The Reverse Charge Mechanism under GST is a system where the responsibility to pay GST shifts from the supplier to the recipient of goods or services. In simple terms, the buyer becomes responsible for the GST tax liability instead of the seller in specific situations notified under the GST Council laws.

Understanding the RCM meaning in GST is important because it affects invoicing, tax payments, and compliance requirements for businesses. RCM in GST commonly applies to selected goods, services, and transactions where reverse charge GST applicability rules are triggered, requiring the GST recipient tax payment to be made directly to the government.

What Is Reverse Charge Mechanism Under GST?

The GST Reverse Charge Mechanism, explained simply, means that the responsibility to pay GST shifts from the supplier to the recipient in specified cases. The RCM meaning in GST is covered under Sections 9(3), 9(4), and 9(5) of the CGST Act. Section 9(3) covers notified goods and services, Section 9(4) applies to certain purchases from unregistered suppliers, and Section 9(5) applies to specific e-commerce services. Unlike forward charge, where the supplier pays tax, reverse charge on GST requires the buyer to deposit the tax directly.

For example, if a business hires legal services from an advocate, the business receiving the service may need to pay GST under RCM.

Forward Charge vs Reverse Charge Mechanism

Understanding the difference between forward charge and reverse charge is important for proper GST compliance and tax reporting. Under the forward charge mechanism, the supplier collects and pays GST to the government. Under reverse charge, the recipient becomes responsible for paying tax directly. This reverse charge vs forward charge comparison helps businesses understand their GST payment responsibilities more clearly.

|

Basis

|

Forward Charge

|

Reverse Charge Mechanism

|

|

Who Pays Tax

|

Supplier pays GST to the government

|

Recipient pays GST directly to the government

|

|

Tax Collection

|

GST is collected from the buyer by the supplier

|

GST recipient pays tax without supplier collection

|

|

Invoice Responsibility

|

Supplier issues a GST invoice with tax

|

Supplier may issue an invoice, but the recipient handles tax payment

|

|

GST Compliance Burden

|

Mainly on the supplier

|

Shifts partly to the recipient

|

|

ITC Eligibility

|

Recipient may claim ITC if conditions are met

|

Recipient may claim ITC after paying GST under RCM

|

|

Common Applicability

|

Regular sale of goods and services

|

Specific GST-notified services, goods, and transactions under GST

|

Types of Reverse Charge Mechanism

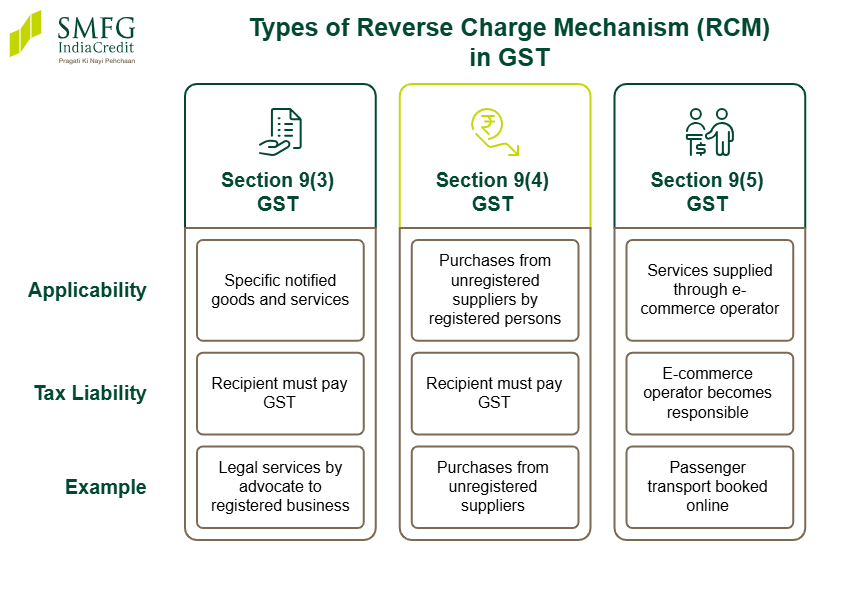

The types of RCM in GST are mainly divided under Sections 9(3), 9(4), and 9(5) of the CGST Act. Each provision defines different situations where the GST recipient's tax liability shifts from the supplier to the buyer or service recipient. Businesses should understand these categories carefully because reverse charge under GST rules may apply differently depending on the transaction type and supplier category.

- Section 9(3) GST: Applies to specific notified goods and services where the recipient must pay GST. For example, legal services provided by an advocate to a registered business may attract RCM.

- Section 9(4) GST: Applies to certain purchases made from unregistered suppliers by specified registered persons, subject to current government notifications and applicability updates.

- Section 9(5) GST: Applies to specific services supplied through an e-commerce operator, where the operator becomes responsible for GST payment instead of the actual service provider. Examples may include certain passenger transport or accommodation services booked online.

