If you miss the deadline for filing your GST return or paying your tax dues, the Government of India charges GST late fees or late payment interest. These are not optional charges. They apply to every GST-registered taxpayer, regardless of whether you have a tax liability or not.

In this article, let us learn how GST penalties for late filing work, how they are calculated, and what the rules say, to save your business from unnecessary costs and legal complications.

What Is the GST Return Late Fee?

The GST late fees meaning refers to a daily charge applied when you fail to file your returns by the prescribed due date. It is levied under the Goods and Services Tax (GST) Act and applies to returns such as GSTR-1, GSTR-3B, GSTR-4, GSTR-9, and others. The GST late filing fee is calculated per day, starting from the day after the due date until you actually file the return.

One important point to keep in mind: The late filing penalty in GST applies even when you are filing a nil return, meaning you had no sales, purchases, or tax liability in that period. Late fees must be paid in cash (via the Electronic Cash Ledger) and cannot be offset using Input Tax Credit (ITC).

What Is GST Interest?

The GST interest's meaning differs from a late fee. While a late fee is charged for delayed filing, interest on GST late payment is charged when you fail to pay your tax dues on time. The GST interest rate is 18% per annum for delayed tax payments on Central GST (CGST), State GST (SGST), and Integrated GST (IGST).

Interest is calculated on the net tax liability after adjusting the eligible Input Tax Credit (ITC). If you have claimed excess ITC or reduced your output tax liability beyond what is permitted, a higher interest rate of 24% per annum applies. These GST payment delay charges can add up quickly if left unaddressed.

Difference Between GST Late Fees and Interest

Understanding the GST late fees vs interest distinction is essential for proper compliance under the Goods and Services Tax framework. While both are charges for delays, they apply in different situations and are calculated differently.

|

Basis

|

GST Late Fees

|

GST Interest

|

|

What triggers it?

|

Delay in filing the GST return

|

Delay in paying tax dues

|

|

Rate

|

₹50/day (₹20/day for nil returns)

|

18% or 24% per annum

|

|

Paid via

|

Cash only (no ITC)

|

Cash only

|

|

Applicable on

|

All GST-registered taxpayers

|

GST taxpayers with pending tax liability

|

|

Calculated from

|

Day after the due date until the return is filed

|

Due date until the actual payment date

|

Knowing this difference between GST penalty and interest helps you avoid confusion and ensures that both filing and payment obligations are met on time.

GST Return Due Dates

Your GST return due date depends on your taxpayer category and the type of return you file. Missing these dates triggers GST late fees and interest charges. Here is a summary of the key deadlines:

|

Return Form

|

GST Return Due Date

|

|

GSTR-1 (Monthly)

|

11th of the next month

|

|

GSTR-1 (Quarterly)

|

13th of the month after the quarter ends

|

|

GSTR-3B (Monthly)

|

20th of the next month

|

|

GSTR-3B (Quarterly)

|

22nd (category X states) or 24th (category Y states) of the month after the quarter ends

|

|

CMP-08 (Quarterly)

|

18th of the month after the quarter ends

|

|

GSTR-4 (Annual)

|

30th June following the financial year

|

|

GSTR-5 (Monthly)

|

13th of the next month

|

|

GSTR-5A (Monthly)

|

20th of the next month

|

|

GSTR-6 (Monthly)

|

13th of the next month

|

|

GSTR-7 (Monthly)

|

10th of the next month

|

|

GSTR-8 (Monthly)

|

10th of the next month

|

|

GSTR-9 (Annual)

|

31st December of the next financial year

|

|

GSTR-9C (Annual)

|

31st December of the next financial year

|

|

GSTR-10 (One-time)

|

Within three months of GST registration cancellation

|

Note: GST filing due dates are subject to changes through CBIC notifications and orders.

