Buying a new phone in India? The price you see on the box is not the full story. GST on mobile phone purchases applies across every state, and a flat rate shapes the total you pay at checkout. The GST rates on mobile phones cover both handsets and most accessories, which changes how you plan a purchase and how retailers price their stock.

Getting the GST calculation for mobile phones right matters to both buyers and sellers, since a wrong base value throws off the invoice and can create mismatches at return-filing time. This guide walks you through the current rate, HSN codes, calculation method, and ITC rules.

What Is GST on Mobile Phones in India?

Under the Goods and Services Tax (GST) framework of the Government of India, mobile phones are taxed at a single, uniform rate across every state and Union Territory. The GST on mobile phones in India currently sits in the 18% slab, classified under HSN code 8517.

This rate applies the same way to a ₹6,000 feature phone and a flagship smartphone worth ₹1,50,000. GST replaced the old mix of VAT, excise duty, and CST, removing the cascading tax effect and bringing clarity to mobile tax in India figures on every invoice.

Latest GST Rate on Mobile Phones (2026 Update)

The new GST rate on mobile phone purchases was confirmed during the 56th GST council meeting held on 3 September 2025, with changes taking effect from 22 September 2025. Even though many electronic items, such as air conditioners and televisions, moved from 28% to 18% under GST 2.0, the mobile phone GST rate stayed unchanged at 18%.

GST Rate on Mobile Accessories with HSN Code

Most mobile accessories share the same 18% slab as the handset, so your charger, case, and earphones carry the same tax rate on a single invoice. The mobile accessories GST rate keeps billing simple for electronics retailers and for you as a buyer. A small number of items can fall under different HSN codes, but the rate usually stays at 18%.

|

Accessory

|

HSN Code for Mobile Accessories

|

GST on Mobile Accessories

|

|

Mobile phones (handsets)

|

8517

|

18%

|

|

Earphones and headphones

|

8518

|

18%

|

|

Power banks

|

8507

|

18%

|

|

Batteries (lithium-ion)

|

8507 60 00

|

18%

|

|

Memory cards

|

8523

|

18%

|

|

Tempered glass and plastic screen protectors

|

3919 / 7007

|

18%

|

|

Parts used for telephone manufacturing for cellular networks or other wireless networks

|

85

|

12%

|

GST on Mobile Phone Repair Services & Spare Parts

The GST on mobile repair is 18% on both the labour charge and the spare parts. If you visit a service centre to replace a cracked display, the repair bill splits into parts and service, and each line attracts 18% GST separately. Spare parts such as display assemblies, batteries, speakers, charging ports, and internal cables are taxed at 18% under HSN Chapter 85.

The GST on smartphone repair may apply whether the work is under warranty (where the service provider may absorb the tax) or out of warranty. Registered repair shops can claim Input Tax Credit (ITC) on the GST they pay for spare parts, provided the parts are used for taxable repair services.

GST Calculation on Mobile Phones

GST is charged on the taxable value, which is the price after discounts but before tax. The formula for GST price calculation for mobile phones is:

GST Amount = Taxable Value × 18%

Final Price = Taxable Value + GST Amount

For example, if a phone has a taxable value of ₹20,000, the GST comes to ₹3,600 (₹20,000 × 18%). The final invoice price is ₹23,600. If the dealer is in your state, the tax splits as ₹1,800 CGST and ₹1,800 SGST. If the dealer is in another state, the full ₹3,600 is charged as IGST. This mobile price GST in India logic applies uniformly, whether you buy through an e-commerce platform or a physical store.

GST Calculation Example (Detailed Breakdown)

Here is a GST calculation example mobile buyers can use as a reference:

|

Component

|

Intra-State Purchase

|

Inter-State Purchase

|

|

Base Price (Taxable Value)