Goods Covered Under Reverse Charge Mechanism

Certain GST-notified goods are covered under the Reverse Charge Mechanism, where the recipient becomes responsible for paying GST instead of the supplier. The list of goods under reverse charge is specified through government notifications and may change from time to time. Businesses should regularly review the latest RCM goods list to ensure proper GST compliance and tax reporting.

Illustrative List of Goods Covered Under RCM

|

Goods Type

|

Supplier

|

Recipient

|

Reverse Charge GST Applicability

|

|

Cashew nuts (not shelled or peeled)

|

Agriculturist

|

Registered person

|

GST payable under RCM

|

|

Tobacco leaves

|

Agriculturist

|

Registered person

|

GST payable under RCM

|

|

Raw cotton

|

Agriculturist

|

Registered person

|

GST payable under RCM

|

|

Silk yarn manufactured from raw silk

|

Manufacturer of silk yarn

|

Registered person

|

GST payable under RCM

|

|

Metal scrap

|

Unregistered person

|

Registered person

|

GST payable under RCM

|

|

Used vehicles, scrap, confiscated goods

|

Central/State Government or local authority

|

Registered person

|

GST payable under RCM

|

The above list is illustrative and not exhaustive. Additional goods may also fall under RCM based on GST notifications and regulatory updates.

Services Covered Under Reverse Charge Mechanism

Certain GST RCM services require the recipient of the service to pay GST instead of the supplier. The reverse charge services list under GST includes specific notified services that commonly affect businesses, corporates, financial institutions, and registered taxpayers. Businesses should regularly review updates to services under RCM, as GST notifications and applicability rules may change over time.

Illustrative List of Services Covered Under RCM

|

Service Type

|

Supplier of Service

|

Recipient of Service

|

Reverse Charge GST Applicability

|

|

Goods Transport Agency (GTA) services

|

Goods Transport Agency (GTA)

|

Registered businesses and specified entities

|

GST payable under RCM

|

|

Legal services by advocates or law firms

|

Advocate or law firm

|

Business entity in taxable territory

|

GST payable under RCM

|

|

Director services

|

Director

|

Company or body corporate falling under taxable territory

|

GST payable under RCM

|

|

Sponsorship services

|

Person other than body corporate

|

Body corporate or partnership firm falling under taxable territory

|

GST payable under RCM

|

|

Insurance agent services

|

Insurance agent

|

Insurance company falling under taxable territory

|

GST payable under RCM

|

|

Recovery agent services

|

Recovery agent

|

Banks, NBFCs, financial institutions under taxable territory

|

GST payable under RCM

|

The above examples are illustrative and not exhaustive. Additional services may also fall under RCM based on the latest GST notifications and regulatory updates.

Reverse Charge Mechanism on E-commerce Transactions

Under section 9(5) GST, the responsibility to pay GST on certain services shifts from the actual service provider to the e-commerce operator. This e-commerce GST reverse charge framework mainly applies to aggregator-based digital platforms that facilitate transportation, accommodation, and specific household services. Recent GST updates have continued to clarify compliance responsibilities for GST on e-commerce operators and platform-based transactions.

Examples of services covered under Section 9(5) include:

- Passenger transport services provided through taxi and ride-hailing platforms.

- Transportation of passengers through certain omnibus booking platforms.

- Accommodation services such as hotels, inns, guest houses, and campsites booked through e-commerce platforms.

- Housekeeping and home services such as plumbing, carpentry, and similar services offered through digital aggregator platforms.

In these cases, the e-commerce operator may become responsible for GST payment instead of the actual service provider.

Examples of the Reverse Charge Mechanism Under GST

Understanding reverse charge examples can help businesses identify situations where GST must be paid directly by the recipient instead of the supplier. These RCM examples in GST are commonly seen across transport, legal, import, and corporate service transactions. Reviewing GST practical examples can also help businesses improve compliance and tax reporting accuracy.

- Legal Services: If a business hires an advocate or law firm, the business receiving the service may need to pay GST under RCM.

- Goods Transport Agency (GTA) Services: A registered company using GTA transport services may become responsible for GST payment under reverse charge.

- Director Remuneration: In certain cases, companies may need to pay GST under RCM on services provided by directors.

- Sponsorship Services: GST liability may shift to the recipient when sponsorship services are provided to a body corporate or partnership firm.

Time of Supply Under Reverse Charge Mechanism

The time of supply under RCM determines when GST becomes payable by the recipient under reverse charge provisions. Businesses must understand these GST supply rules carefully because the tax liability arises based on specific dates related to invoices, payments, or receipt of goods and services. These reverse charge timing rules differ slightly for goods and services.

For Goods, the time of supply is generally the earliest of:

- Date of receipt of goods.

- Date of payment.

- 30 days from the supplier’s invoice date.

For Services, the time of supply is generally the earliest of:

- Date of payment.

- 60 days from the invoice date.

- Date recorded in the recipient’s books, if applicable.

If these dates cannot be determined, the date of entry in the recipient’s books may be considered.