Interest on Late Payment of GST

If you fail to pay your GST dues by the applicable due date, GST interest on delayed payment applies from the day after the due date until the actual payment date. The rates are set by the Central Board of Indirect Taxes and Customs (CBIC).

|

Particulars

|

GST Interest Rate

|

|

Tax paid after due date

|

18% per annum

|

|

Excess ITC claimed or excess reduction in output tax liability

|

24% per annum

|

GST interest calculation formula:

Interest = (Outstanding tax liability × Interest rate × Number of days of delay) / 365

Example: You have a tax liability of ₹10,000 for January 2026, due on 20th February 2026. You make the payment on 22nd March 2026, a delay of 30 days.

Interest = (₹10,000 × 18% × 30) / 365 = ₹147.95

GST Late Fees Calculation

GST late fees calculation is based on the number of days you delay filing your return. For returns like GSTR-1 and GSTR-3B, the GST late fee per day is ₹50, split equally between CGST and SGST at ₹25 each. For nil returns, the GST penalty per day is ₹20, split as ₹10 each under CGST and SGST.

Example: You file GSTR-3B for February 2026 on 23rd March 2026. The due date was 20th March 2026, so the delay is 3 days.

Late fee = ₹50 × 3 = ₹150 (₹75 under CGST + ₹75 under SGST)

For a nil return with the same delay: ₹20 × 3 = ₹60 (₹30 CGST + ₹30 SGST)

Late fees cannot be paid using ITC. You must pay in cash through the GST portal.

GST Late Fees Structure (Return-wise)

Here is a return-wise breakdown of the GST penalty per day and applicable charges:

|

Return Type

|

Who Files It

|

Late Fee per Day

|

|

GSTR-3B

|

Every GST-registered taxpayer

|

₹50/day (₹20/day for nil returns)

|

|

GSTR-1

|

Registered suppliers reporting outward supplies

|

₹50/day (₹20/day for nil returns)

|

|

GSTR-4

|

Composition scheme taxpayers

|

₹50/day (₹20/day for nil returns)

|

|

GSTR-7

|

TDS deductors under GST

|

₹50/day per act per return

|

|

GSTR-9

|

All registered taxpayers (annual return)

|

₹50 to ₹200/day depending on turnover

|

|

GSTR-10

|

Taxpayers whose registration is cancelled

|

₹200/day

|

Maximum Late Fees Under GST

The GST penalty rules set a cap on the late fees you can be charged. These caps apply from June 2021 onwards, following the 43rd GST Council meeting.

The GST late fee limits are as follows:

|

Return

|

Type

|

Annual Turnover (Previous Year)

|

Max Late Fee (CGST)

|

Max Late Fee (SGST)

|

Total Maximum

|

|

GSTR-1 and GSTR-3B

|

Nil return

|

N/A

|

₹250

|

₹250

|

₹500

|

|

GSTR-1 and GSTR-3B

|

Other

|

Up to ₹1.5 crore

|

₹1,000

|

₹1,000

|

₹2,000

|

|

GSTR-1 and GSTR-3B

|

Other

|

₹1.5 crore to ₹5 crore

|

₹2,500

|

₹2,500

|

₹5,000

|

|

GSTR-1 and GSTR-3B

|

Other

|

More than ₹5 crore

|

₹5,000

|

₹5,000

|

₹10,000

|

|

GSTR-4 (from FY 2021-22)

|

Nil return

|

N/A

|

₹250

|

₹250

|

₹500

|

|

GSTR-4 (from FY 2021-22)

|

Other

|

N/A

|

₹1,000

|

₹1,000

|

₹2,000

|

|

GSTR-7 (TDS under GST)

|

N/A

|

N/A

|

₹1,000

|

₹1,000

|

₹2,000

|

Penalty for Missing GST Due Date

When you miss the return due date, two charges may apply simultaneously: GST penalty for late filing on delayed returns and interest on any unpaid tax liability. This combination makes delays costly.

Beyond direct charges, missing deadlines carries wider consequences. If you miss two consecutive GSTR-3B filings, your GSTR-1 gets blocked. Continued non-filing can also lead to restrictions on e-Way bill generation. Prolonged non-compliance may eventually put your GST registration at risk of suspension or cancellation.