|

₹30,000

|

₹30,000

|

|

CGST @ 9%

|

₹2,700

|

Nil

|

|

SGST @ 9%

|

₹2,700

|

Nil

|

|

IGST @ 18%

|

Nil

|

₹5,400

|

|

Total GST

|

₹5,400

|

₹5,400

|

|

Final Invoice Value

|

₹35,400

|

₹35,400

|

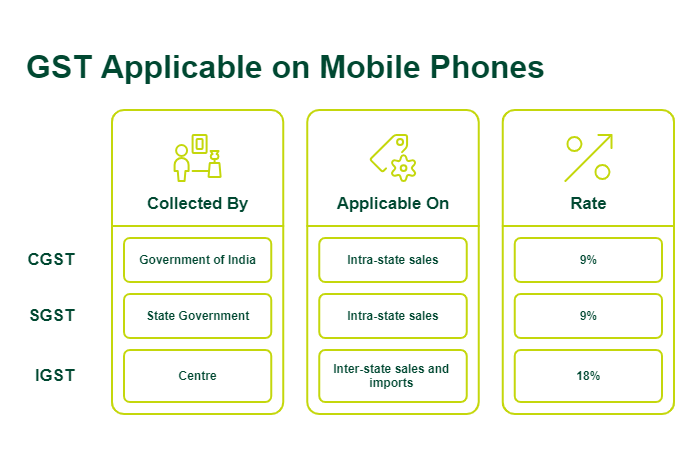

Types of GST Applicable on Mobile Phones

Three types of GST apply to a mobile phone purchase, and the one charged depends on the location of the buyer and the seller.

- CGST (Central GST): Collected by the Government of India on intra-state sales, at 9% on mobile phones.

- SGST (State GST): Collected by the state government on intra-state sales, also at 9%, paid alongside CGST.

- IGST (Integrated GST): Collected by the Centre on inter-state sales and imports, at the full 18%.

How Is the Value of Supply Calculated?

The taxable value of a mobile phone is the transaction value at the time of sale. It includes the base price, any incidental charges like packing and transportation, and excludes GST itself. Pre-sale discounts shown on the invoice reduce the taxable value directly, so GST is charged on the discounted amount. Post-sale discounts, such as cashback given later, do not change the taxable value on the original invoice.

If the seller bundles the phone with a paid accessory as a composite supply, the rate of the principal supply (18% for the mobile) applies to the entire bundle.

GST on Imported Mobile Phones

Imported handsets attract both customs duty and IGST. The GST import mobile phones calculation typically follows this order: first, the basic customs duty is applied on the assessable value, and then IGST at 18% is charged on the sum of the assessable value plus customs duty and any other applicable cess.

In the Union Budget 2024, basic customs duty on mobile phones, mobile Printed Circuit Board Assembly (PCBA), and chargers was reduced to 15% from 20%. GST-registered importers can claim the IGST paid at import as Input Tax Credit, which reduces their effective cost when the handset is onward sold.

Impact of GST on Mobile Phone Prices

The GST impact on mobile prices has brought uniformity across India, so a phone listed at ₹40,000 carries the same tax whether you buy it in Mumbai or Guwahati. The 18% rate raised the effective tax on handsets compared to the pre-GST mix of 5% to 6% VAT plus excise, but it removed the cascading tax effect where each intermediary added tax on top of the last.

This has cleaned up pricing, cut invoice disputes, and given consumers a clear line on the final price. For electronics retailers, GST has also enabled quicker stock movement between states since inter-state check-posts and entry taxes no longer apply.

GST vs Pre-GST Tax on Mobile Phones

The GST vs VAT on mobile phones comparison helps you see what has shifted since July 2017.

|

Component

|

Pre-GST Regime

|

GST Regime

|

|

Tax type

|

VAT + Excise Duty + CST

|

Single GST

|

|

Effective tax rate

|

Approx 6% to 14% combined (varied by state)

|

18% uniform

|

|

Tax-on-tax (cascading)

|

Yes

|

No

|

|

Inter-state movement

|

Additional CST and entry tax

|

IGST only, fully creditable

|

|

Pricing uniformity across states

|

No

|

Yes

|

|

Input credit

|

Limited and fragmented

|

Full ITC on business purchases

|

Can ITC Be Claimed on Mobile Phones?

ITC on mobile phones can be claimed by GST-registered businesses when the handset is bought for business use. If you run a company and issue a phone to an employee for sales calls, customer support, or field work, you can claim the 18% GST paid as Input Tax Credit, subject to normal ITC conditions.

