and economic stability funded through tax revenue. The advantages of paying taxes are visible in everyday life.

Major benefits of taxes include:

- Funding infrastructure development, such as roads and transport

- Strengthening the healthcare system

- Supporting the education sector

- Maintaining national defense

These advantages of paying taxes ensure that public systems function properly. Timely payment also improves your financial credibility and avoids tax penalties.

Importance of Taxes for the Indian Economy

The importance of taxes in the economy is directly linked to national stability and development. The role of taxes in India includes funding public expenditure, managing the fiscal deficit, and supporting GDP growth. Tax revenue allows the government to invest in various social welfare schemes and long-term infrastructure development.

Without steady tax collection, economic development would slow, and public services would weaken. A strong tax system in India ensures balanced growth, responsible fiscal policy, and sustainable economic planning.

Consequences of Not Paying Taxes

If you fail to pay tax on time, you may face a tax penalty under the Income Tax Act. Non-payment, underreporting income, or delayed tax filing can trigger an income tax notice from the department. In serious cases, tax evasion can lead to legal action and even prosecution.

Financial consequences may include income tax penalty charges and interest on late payment on the outstanding tax amount. Repeated non-compliance increases scrutiny and may affect your financial credibility. Staying compliant helps you avoid unnecessary tax disputes and protects you from legal and financial risks.

Digital Tax Filing & Compliance in India

In 2026, online income tax filing has become the standard method for submitting returns and managing tax records. The Income Tax Portal allows you to file returns, track refunds, and respond to notices digitally. Tools such as the Annual Information Statement (AIS) and form 26as help you verify TDS in India and other tax details. The introduction of Faceless Assessment has reduced physical interaction and improved transparency.

Strong digital tax compliance ensures accurate reporting, timely tax payment, and reduced errors. With integrated systems, you can monitor income, deductions, and tax liability more efficiently, making tax compliance in India smoother and more reliable.

Who Needs to Pay Tax in India?

If you are wondering who should pay tax in India, the answer depends on your income level and financial activity. Salaried individuals, freelancers, MSMEs, companies, and startups are all covered under tax laws. If your income exceeds the basic exemption limit during the financial year, you must pay income tax and complete a tax filing. Businesses are also required to comply with corporate tax and indirect tax rules. Every taxpayer must review their income carefully and ensure proper tax compliance to avoid penalties.

Conclusion

Taxation in India includes both direct and indirect taxes that fund national development, infrastructure, and essential public services. When you clearly understand the tax definition, the types of taxes in India, and the deductions available under the law, you are better equipped to manage your financial responsibilities efficiently. The Income Tax Department administers direct taxes, while GST operates under the broader indirect tax framework. The importance of tax compliance extends beyond avoiding penalties; it strengthens financial credibility and contributes to economic stability.

Consistent tax compliance also plays a practical role in personal finance. Income tax returns are often required as part of personal loan documents and other credit applications, as lenders assess repayment capacity based on declared income. Maintaining accurate records and timely filings can therefore support smoother loan processing.

If you are planning a major expense and need financial assistance, SMFG India Credit offers personal loans of up to Rs. 30 lakhs*, with interest rates starting from 13%* per annum. Check your personal loan eligibility and apply online. Before submitting your application, you can also use the personal loan EMI calculator and eligibility calculators to plan your finances more effectively.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us