For enterprises planning for investment or applying for external financing, such as a business loan, a clean GST compliance record is an important factor that stakeholders may review as part of their eligibility assessment. Timely GST return filing helps maintain both compliance standing and financial credibility.

Examples of GST Late Fees and Interest Calculation

Here are a few practical GST late fees examples to help you understand how charges work:

|

Scenario

|

Details

|

Calculation

|

Amount

|

|

GSTR-3B filed 3 days late (with tax liability)

|

Due: 20th March 2026, Filed: 23rd March 2026

|

₹50 × 3 days

|

₹150

|

|

GSTR-3B filed 3 days late (nil return)

|

Due: 20th March 2026, Filed: 23rd March 2026

|

₹20 × 3 days

|

₹60

|

|

Tax payment delayed by 30 days

|

Tax: ₹10,000, Rate: 18% p.a.

|

(₹10,000 × GST Interest Rate [18%] × 30) / 365

|

₹147.95

|

|

Tax payment delayed by 20 days

|

Tax: ₹50,000, Rate: 18% p.a.

|

(₹50,000 × GST Interest Rate [18%] × 20) / 365

|

₹493.15

|

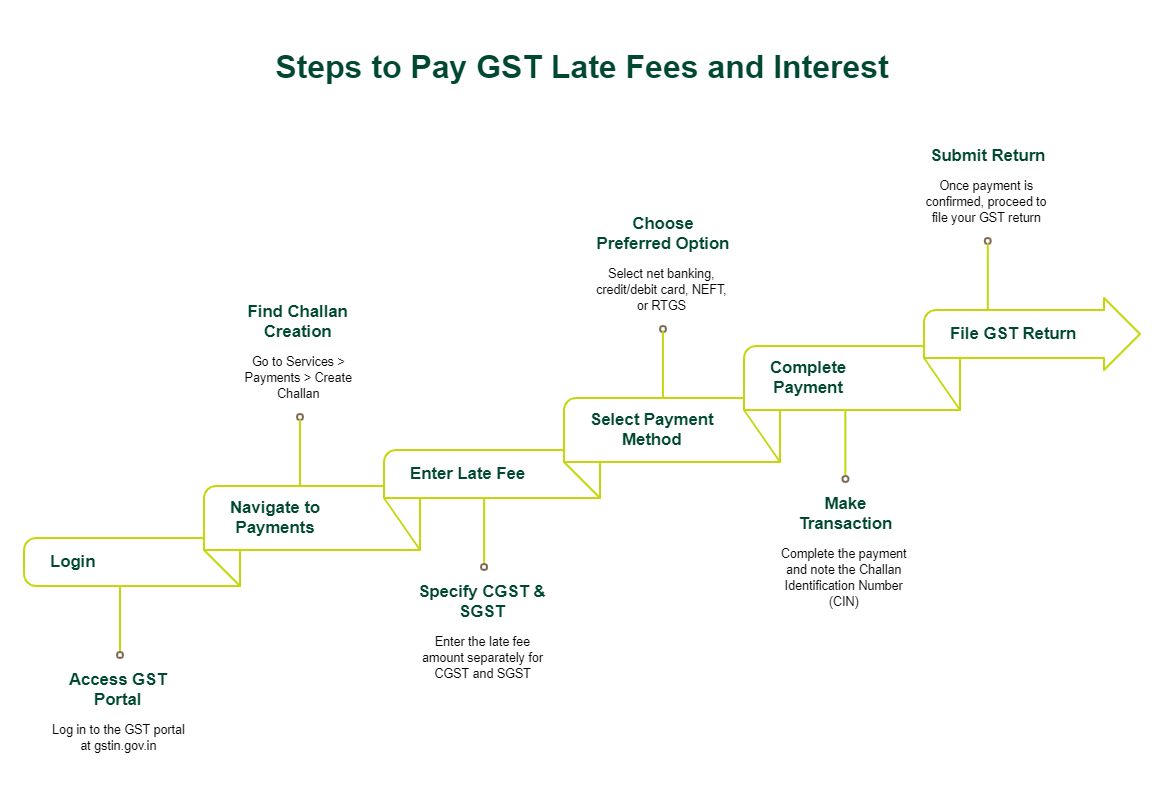

How to Pay GST Late Fees and Interest on the Portal

The GST portal automatically calculates any applicable late fee when you submit your return. The fee for the current period also includes any unpaid charges carried forward from the previous period. Here is how to complete the GST late fees or interest payment process:

- Log in to the GST portal at gstin.gov.in.

- Navigate to Services > Payments > Create Challan.

- Enter the late fee amount under the relevant head, separately for CGST and SGST.

- Select your preferred payment method: net banking, credit or debit card, NEFT, or RTGS.

- Complete the payment and note your Challan Identification Number (CIN).

- Once payment is confirmed, proceed to file your GST return.

You cannot file your return until the late fee is cleared.

Rules Applicable for GST Payment

GST penalty rules vary depending on your taxpayer category. Here is what applies to each:

Regular taxpayers: You must file both GSTR-1 and GSTR-3B and pay any tax due by the prescribed due date. Failure to do so results in GST late payment interest and late fees.

Composition scheme taxpayers: You file GSTR-4 annually but must make quarterly tax payments via CMP-08 by the 18th of the month following the quarter. Late payments attract 18% per annum interest.

Casual taxable persons: You must register for GST before starting business and pay tax in advance based on estimated liability. Late payments carry the same GST compliance penalty as regular taxpayers.

Key rules applicable across all categories:

- Late fees must always be paid in cash. ITC cannot be used.

- All tax-related payments above ₹10,000 must be made digitally.

- Challans generated on the GST portal are valid for 15 days.

- If a CIN is not generated after online payment, you can submit Form GST PMT-07 (grievance against payment).

Tips To Avoid GST Late Fees and Interest

- Set calendar reminders for every GST return due date at least five days in advance.

- File nil returns on time even when you have no transactions for the period.

- Reconcile your ITC monthly by matching invoices with GSTR-2B to avoid excess ITC claims.

- Keep a sufficient balance in your electronic cash ledger before the due date arrives.

- Review your GST liability, cash, and credit ledgers regularly to catch mismatches early.

- Work with a tax professional or use GST compliance software to reduce the risk of last-minute errors.

Latest Updates on GST Late Fees and Interest

From July 2025, the Government of India has introduced a time limit on filing pending GST returns. Taxpayers will no longer be able to file monthly or annual returns more than three years after the original due date. This change affects GSTR-1, GSTR-3B, and several other returns. If you have any pending returns from earlier years, filing them without delay is essential to avoid losing your ability to file entirely.

For FY 2022-23 onwards, CBIC Notification 07/2023 reduced the late fee for GSTR-9. Taxpayers with an Annual Aggregate Turnover (AATO) up to ₹5 crore pay ₹50 per day, capped at 0.04% of turnover in the relevant state or union territory. Those with an AATO between ₹5 crore and ₹20 crore shall pay late fees of ₹100 per day, capped at 0.04% of turnover in the relevant state or union territory.

Conclusion

GST late payment interest and late fees are direct financial consequences of missing return filing and payment deadlines. The charges follow a clearly defined structure under the GST Act, with specific rates, caps, and rules for each return type. For small businesses and large enterprises alike, staying on top of your GST return due dates is one of the most straightforward ways to avoid unnecessary costs. File on time, reconcile your ITC regularly, and keep your cash ledger funded.

Strong GST compliance also enhances your financial profile and business credibility, which are important when seeking external financing. If you are planning to expand operations, manage cash flow, or invest in your next phase of growth, a business loan from SMFG India Credit could be a suitable option. Check your eligibility and apply online to access competitive business loan interest rates and unsecured funding of up to Rs. 75 lakhs*.

Explore More on GST

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us