If your business is registered under Goods and Services Tax and has an annual turnover above Rs. 5 crore, GST e-invoice compliance is mandatory.

The e-invoice under the GST system validates your B2B invoices through a government-approved portal before they reach your buyers. Non-compliance can attract penalties and may lead to invoices being treated as invalid.

This article explains GST e-invoice rules in India, including applicability, the generation process, and the consequences of non-compliance.

What Is e-Invoicing in GST?

The government does not generate invoices on your behalf. E-invoice GST is a system in which you create your invoice in your own accounting or ERP software and submit it to the Invoice Registration Portal for authentication. The IRP validates the invoice, generates an IRN (Invoice Reference Number), applies a digital signature, and returns the invoice with a QR code. Only after this is your invoice considered valid under the GST compliance requirements. This GST e-invoice system in India prevents duplicate and fake invoices across the supply chain.

Why GST e-Invoicing Was Introduced

The gst council introduced e-invoicing to fix structural gaps in the tax system:

- Tax evasion: Fake invoices could be used to claim fraudulent Input Tax Credit. Real-time validation on the GST portal puts a stop to this.

- Reconciliation errors: Invoice data now flows automatically into your GST return, reducing mismatches between buyers and sellers.

- Audit trail: Every invoice gets a unique IRN, giving tax authorities complete visibility into B2B transactions.

- E-Way Bill automation: Invoice data auto-populates Part A of the E-Way Bill, cutting down manual effort.

GST e-Invoicing Applicability

GST e-invoice applicability is based on your Aggregate Annual Turnover (AATO), calculated across all GSTINs under a single PAN in India.

E-invoice applicability in GST covers all B2B supplies and exports for businesses with AATO above Rs. 5 crore.

If your turnover was below the threshold last year but crosses it this year, e-invoicing becomes mandatory from the start of the next financial year. Monitor your turnover actively and prepare your ERP systems well in advance.

Proper tracking can also support better cash flow management, especially if you have ongoing or future repayment obligations through external financing. Using tools like a business loan EMI calculator can further help with effective budgeting.

GST e-Invoicing Threshold Limit

The GST e-invoice threshold has been reduced progressively since its introduction in October 2020, starting at Rs. 500 crore and brought down to Rs. 5 crore effective August 1, 2023. As of 2026, the mandatory GST e-invoice limit stands at Rs. 5 crore in annual turnover.

Any business crossing this in a given financial year must comply from the following year onwards. It is worth noting that your AATO includes turnover across all GSTINs registered under a single PAN across India, not just one branch or location.

Businesses Exempt from GST e-Invoicing

Certain businesses are exempt from GST e-invoice requirements regardless of turnover:

- GTAs or Goods Transport Agencies

- Government bodies and local authorities

- Passenger transportation service providers

- Insurance companies, financial institutions, and NBFCs

- Businesses providing cinema admission services in multiplexes

- Units operating within Special Economic Zones (SEZs)

- Entities registered under Rule 14 of the CGST Rules, such as OIDAR service providers

Exempt transactions include B2C supplies, nil-rated or exempt supplies, imports, and high sea sales. Documents such as delivery challans, bills of supply, and ISD invoices also fall outside the scope of the GST e-invoice portal.

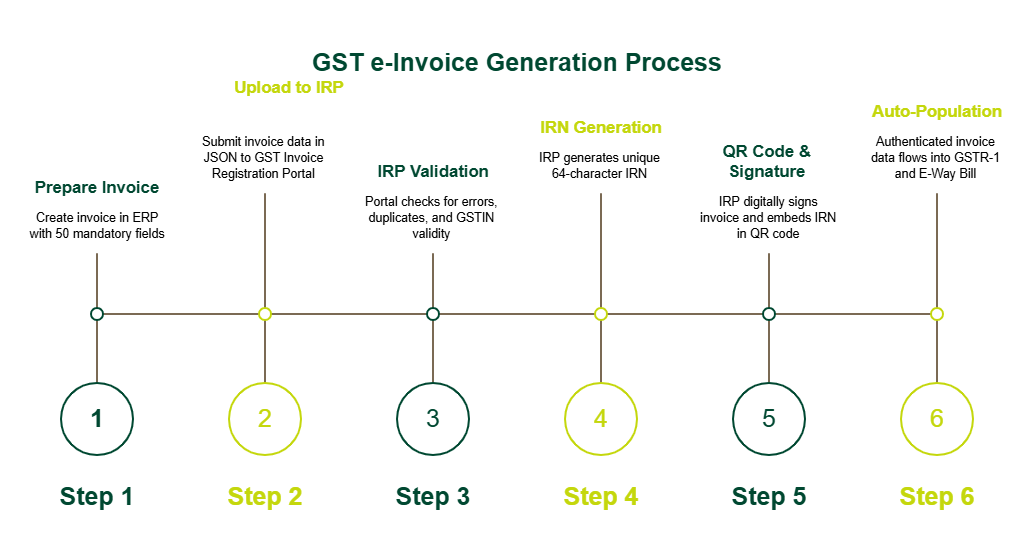

GST e-Invoice Generation Process

Here is the step-by-step e-invoice process Indian businesses must follow:

- Prepare your invoice: Create it in your ERP using the prescribed format, including all 50 mandatory fields, such as supplier GSTIN, buyer GSTIN, HSN codes, invoice value, and tax amounts.

- Upload to the IRP: Submit invoice data in JSON format to the GST Invoice Registration Portal via API integration, GSP, or bulk upload tool.

- IRP validation: The e-invoice GST portal checks for errors, duplicate entries, and GSTIN validity.

- IRN generation process: The Invoice Registration Portal generates a unique 64-character IRN based on your GSTIN, invoice number, financial year, and document type.

- QR code and digital signature: The IRP digitally signs the invoice and embeds the IRN in a QR code that includes the supplier and recipient GSTINs, invoice number, date, value, HSN, and IRN details.

- Auto-population: Authenticated invoice data flows directly into your GSTR-1 draft and the E-Way Bill portal on the GST portal.

GST e-Invoice Workflow

|

Step

|

Action

|

Outcome

|

|

1

|

Create an invoice in ERP

|

Prepared in the prescribed format

|

|

2

|

Upload JSON to IRP

|

Submitted for validation

|

|

3

|

IRP validates data

|

Duplicate and error check done

|

|

4

|

IRN assigned

|

Unique 64-character hash generated

|

|

5

|

QR code and digital signature applied

|

Invoice authenticated

|

|

6

|

Invoice returned to the supplier

|

Valid e-invoice with IRN and QR code

|

|

7

|

Auto-sync to GST portal

|

GSTR-1 and E-Way Bill updated

|

This workflow ensures that every B2B invoice is authenticated before it reaches your buyer, helping you fully meet your GST compliance requirements.

Benefits of GST e-Invoicing for Businesses

Adopting the GST e-invoice system brings clear operational benefits:

- Real-time validation on the Invoice Registration Portal catches errors before invoices are issued.

- Invoice data flows directly into your GST return, cutting manual data entry.

- Buyers can verify invoices instantly, speeding up Input Tax Credit claims.

- E-Way Bill Part A is auto-populated from invoice data, removing duplicate effort.

- Every invoice carries a unique IRN, making audits and dispute resolution straightforward.

- Automation reduces the time and cost spent on manual invoicing processes.

Strong compliance and well-maintained records can also enhance financial credibility in the eyes of lenders, potentially improving access to funding at competitive business loan interest rates.

Common Challenges in GST e-Invoicing

Businesses can face the following practical hurdles when meeting GST compliance requirements around e-invoicing:

- ERP integration: Many accounting systems are not compatible with the JSON schema required by the IRP, leading to API failures and validation errors due to HSN mismatches and incorrect tax mapping.

- Data errors: Wrong recipient GSTIN, duplicate invoice numbers, or incorrect place of supply lead to IRN rejection.

- Cancellation limits: An e-invoice can only be cancelled within 24 hours of IRN generation. Partial cancellations are not allowed, creating difficulties during price revisions or goods returns.

Penalties for Non-Compliance with GST e-Invoicing

Failure to generate an e-invoice or issuing an incorrect one attracts penalties. For non-generation of an e-invoice, the penalty is 100% of the tax amount due or Rs. 10,000 per invoice, whichever is higher, while incorrect or invalid invoicing can result in a penalty of ₹25,000 per invoice. Consistent non-compliance can considerably increase your audit exposure on the GST portal.

Conclusion

GST e-invoicing is a standard compliance requirement for all businesses with a turnover above Rs. 5 crore. From uploading invoices to the GST Invoice Registration Portal to obtaining a valid IRN, every step in the e-invoice process in India serves a clear purpose: making the tax system more transparent and fraud-resistant.

As you manage compliance requirements alongside day-to-day expenses and business growth, maintaining healthy cash flow becomes essential. SMFG India Credit offers unsecured business loans of up to Rs. 75 lakhs* to support your financial needs.

You can use the business loan eligibility calculator to estimate your borrowing capacity and make informed decisions before applying online.

Also, review the business loan documents required in advance to help ensure a smoother application process.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us