The key GST ITC rules for mobile phones are:

- The phone must be used for business purposes, not personal use

- You must hold a valid tax Invoice carrying the supplier's GSTIN, your GSTIN, HSN Code, and GST amount

- The supplier must have filed their GSTR-1 and paid the tax to the government

- The phone must have been received by you (actual delivery)

- The ITC claim must be filed within the time limit prescribed under the CGST Act

Benefits of GST for Mobile Dealers

For mobile dealers and electronics retailers, GST has made day-to-day operations cleaner in several ways.

The advantages of GST for mobile retailers include:

- One rate replaces the earlier mix of VAT, CST, and entry tax, making pricing and stock transfer easier.

- Dealers can claim ITC on stock purchases, rent, utilities, logistics, and business services.

- GST paid at each stage offsets the GST collected, so only the value addition at each point is taxed.

- Removal of check-posts and entry taxes cuts transit time.

- Customers see the same tax amount on the invoice anywhere in India, increasing trust and transparency.

- A single GST portal tracks returns, payments, and credits, which shortens audit and reconciliation time.

GST Compliance for Mobile Retailers

GST compliance for electronics retailers is set out in the CGST and SGST Acts. A standard retailer with turnover above the threshold has to handle the following to maintain GST mobile compliance in India:

- Obtain a GSTIN for each state of operation

- Issue GST-compliant tax invoices with GSTIN, HSN Code 8517 for handsets, quantity, taxable value, CGST, SGST, or IGST

- File GSTR-1 for outward supplies and GSTR-3B for summary tax liability and ITC

- File GSTR-9 if turnover crosses ₹2 crore in a financial year

- Match the ITC claimed with GSTR-2B before filing GSTR-3B

- Keep purchase, sales, and stock registers for the period prescribed under the GST law

Challenges for Mobile Phone Retailers

The 18% rate and compliance load create some real pressure points for retailers. Here are some key GST issues electronic businesses can face:

- Online sellers often run deep discounts that brick-and-mortar stores cannot match, though GST applies the same way on both, leading to pricing competition

- GST is paid on purchased stock upfront, but sales may take weeks to close, tying up funds

- If a supplier fails to file GSTR-1 on time, your ITC in GSTR-2B gets delayed, blocking your input credit

- CBIC notifications update rules periodically, which adds a compliance-tracking burden

- Margin-scheme accounting for used phones needs extra record-keeping

Common Mistakes in GST Calculation on Mobile Phones

A few errors show up often in mobile invoices and filings. Spot the following mobile GST issues early to avoid disputes and filing problems:

- Charging GST on the MRP instead of the discounted taxable value

- Missing the HSN Code 8517 on the invoice, which can affect ITC for the buyer

- Applying CGST plus SGST on an inter-state sale where IGST should apply

- Forgetting that accessories carry 18% GST and leaving them out of the tax calculation

- Using the wrong tax rate on bundled offers (the rate of the principal supply applies to the full bundle)

- Not reversing ITC when a phone issued to an employee is used for personal purposes

Tips to Ensure Accurate GST Calculation

The following GST billing tips can keep your invoices clean and your compliance straight:

- Use GST software or a verified billing system that auto-applies the 18% rate and corrects HSN codes

- Double-check the HSN Code 8517 on every mobile invoice, along with 8504 / 8518 / 8507 (as applicable) for accessories

- Apply all pre-sale discounts to arrive at the taxable value before calculating GST

- Verify the buyer's state on the invoice to apply CGST plus SGST or IGST correctly

- Reconcile the purchase ITC with GSTR-2B on the GST portal every month

- Train the billing staff on the new GST on mobile phone notifications whenever CBIC issues an update

- Keep a clear record of business-use and personal-use phones to handle ITC reversal cleanly

Conclusion

The GST on mobile phones remains at 18% across India. Whether you are a buyer checking your invoice, a dealer filing returns, or a business claiming ITC, the rules are clear and consistent. Knowing the HSN code, the CGST–SGST–IGST split, and the ITC conditions helps you keep your numbers accurate from the start.

GST on phone sales may not change in the near term, but with accurate billing, timely reconciliation, and proper record-keeping, you can stay compliant and claim all eligible Input Tax Credit efficiently.

Looking to purchase a high-end smartphone? SMFG India Credit offers personal loans of up to Rs. 30 lakhs* to help you manage your purchase without disrupting your savings. Check your eligibility and apply online to benefit from competitive interest rates starting from 13%* per annum.

Explore More on GST

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us