If you run a business in India, understanding the time of supply in GST is the foundation of accurate tax compliance. If you get the GST time of supply meaning wrong, you risk misreporting your tax liability, attracting penalties, and falling foul of tax authorities.

This guide breaks down everything you need to know about the time of supply of goods under GST, from the basic definition to the rules that apply under different scenarios.

Let’s delve further into the time of supply explanation in GST.

What Is the Time of Supply in GST?

The meaning of the time of supply in GST is the point in time when a supply of goods or services is considered to have taken place. The GST time of supply definition, as laid out in the CGST Act, determines when the GST liability arises. In other words, when you are required to pay tax to the government.

Importance of Time of Supply in GST

Why the time of supply is important cannot be overstated. Here is why it matters:

- Determines when to pay tax: The GST tax point rule fixes the date on which your liability to deposit tax arises.

- Governs invoice timing: It sets the deadline by which a tax invoice must be issued.

- Affects Input Tax Credit (ITC): The recipient's ability to claim ITC depends on the time of supply reported by the supplier.

- Drives GST compliance: Incorrect time of supply in GST leads to mismatches in returns, notices from tax authorities, and interest on delayed payments.

In short, it affects the tax liability timing in GST and sits at the very heart of the Goods and Services Tax compliance mechanism. It keeps the entire invoice-to-payment cycle in check.

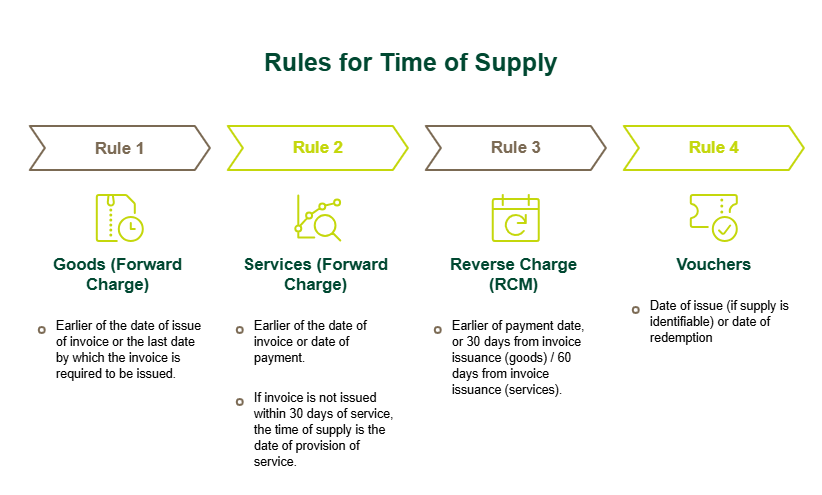

Time of Supply Under Normal Charge (Forward Charge)

Under the forward charge mechanism, where the supplier pays the tax, the time of supply under GST is the earliest of the following three dates, as per Section 12/13 of the CGST Act:

|

Situation

|

Time of Supply

|

|

Invoice issued within the prescribed time

|

Invoice date or payment date, whichever is earlier

|

|

Invoice NOT issued within the prescribed time

|

Delivery date or payment date, whichever is earlier

|

|

Unidentifiable residual cases

|

Date on which the return is to be filed

|

The supplier must issue the invoice on or before the date of removal (for goods involving movement) or on or before the date of delivery (for goods not involving movement). If the invoice is issued within this window, the GST tax point rules are straightforward. The invoice date or payment date, whichever comes first, is the time of supply.

Example: A manufacturer dispatches goods on 5th March and raises the invoice on 3rd March. Payment is received on 20th March. Here, the time of supply is 3rd March (invoice date), since it falls before both dispatch and payment.

Time of Supply Under Reverse Charge (RCM)

The Reverse Charge Mechanism (RCM) in GST shifts the tax payment obligation from the supplier to the recipient. This applies to specific goods and services notified by the government, or when purchases are made from unregistered dealers.