Input Tax Credit (ITC) Under Reverse Charge Mechanism

Businesses may generally claim ITC under reverse charge on the GST paid under RCM, provided the goods or services are used for business purposes, and all applicable GST conditions are satisfied. Claiming Input Tax Credit under GST can help reduce the overall tax burden for eligible businesses. However, GST under reverse charge must first be paid before the ITC claim can be availed.

Basic conditions for a GST ITC claim under RCM include:

- GST payment under reverse charge must be credited to the government.

- Valid tax invoices and supporting records should be maintained.

- Goods or services should be used for business purposes.

- ITC should be reported correctly in GST returns.

Basic ITC claim process:

- Pay GST liability under RCM.

- Record the transaction in GST returns.

- Claim eligible ITC in the applicable return period.

GST Registration Requirement Under RCM

GST registration under RCM may become mandatory in certain cases where businesses are liable to pay tax under reverse charge provisions. While normal GST threshold exemptions may apply to many small businesses, specific reverse charge compliance rules can still require registration depending on the nature of goods, services, or notified transactions involved. Businesses dealing in notified supplies, import of services, or certain e-commerce transactions should carefully review whether mandatory GST registration applies to them under current GST provisions and notification updates.

Invoicing Rules Under Reverse Charge Mechanism

Under reverse charge provisions, businesses may need to follow additional GST invoice rules for proper compliance and recordkeeping. In certain situations, the recipient may have to issue a GST self-invoice if the supplier is unregistered. Businesses may also need to issue a payment voucher GST document at the time of making payment to the supplier. Following the correct GST self-invoicing process can help avoid compliance issues during audits or return filing.

Important invoice details businesses should maintain include:

- Supplier and recipient details

- GSTIN and invoice number

- Description of goods or services

- Invoice date and payment date

- Applicable GST rate and tax amount

- Reference to reverse charge applicability

GST Return Filing for RCM Transactions

Businesses liable to pay GST under reverse charge must report these transactions correctly while filing GST returns. Proper GST filing for RCM transactions is important because the tax liability and eligible input tax credit must both be disclosed accurately. Most reverse charge liabilities are generally reported in GSTR-3B reverse charge sections, along with related ITC claims where applicable. Maintaining organised records can also help businesses improve GST reporting under RCM and reduce reconciliation issues during audits.

Best practices for RCM reporting and compliance include:

- Record all reverse charge transactions separately in accounting records

- Report applicable RCM liability correctly in GSTR-3B

- Maintain self-invoices and payment vouchers where required

- Match invoices, payment records, and GST returns regularly

- Ensure eligible ITC claims are reported in the correct return period

Advantages and Disadvantages of Reverse Charge Mechanism

The Reverse Charge Mechanism offers several GST compliance benefits by improving tax collection and bringing specific transactions into the formal tax system. At the same time, businesses may also face additional reporting and documentation responsibilities under RCM rules. Understanding both the benefits of the reverse charge mechanism and the disadvantages of RCM can help businesses manage compliance more effectively.

Advantages:

- Helps reduce tax evasion in certain sectors

- Improves GST tax collection efficiency

- Expands tax compliance across unorganised sectors

- Allows eligible businesses to claim ITC on RCM payments

Disadvantages:

- Increases compliance and recordkeeping burden

- May affect short-term business cash flow

- Requires additional invoicing and reporting procedures

- Can create confusion for small businesses unfamiliar with reverse charge compliance rules

Penalties for Non-Compliance Under RCM

Failure to comply with reverse charge provisions may lead to a GST penalty under RCM equal to the tax amount due or Rs. 10,000, whichever is higher. Continued incorrect reporting, delayed return filing, or unpaid GST liability can also result in additional scrutiny and legal action under GST law.

Businesses should maintain accurate records and timely filings to avoid GST non-compliance issues and other reverse charge penalties.

Managing Cash Flow Challenges Under GST Compliance

Reverse charge transactions can sometimes create short-term cash flow pressure for businesses because GST must often be paid upfront before claiming eligible ITC. Delayed payments, additional compliance costs, or blocked working capital may affect daily operations, especially for small and growing businesses. In such situations, a business loan may help enterprises manage operational expenses, maintain liquidity, and handle GST-related obligations more smoothly.

Businesses planning their finances carefully may also benefit from assessing repayment capacity before borrowing. Using tools such as a business loan eligibility calculator can help estimate borrowing limits and support more informed financial planning while managing compliance and working capital requirements.

Conclusion

The Reverse Charge Mechanism under GST shifts the responsibility of GST payment from the supplier to the recipient in specified transactions. Understanding RCM rules, compliance requirements, invoicing obligations, and ITC eligibility can help businesses avoid penalties, improve GST reporting accuracy, and manage tax-related responsibilities more efficiently.

For enterprises balancing GST compliance with operational and growth requirements, SMFG India Credit offers unsecured funding of up to Rs. 75 lakhs* at competitive business loan interest rates.

Check out the business loan documents required and apply online today.

* Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG India Credit. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG India Credit's policy at the time of loan application. If you wish to know more about our products and services, please contact us