ITR-3 and ITR-4 are both income tax return forms used by individuals, firms, and HUFs with business or professional income. ITR-3 is for those with complex income, including capital gains, foreign assets, or non-presumptive business income. ITR-4 is for those opting for the Presumptive Taxation Scheme with a total income up to Rs. 50 lakh.

What Are the ITR-3 and ITR-4 Forms?

ITR-3 and ITR-4 are income tax return forms notified by the Central Board of Direct Taxes (CBDT) for individuals, firms, and HUFs with business or professional income. ITR-3 is for taxpayers who maintain books of accounts and report actual profits, while ITR-4 (Sugam) is for those opting for the Presumptive Taxation Scheme, where income is declared at a fixed percentage of turnover or receipts. Both forms apply under the Income Tax Act for FY 2026–27 (AY 2027–28).

Difference Between ITR-3 and ITR-4

The ITR-3 vs ITR-4 difference spans several parameters. Here is a structured comparison:

|

Parameter

|

ITR-3

|

ITR-4

|

|

Eligible taxpayers

|

Individuals/HUFs with business or professional income

|

Resident individuals, HUFs, and firms (excluding LLPs) under presumptive taxation

|

|

Income limit

|

Not applicable

|

Up to ₹50 lakh

|

|

Taxation method

|

Actual profits

|

Presumptive income

|

|

Books of accounts

|

Required if the threshold crosses the prescribed limit under Sec 44AA

|

Not required

|

|

Necessity of audit

|

Required if income/turnover crosses the prescribed limit under Sec 44AB

|

Not required

|

|

Capital gains

|

All capital gains allowed

|

Only LTCG under Section 112A up to ₹1.25 lakh

|

|

House property income

|

Multiple properties allowed

|

Up to 2 properties

|

|

Foreign assets/income

|

Allowed

|

Not allowed

|

|

Complexity

|

Detailed

|

Simpler

|

Choosing the correct ITR form is important because filing the wrong return may lead to processing delays, defective return notices, or difficulties during income verification. Proper tax compliance may also prove useful when applying for financial products such as a personal loan. Lenders often review income records and tax returns to assess repayment capacity and financial stability.

Keeping tax returns updated can also make it easier to organise the personal loan documents required during the application process. This may help support smoother verification, reduce documentation-related delays, and improve overall processing efficiency.

Who Should File ITR-3?

ITR-3 is used for taxpayers with business or professional income who do not opt for the Presumptive Taxation Scheme. ITR-3 is for whom:

- Individuals and HUFs with business or professional income

- Partners in firms earning remuneration, interest, or profit share

- Taxpayers with short-term or long-term capital gains

- Taxpayers with foreign assets or foreign income

- Individuals with deferred tax on ESOPs

- Taxpayers earning income from more than two house properties

ITR-3 cannot be filed by companies, LLPs, or charitable trusts.

Who Should File ITR-4?

ITR-4 is for taxpayers who opt for the Presumptive Taxation Scheme and have simpler income structures. ITR-4 eligibility requires:

- Total income must not exceed Rs. 50 lakh in the financial year

- Business or professional income is calculated on a presumptive basis under Sections 44AD, 44ADA, or 44AE

- Taxpayers with salary or pension income

- Individuals with income from up to two house properties

- Taxpayers earning interest, dividends, or other income sources

- Individuals with agricultural income up to ₹5,000

ITR-4 cannot be filed by non-residents, company directors, individuals holding unlisted equity shares, or taxpayers with foreign assets/income.

ITR filing for professionals in specified streams (such as engineering, medical, and technical consultancy) can use ITR-4 if they opt for presumptive taxation and stay within the prescribed limits.

ITR-3 vs ITR-4 Eligibility Comparison

Here is a quick ITR-3 vs ITR-4 comparison by taxpayer type to help you decide which ITR form you should file:

|

Taxpayer Type

|

File ITR-3

|

File ITR-4

|

|

Salaried individual with capital gains

|

Yes

|

No

|

|

Freelancer or consultant under Section 44ADA limit

|

No

|

Yes

|

|

Small business owner under Section 44AD

|

No

|

Yes

|

|

Partner in a partnership firm

|

Yes

|

No

|

|

Director in a company

|

Yes

|

No

|

|

Taxpayer with foreign assets

|

Yes

|

No

|

|

A professional maintaining books of accounts

|

Yes

|

No

|

Income Sources Covered Under ITR-3 and ITR-4

|

Income Source

|

ITR-3

|

ITR-4

|

|

Salary or pension

|

Yes

|

Yes

|

|

Business income (non-presumptive)

|

Yes

|

No

|

|

Business income (presumptive under 44AD, 44ADA or 44AE)

|

Yes

|

Yes

|

|

House property income

|

Any number of properties

|

Up to two properties

|

|

Short-term capital gains

|

Yes

|

No (except LTCG u/s 112A up to Rs. 1.25 lakh)

|

|

Long-term capital gains

|

Yes

|

Limited to Section 112A up to Rs. 1.25 lakh

|

|

Foreign income or assets

|

Yes

|

No

|

|

Lottery or racehorse income

|

Yes

|

No

|

|

Dividend income

|

Yes

|

Yes (within limits)

|

|

Agricultural income

|

Yes

|

Up to Rs. 5,000 only

|

Once you are clear about your ITR eligibility and tax compliance requirements, you can use tools such as a personal loan EMI calculator for better borrowing decisions and long-term financial planning.

Strong financial discipline, proper documentation, and a healthy credit profile can improve your chances of securing financing at competitive personal loan interest rates.