Under the CGST Act, for the time of supply under the Reverse Charge Mechanism, it is the earliest of:

|

Situation

|

Time of Supply

|

|

Date of receipt of goods

|

Date goods are received

|

|

Date of payment

|

Date payment is made or debited from the bank, whichever is earlier

|

|

Date immediately after 30 days from the invoice date

|

If neither of the above is determinable

|

Why does this matter? Under the Reverse Charge Mechanism, the recipient is responsible for self-invoicing and paying the tax. Misidentifying the time of supply for goods under RCM means the tax is deposited in the wrong month, which triggers interest under Section 50 of the CGST Act.

For instance, if a registered dealer receives goods from an unregistered supplier on 10th April and makes payment on 25th April, the time of supply under RCM is 10th April, which is the earlier of the two dates.

Time of Supply for Vouchers

Vouchers are a common business tool, from prepaid gift cards to discount coupons, and GST has specific rules for them. These rules also apply when determining the prepaid vouchers' GST time for taxation.

- If the supply is identifiable at the time of issue (e.g., a voucher redeemable only for a specific product): The time of supply is the date of issue of the voucher.

- If the supply is NOT identifiable at the time of issue (e.g., a general-purpose gift card): The time of supply under GST is the date of redemption of the voucher.

The nature of the voucher, whether it is single-purpose or multi-purpose, determines when the tax clock starts ticking.

How to Determine the Time of Supply?

Here is a step-by-step approach to determine the time of supply under GST for any transaction involving goods. Since the time of supply essentially identifies the taxable event under GST, following the correct sequence is critical:

- Identify the mechanism: Is this a forward charge or Reverse Charge Mechanism?

- Check the invoice date: Has the tax invoice been issued within the prescribed time limit?

- Identify the payment date: When was payment made or received?

- Apply Section 12/13 rules: Compare the relevant dates and pick the earliest.

- Check for special categories: Is it a voucher, continuous supply, or import? These may have separate rules.

- Document your conclusion: Record the time of supply determination for audit readiness.

Using a GST calculator for the time of supply can make this process significantly faster and less error-prone. Several online GST calculators allow you to input transaction details and automatically determine the applicable tax period.

What Happens When the Time of Supply Cannot Be Determined?

There are situations where none of the standard rules can cleanly establish the time of supply, for example:

- No invoice has been issued

- Payment has not been received or recorded

- The date of removal or delivery is disputed

In such cases, the CGST Act provides a residual provision: the time of supply defaults to the date on which the periodic return is to be filed by the supplier.

This residual provision acts as a safety net. However, businesses should not rely on it regularly. It signals a gap in documentation and can attract scrutiny during audits.

Using a GST Calculator for Normal Charge Time of Supply

Manual determination of the time of supply in GST for large volumes of transactions is both time-consuming and error-prone. This is where a GST calculator for time of supply proves its value.

These tools allow businesses to:

- Input tax invoice date, dispatch date, and payment date

- Automatically identify the earliest applicable date

- Generate time of supply reports for filing purposes

- Flag exceptions such as delayed invoicing or RCM applicability

The benefits go beyond speed. Accuracy in time of supply under normal charge transactions directly impacts your GST returns, ITC claims, and cash flow planning.

Conclusion

Time of supply in GST is one of the most operationally significant concepts under India's GST framework. Understanding and correctly applying the rules is essential to keep your business compliant and ensure your GST liability is reported accurately to tax authorities.

Running a compliant business takes more than just knowing the rules. It also takes the right financial foundation. Whether you are managing working capital, covering GST payouts before collections arrive, or scaling operations, SMFG India Credit's unsecured business loans are designed to give you the flexibility you need. With quick processing, competitive interest rates, and loan amounts of up to Rs. 75 lakhs*, your enterprise can stay financially agile so compliance never turns into a cash-flow challenge.

Review the business loan eligibility criteria, use the EMI and eligibility calculators to plan your finances, and apply online with minimal documentation.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us