Presumptive Taxation and Its Role in ITR-4

Presumptive taxation ITR-4 filing is the defining feature that sets this form apart from ITR-3. Under the Presumptive Taxation Scheme, eligible taxpayers declare a fixed percentage of their turnover or receipts as income, without needing to maintain detailed books of accounts.

|

Scheme

|

Section

|

Applicable To

|

Presumptive Income

|

|

Business income

|

Section 44AD

|

Small businesses and traders

|

8% of turnover (6% for digital receipts)

|

|

Professional income

|

Section 44ADA

|

Specified professionals

|

50% of gross receipts of up to Rs. 50 lakhs (Rs 75 lakhs from FY 2024-25 onwards, with 95% or more receipts being through digital mode)

|

|

Goods carriage income

|

Section 44AE

|

Owners of up to 10 goods vehicles

|

₹7,500 per vehicle per month

|

The scheme simplifies tax filing by removing the need for detailed accounting and tax audits. However, taxpayers declaring income lower than the prescribed presumptive rates may need to maintain books of accounts and file ITR-3 instead.

When Should You Choose ITR-3 Instead of ITR-4?

You may need to switch from ITR-4 to ITR-3 in the following situations:

- Business turnover exceeds the prescribed limit under Section 44AD

- You have taxable short-term or long-term capital gains

- You own foreign assets or earn foreign income

- You declare income lower than the presumptive rate

- You are a company director or hold unlisted shares

- You earn income from more than two house properties

Common Mistakes While Choosing Between ITR-3 and ITR-4

- Using ITR-4 despite having capital gains beyond the allowed limit

- Filing ITR-4 when total income exceeds ₹50 lakh

- Choosing ITR-3 even when eligible for simpler presumptive taxation under ITR-4

- Not matching income details with Form 26AS and AIS before filing

- Reporting partnership firm income in ITR-4 instead of ITR-3

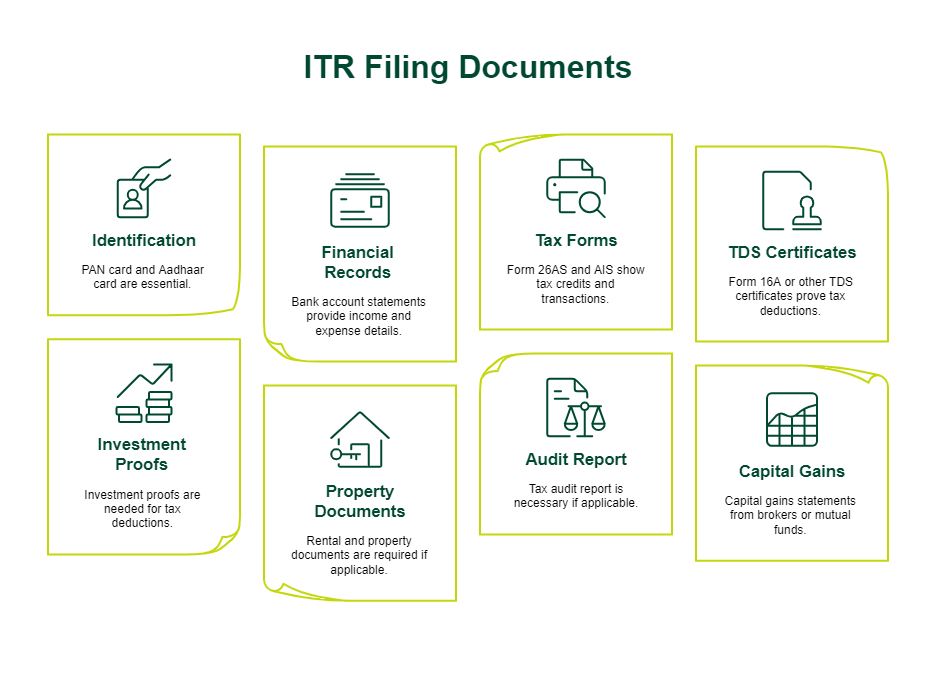

Documents Required for Filing ITR-3 and ITR-4

The basic documents required for both ITR-3 and ITR-4 include:

- Permanent Account Number (PAN) card and Aadhaar card

- Bank account statements

- Form 26AS and AIS

- Form 16A or other TDS certificates

- Investment proofs for tax deductions

- Rental and property documents, if applicable

- Tax audit report, if applicable

- Capital gains statements from brokers or mutual funds

ITR-4 requires fewer documents since presumptive taxation removes the need for audited financial statements. However, it is still advisable to keep basic income and receipt records for verification.

Latest ITR Filing Updates for FY 2026

The Central Board of Direct Taxes (CBDT) has notified updated ITR-3 and ITR-4 forms for FY 2025–26 (AY 2026–27). Key changes include allowing ITR-4 filers to report income from up to two house properties, removal of separate capital gains reporting based on 23 July 2024 timelines, and additional disclosure fields for F&O turnover and income reporting.

Conclusion

The key difference between ITR-3 and ITR-4 is whether income is reported on actual profits or under the Presumptive Taxation Scheme. ITR-3 is suitable for taxpayers with complex income sources, while ITR-4 is meant for eligible small businesses and professionals seeking simpler tax filing.

If you are planning your finances alongside your tax obligations, understanding your borrowing options can also help you make more informed financial decisions. SMFG India Credit offers personal loans of up to Rs. 30 lakhs* at competitive interest rates starting from 13%* per annum. Use our personal loan eligibility calculator to estimate how much you may be qualified to borrow and apply online based on your financial requirements.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us